Dollar soars as Trump launches trade war

The US dollar rallied during almost the entirety of last week as all signs suggested that the imposition of tariffs from the Trump administration was imminent.

FX Market Updates

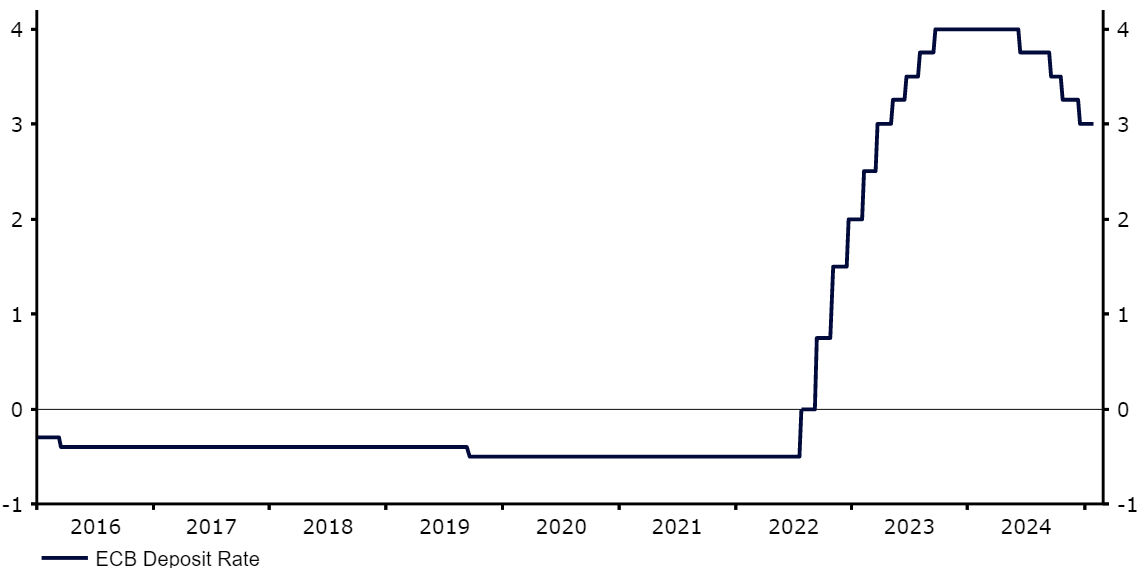

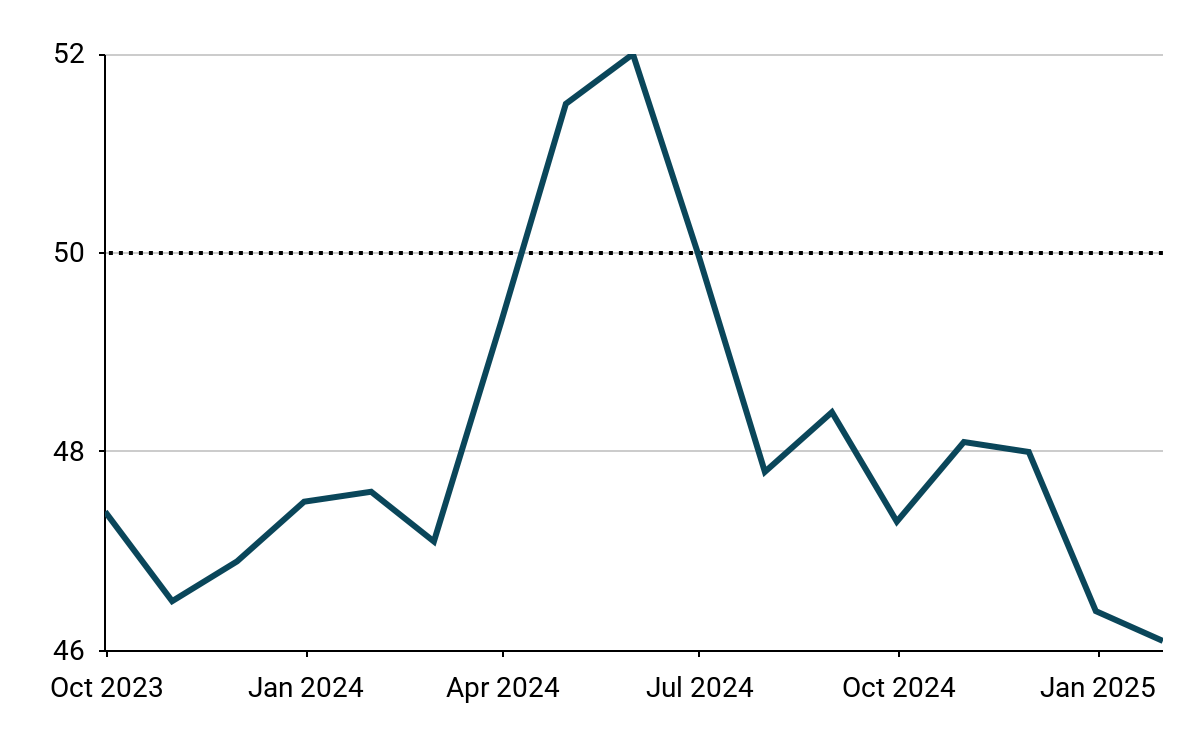

The US dollar rallied during almost the entirety of last week as all signs suggested that the imposition of tariffs from the Trump administration was imminent.Over the weekend, the White House confirmed that harsh 25% tariffs would be imposed on Canadian and Mexican goods, save for Canadian energy, where 10% would be levied. 10% tariffs were imposed on China, and will also take effect on Tuesday. All in all, this is a combination that makes little macroeconomic sense, except as leverage over other political goals. The dollar surged upwards during Asian trading on the back of the news, with the European currencies (including the euro) bearing the brunt of the sell-off. EM currencies have also been hit hard, led by the Mexican peso itself.Ordinarily, the key moments for markets this week would have been Eurozone inflation data (Monday), the BoE meeting on Thursday, and the US payrolls release (Friday). However, Trump's trade war, including announcements of further tariffs (levies on EU products are expected to follow shortly) and any hints at the conditions Trump will demand for easing the pressure will swamp other macro news Even after the recent sell off, most currencies still trade at levels that imply markets are expecting draconian tariff levels to be short lived. We hope they are right.USDA most anodyne Federal Reserve meeting last week was completely overshadowed by the escalation of rhetoric leading to the imposition of tariffs over the weekend. The dollar has rallied hard as a result, and is trading higher against almost every currency worldwide in the past week, with very few exceptions. Unlike in Europe, the biggest economic impact of the tariffs to the US looks likely to be higher inflation and, consequently, a more hawkish FOMC. As things stand, futures are now not fully pricing in the next Fed cut until September, with a second cut only assigned around a 50/50 chance.The macroeconomic focus this week is on labour market data, including the JOLTS report on Wednesday and the payrolls report for January on Friday. Markets expect further evidence that suggests the economy is humming along nicely. Yet, as elsewhere, tariff headlines will probably overwhelm any response to the actual data. EURThe January meeting of the European Central Bank adhered to the script very closely. The bank cut rates by 25bps and hinted that policymakers are comfortable with market expectations of another rate reduction in March. January Inflation data on Monday should bring further comfort to the Governing Council, with the core index expected to fall to 2.6% and inch closer to the 2% target.Nevertheless, Trump's trade war means that headlines on tariffs will be a far more important factor in how the euro trades than macroeconomic reports. Indeed, we’ve already seen a downward repricing in Euro Area rates in response to the news over the weekend, as investors brace for weaker European growth and, therefore, a more dovish ECB.Figure 1: ECB Deposit Rate (2016 - 2025) Source: LSEG Datastream Date: 03/02/2025 GBPThe UK seems to be relatively low on the list of the Republican targets for tariffs, which means that sterling is performing better than other European currencies. Trump said over the weekend that the UK was ‘out of line’ with regards to its trade policies, although he also hinted that a deal could be reached that avoided the imposition of tariffs. Britain actually runs a decent trade surplus with the US, which could be used to sidestep import duties. The onus will be on Keir Starmer’s government to strike a deal, yet he will be in Brussels this week looking to ‘reset’ the UK’s relationship with the EU - not exactly great timing.The Bank of England is expected to cut rates by 25 basis points on Thursday, as it prioritises weak growth over still high inflation. We do not expect a unanimous decision, but it is possible that MPC votes and communications will reflect the increased gloom brought about by Trump's trade war, opening the way for further cuts beyond those already priced in. RONThe all-time-low manufacturing PMI reading (46.1) adds to a list of rather uninspiring macroeconomic data points out of Romania (albeit the index is less than two years old, which makes the outlook less dramatic). Thursday will give us an insight into domestic demand, with a December retail sales reading, which should be far more important.Figure 2: Romania Manufacturing PMI (2023 - 2024)

Source: LSEG Datastream Date: 03/02/2025 GBPThe UK seems to be relatively low on the list of the Republican targets for tariffs, which means that sterling is performing better than other European currencies. Trump said over the weekend that the UK was ‘out of line’ with regards to its trade policies, although he also hinted that a deal could be reached that avoided the imposition of tariffs. Britain actually runs a decent trade surplus with the US, which could be used to sidestep import duties. The onus will be on Keir Starmer’s government to strike a deal, yet he will be in Brussels this week looking to ‘reset’ the UK’s relationship with the EU - not exactly great timing.The Bank of England is expected to cut rates by 25 basis points on Thursday, as it prioritises weak growth over still high inflation. We do not expect a unanimous decision, but it is possible that MPC votes and communications will reflect the increased gloom brought about by Trump's trade war, opening the way for further cuts beyond those already priced in. RONThe all-time-low manufacturing PMI reading (46.1) adds to a list of rather uninspiring macroeconomic data points out of Romania (albeit the index is less than two years old, which makes the outlook less dramatic). Thursday will give us an insight into domestic demand, with a December retail sales reading, which should be far more important.Figure 2: Romania Manufacturing PMI (2023 - 2024) Source: NIS via Bloomberg, 03/02/2025The attention has once again shifted towards politics, however, with Calin Georgescu continuing his controversial campaign (his last week’s remarks included calling Ukraine a 'fictional state' and suggesting an annexation of its territories). A presidential re-run will take place in May, it is yet uncertain whether the previous winner – the aforementioned Georgescu – will be admitted to compete. HUFHUF did struggle as US tariffs got announced, but the sell-off has been a bit more limited than the rest of the CE-3, possibly due to the fact that it is already at low levels following a large depreciation last year, Hungary itself is more exposed to China (with optimism towards the Middle Kingdom improving as of late) and the MNB turned out to be relatively hawkish. The bank paused again and stressed that pro-inflationary risks have increased, suggesting that rates could remain higher for longer. Heightened geopolitical tensions and continued currency weakness may reduce the room for cuts, which might have given the currency a bit of a boost.Figure 3: MNB Reference Rate (2021 - 2025)Source: NIS via Bloomberg, 03/02/2025In March, however, we will likely see a change in the position of the bank's governor. György Matolcsy, conflicted with Orban, could be replaced by someone much more sympathetic to the Fidesz, which makes the direction of monetary policy hard to determine. If rates indeed remain elevated, the Hungarian currency may continue to be an attractive option from a carry trade perspective. PLNThe zloty’s wild ride, which put the currency at its strongest position against the euro in almost 7 years (EUR/PLN below 4.20), seems to be over, as Trump tariff threats start becoming reality. Due to the sell-off in EUR/USD, USD/PLN registered a particularly sharp uptick of over 1.5% – the biggest since Nov. 6, when Trump was confirmed to have won the elections and the aforementioned tariff threat became realistic. The zloty is likely to remain under pressure in the near term, in our view, weighed down by the threat of tariff imposition on the EU.Figure 4: Poland GDP [Annual] (2015 - 2024)

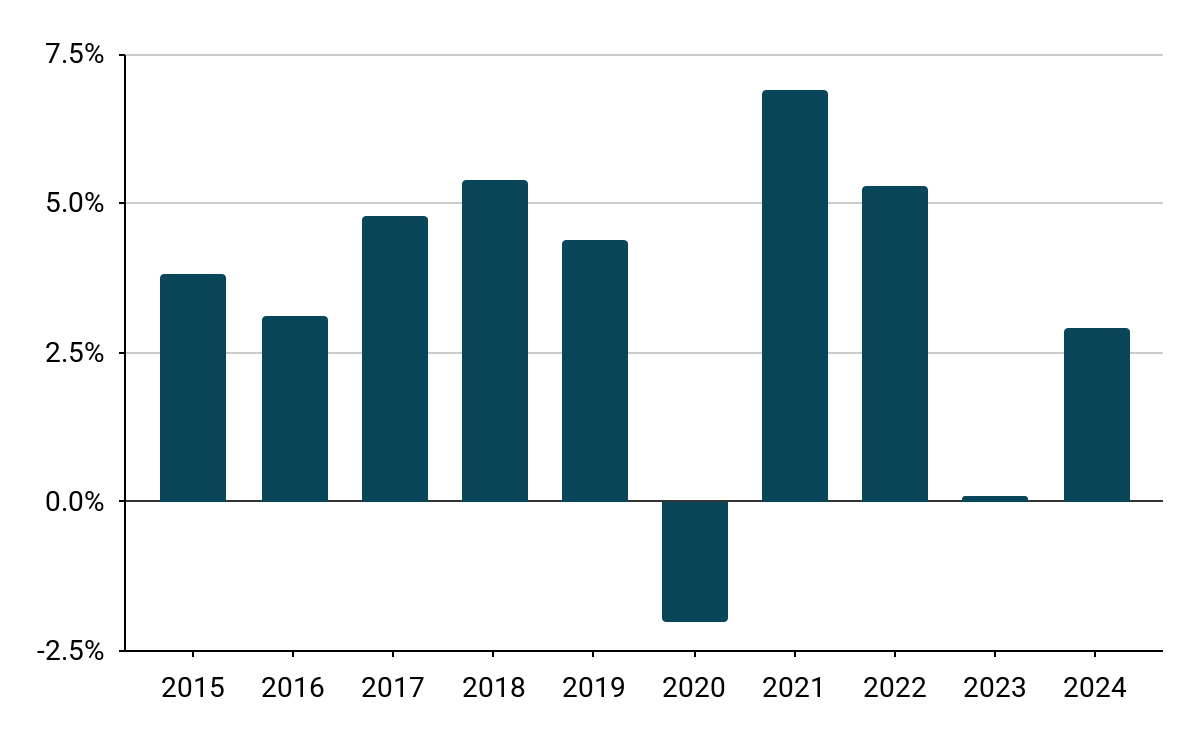

Source: NIS via Bloomberg, 03/02/2025The attention has once again shifted towards politics, however, with Calin Georgescu continuing his controversial campaign (his last week’s remarks included calling Ukraine a 'fictional state' and suggesting an annexation of its territories). A presidential re-run will take place in May, it is yet uncertain whether the previous winner – the aforementioned Georgescu – will be admitted to compete. HUFHUF did struggle as US tariffs got announced, but the sell-off has been a bit more limited than the rest of the CE-3, possibly due to the fact that it is already at low levels following a large depreciation last year, Hungary itself is more exposed to China (with optimism towards the Middle Kingdom improving as of late) and the MNB turned out to be relatively hawkish. The bank paused again and stressed that pro-inflationary risks have increased, suggesting that rates could remain higher for longer. Heightened geopolitical tensions and continued currency weakness may reduce the room for cuts, which might have given the currency a bit of a boost.Figure 3: MNB Reference Rate (2021 - 2025)Source: NIS via Bloomberg, 03/02/2025In March, however, we will likely see a change in the position of the bank's governor. György Matolcsy, conflicted with Orban, could be replaced by someone much more sympathetic to the Fidesz, which makes the direction of monetary policy hard to determine. If rates indeed remain elevated, the Hungarian currency may continue to be an attractive option from a carry trade perspective. PLNThe zloty’s wild ride, which put the currency at its strongest position against the euro in almost 7 years (EUR/PLN below 4.20), seems to be over, as Trump tariff threats start becoming reality. Due to the sell-off in EUR/USD, USD/PLN registered a particularly sharp uptick of over 1.5% – the biggest since Nov. 6, when Trump was confirmed to have won the elections and the aforementioned tariff threat became realistic. The zloty is likely to remain under pressure in the near term, in our view, weighed down by the threat of tariff imposition on the EU.Figure 4: Poland GDP [Annual] (2015 - 2024) Source: NIS via Bloomberg, 03/02/2025Last week confirmed that the Polish economy accelerated substantially in 2024, registering a somewhat higher-than-expected growth of 2.9%. This year is set to bring stronger and more balanced growth, but a tariff risk is looming in the background. This week will provide some domestic headlines as well, with NBP rate decisions scheduled for Wednesday. Any change in rates would be a major surprise, with attention again focused squarely on communications, particularly Governor Glapiński’s Thursday press conference. Aside from the typical, any insight into the MPC’s approach towards zloty’s recent strength as well as Trump’s tariffs and threats would be worth observing.

Source: NIS via Bloomberg, 03/02/2025Last week confirmed that the Polish economy accelerated substantially in 2024, registering a somewhat higher-than-expected growth of 2.9%. This year is set to bring stronger and more balanced growth, but a tariff risk is looming in the background. This week will provide some domestic headlines as well, with NBP rate decisions scheduled for Wednesday. Any change in rates would be a major surprise, with attention again focused squarely on communications, particularly Governor Glapiński’s Thursday press conference. Aside from the typical, any insight into the MPC’s approach towards zloty’s recent strength as well as Trump’s tariffs and threats would be worth observing.

Source: LSEG Datastream Date: 03/02/2025 GBPThe UK seems to be relatively low on the list of the Republican targets for tariffs, which means that sterling is performing better than other European currencies. Trump said over the weekend that the UK was ‘out of line’ with regards to its trade policies, although he also hinted that a deal could be reached that avoided the imposition of tariffs. Britain actually runs a decent trade surplus with the US, which could be used to sidestep import duties. The onus will be on Keir Starmer’s government to strike a deal, yet he will be in Brussels this week looking to ‘reset’ the UK’s relationship with the EU - not exactly great timing.The Bank of England is expected to cut rates by 25 basis points on Thursday, as it prioritises weak growth over still high inflation. We do not expect a unanimous decision, but it is possible that MPC votes and communications will reflect the increased gloom brought about by Trump's trade war, opening the way for further cuts beyond those already priced in. RONThe all-time-low manufacturing PMI reading (46.1) adds to a list of rather uninspiring macroeconomic data points out of Romania (albeit the index is less than two years old, which makes the outlook less dramatic). Thursday will give us an insight into domestic demand, with a December retail sales reading, which should be far more important.Figure 2: Romania Manufacturing PMI (2023 - 2024)Source: NIS via Bloomberg, 03/02/2025The attention has once again shifted towards politics, however, with Calin Georgescu continuing his controversial campaign (his last week’s remarks included calling Ukraine a 'fictional state' and suggesting an annexation of its territories). A presidential re-run will take place in May, it is yet uncertain whether the previous winner – the aforementioned Georgescu – will be admitted to compete. HUFHUF did struggle as US tariffs got announced, but the sell-off has been a bit more limited than the rest of the CE-3, possibly due to the fact that it is already at low levels following a large depreciation last year, Hungary itself is more exposed to China (with optimism towards the Middle Kingdom improving as of late) and the MNB turned out to be relatively hawkish. The bank paused again and stressed that pro-inflationary risks have increased, suggesting that rates could remain higher for longer. Heightened geopolitical tensions and continued currency weakness may reduce the room for cuts, which might have given the currency a bit of a boost.Figure 3: MNB Reference Rate (2021 - 2025)Source: NIS via Bloomberg, 03/02/2025In March, however, we will likely see a change in the position of the bank's governor. György Matolcsy, conflicted with Orban, could be replaced by someone much more sympathetic to the Fidesz, which makes the direction of monetary policy hard to determine. If rates indeed remain elevated, the Hungarian currency may continue to be an attractive option from a carry trade perspective. PLNThe zloty’s wild ride, which put the currency at its strongest position against the euro in almost 7 years (EUR/PLN below 4.20), seems to be over, as Trump tariff threats start becoming reality. Due to the sell-off in EUR/USD, USD/PLN registered a particularly sharp uptick of over 1.5% – the biggest since Nov. 6, when Trump was confirmed to have won the elections and the aforementioned tariff threat became realistic. The zloty is likely to remain under pressure in the near term, in our view, weighed down by the threat of tariff imposition on the EU.Figure 4: Poland GDP [Annual] (2015 - 2024)Source: NIS via Bloomberg, 03/02/2025Last week confirmed that the Polish economy accelerated substantially in 2024, registering a somewhat higher-than-expected growth of 2.9%. This year is set to bring stronger and more balanced growth, but a tariff risk is looming in the background. This week will provide some domestic headlines as well, with NBP rate decisions scheduled for Wednesday. Any change in rates would be a major surprise, with attention again focused squarely on communications, particularly Governor Glapiński’s Thursday press conference. Aside from the typical, any insight into the MPC’s approach towards zloty’s recent strength as well as Trump’s tariffs and threats would be worth observing.