Dollar pull back gather speed as tariff threat fades

A "tariff relief" rally gathered speed last week, as Trump's flurry of initial activity and executive orders seem to be focused elsewhere for now, and markets hope that their worst fears on tariffs will not be realised.

FX Market Updates

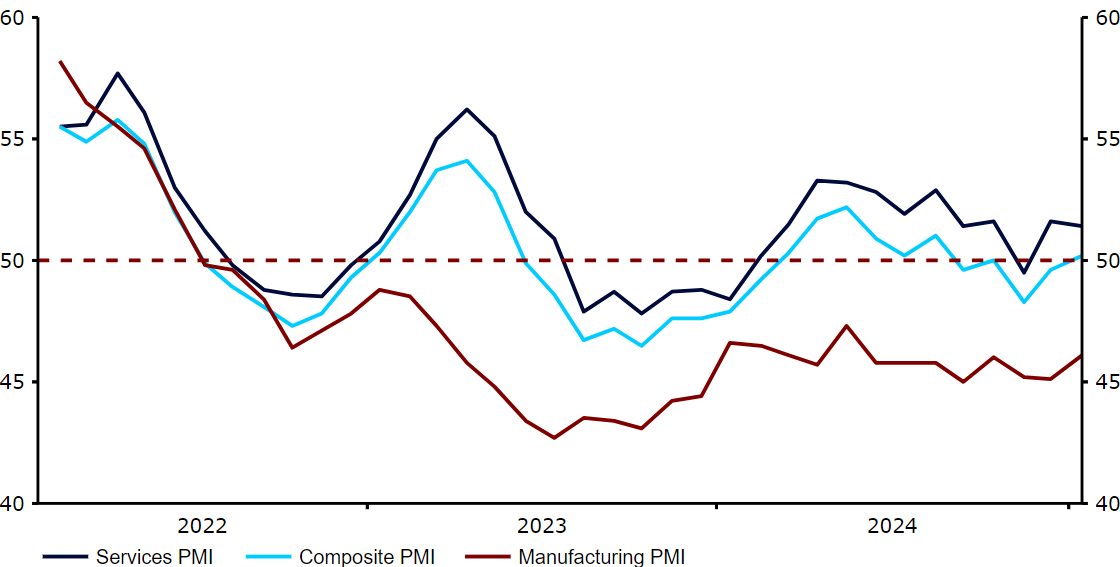

A "tariff relief" rally gathered speed last week, as Trump's flurry of initial activity and executive orders seem to be focused elsewhere for now, and markets hope that their worst fears on tariffs will not be realised.The rally in almost every G10 currency against the dollar was led by the pound. EM currencies were supported by Trump’s hint of modest tariffs on China suggesting that the hit to global growth may be less significant than feared. Latin American currencies were given the biggest leg up, although uncertainty remains high after Trump ordered tariffs specifically targeting Colombia in retaliation for president Petro’s decision to turn away migrant repatriation flights from the US. While these tariff threats have since been revoked, the spat is a reminder that the situation is very fluid, and that Trump's decisions can have as much, or more, of an impact as economic news or a Fed rate move.This week would ordinarily have been dominated by the January meetings of the two most important central banks in the world, the Federal Reserve and the ECB. However, the mercurial Trump administration is liable to steal the spotlight with a sudden tariff decision. We will stick to predicting the predictable and, in this case, there is little doubt about the outcome of both central bank meetings: a cut from the ECB and no change from the Fed. USDThe holiday shortened week in the US yielded little to change our macroeconomic forecasts in either direction, although a weaker than expected PMI release did help currencies worldwide rally against the dollar. Yet, fears of Trump's tariffs remain the main driver of currency markets. For now, the onslaught of executive orders has yet to result in any tariff increases, which has calmed nerves somewhat, as has hints of no more than 10% trade duties on China.This week’s Federal Reserve meeting could be overlooked by market participants. Futures markets are assigning effectively no chance of another rate reduction on Wednesday, and we wholeheartedly agree. For now, we expect the FOMC to adopt a patient approach, as it awaits more details of Trump’s tariff and tax plans before it delivers any concrete guidance. EURThe Eurozone also saw an improvement in the PMIs last week, albeit a more moderate one than in the UK. This was, however, enough to push the composite index just above the 50 level, back to signalling modest levels of growth. The increase was a slight one, but market positioning and consensus for a stronger dollar is so widespread that even the tenderest green shoots in Europe are enough to bring about significant countertrend moves, and the euro is now up for the year against the dollar.The key for the common currency this week will be the European Central Bank meeting on Thursday. As another rate cut is expected, and fully priced in, we will be paying close attention to the Council’s communications and president Lagarde’s press conference for hints on what ECB members see as a likely terminal level for interest rates in this cutting cycle.Figure 1: Euro Area PMIs (2022 - 2025)

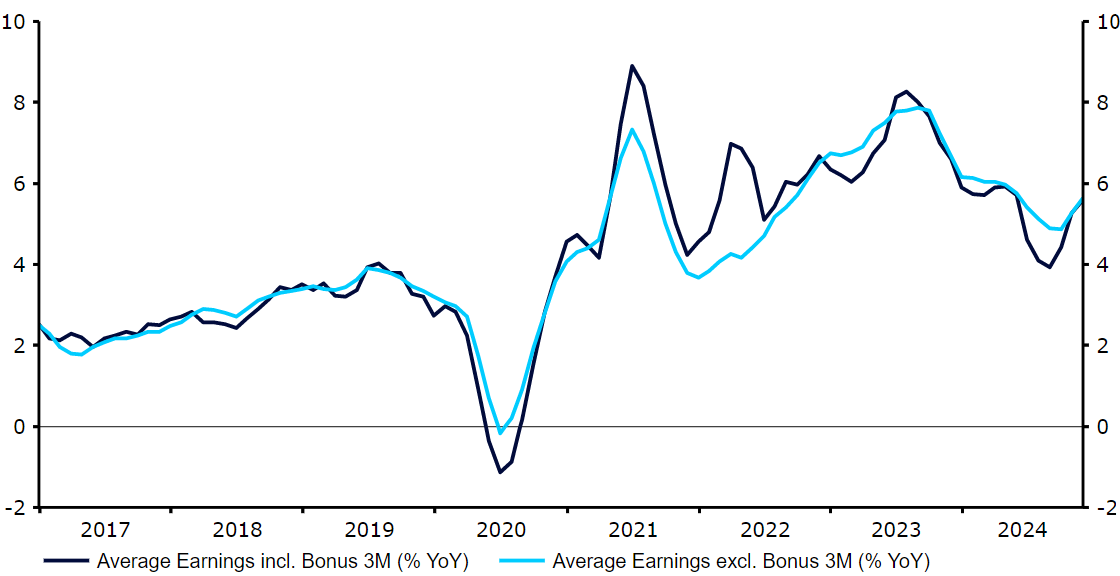

USDThe holiday shortened week in the US yielded little to change our macroeconomic forecasts in either direction, although a weaker than expected PMI release did help currencies worldwide rally against the dollar. Yet, fears of Trump's tariffs remain the main driver of currency markets. For now, the onslaught of executive orders has yet to result in any tariff increases, which has calmed nerves somewhat, as has hints of no more than 10% trade duties on China.This week’s Federal Reserve meeting could be overlooked by market participants. Futures markets are assigning effectively no chance of another rate reduction on Wednesday, and we wholeheartedly agree. For now, we expect the FOMC to adopt a patient approach, as it awaits more details of Trump’s tariff and tax plans before it delivers any concrete guidance. EURThe Eurozone also saw an improvement in the PMIs last week, albeit a more moderate one than in the UK. This was, however, enough to push the composite index just above the 50 level, back to signalling modest levels of growth. The increase was a slight one, but market positioning and consensus for a stronger dollar is so widespread that even the tenderest green shoots in Europe are enough to bring about significant countertrend moves, and the euro is now up for the year against the dollar.The key for the common currency this week will be the European Central Bank meeting on Thursday. As another rate cut is expected, and fully priced in, we will be paying close attention to the Council’s communications and president Lagarde’s press conference for hints on what ECB members see as a likely terminal level for interest rates in this cutting cycle.Figure 1: Euro Area PMIs (2022 - 2025) Source: LSEG Datastream Date: 27/01/2025 GBPMacroeconomic news flow turned positive for sterling last week. A solid labour report was followed by an encouraging uptick in the PMIs of business activity for January. Both the manufacturing and the services subindices posted gains, and the composite index is now consistent with solid, if unspectacular, growth.The pound reacted well to the news, posting strong gains against every single G10 currency to end at the top of the currency performance table for the week. An attractive valuation, the prospect of a better relationship with the European Union and relative isolation from the threat of Trump's tariffs are all significant positives for the pound at these levels. Yet, downside risks remain, most notably the threat of a worsening in labour market conditions following Labour’s employer tax hikes. Indeed, the details of the PMI surveys showed that businesses are now slashing jobs at the fastest pace since the GFC, once the pandemic period is excluded.Figure 2: UK Wage Growth (2017 - 2024)

Source: LSEG Datastream Date: 27/01/2025 GBPMacroeconomic news flow turned positive for sterling last week. A solid labour report was followed by an encouraging uptick in the PMIs of business activity for January. Both the manufacturing and the services subindices posted gains, and the composite index is now consistent with solid, if unspectacular, growth.The pound reacted well to the news, posting strong gains against every single G10 currency to end at the top of the currency performance table for the week. An attractive valuation, the prospect of a better relationship with the European Union and relative isolation from the threat of Trump's tariffs are all significant positives for the pound at these levels. Yet, downside risks remain, most notably the threat of a worsening in labour market conditions following Labour’s employer tax hikes. Indeed, the details of the PMI surveys showed that businesses are now slashing jobs at the fastest pace since the GFC, once the pandemic period is excluded.Figure 2: UK Wage Growth (2017 - 2024) Source: LSEG Datastream Date: 27/01/2025 RONAlthough industrial production data for November did not impress (a monthly decline, mainly due to the high October base), its growth rate is still impressive compared to other European countries (5.2% YoY in real terms). Hard macroeconomic data points to rather healthy levels of growth, which should be confirmed on Valentine's Day, the 14th of February.Figure 3: Romania Industrial Sales (2022 - 2025)

Source: LSEG Datastream Date: 27/01/2025 RONAlthough industrial production data for November did not impress (a monthly decline, mainly due to the high October base), its growth rate is still impressive compared to other European countries (5.2% YoY in real terms). Hard macroeconomic data points to rather healthy levels of growth, which should be confirmed on Valentine's Day, the 14th of February.Figure 3: Romania Industrial Sales (2022 - 2025)

USDThe holiday shortened week in the US yielded little to change our macroeconomic forecasts in either direction, although a weaker than expected PMI release did help currencies worldwide rally against the dollar. Yet, fears of Trump's tariffs remain the main driver of currency markets. For now, the onslaught of executive orders has yet to result in any tariff increases, which has calmed nerves somewhat, as has hints of no more than 10% trade duties on China.This week’s Federal Reserve meeting could be overlooked by market participants. Futures markets are assigning effectively no chance of another rate reduction on Wednesday, and we wholeheartedly agree. For now, we expect the FOMC to adopt a patient approach, as it awaits more details of Trump’s tariff and tax plans before it delivers any concrete guidance. EURThe Eurozone also saw an improvement in the PMIs last week, albeit a more moderate one than in the UK. This was, however, enough to push the composite index just above the 50 level, back to signalling modest levels of growth. The increase was a slight one, but market positioning and consensus for a stronger dollar is so widespread that even the tenderest green shoots in Europe are enough to bring about significant countertrend moves, and the euro is now up for the year against the dollar.The key for the common currency this week will be the European Central Bank meeting on Thursday. As another rate cut is expected, and fully priced in, we will be paying close attention to the Council’s communications and president Lagarde’s press conference for hints on what ECB members see as a likely terminal level for interest rates in this cutting cycle.Figure 1: Euro Area PMIs (2022 - 2025)Source: LSEG Datastream Date: 27/01/2025 GBPMacroeconomic news flow turned positive for sterling last week. A solid labour report was followed by an encouraging uptick in the PMIs of business activity for January. Both the manufacturing and the services subindices posted gains, and the composite index is now consistent with solid, if unspectacular, growth.The pound reacted well to the news, posting strong gains against every single G10 currency to end at the top of the currency performance table for the week. An attractive valuation, the prospect of a better relationship with the European Union and relative isolation from the threat of Trump's tariffs are all significant positives for the pound at these levels. Yet, downside risks remain, most notably the threat of a worsening in labour market conditions following Labour’s employer tax hikes. Indeed, the details of the PMI surveys showed that businesses are now slashing jobs at the fastest pace since the GFC, once the pandemic period is excluded.Figure 2: UK Wage Growth (2017 - 2024)Source: LSEG Datastream Date: 27/01/2025 RONAlthough industrial production data for November did not impress (a monthly decline, mainly due to the high October base), its growth rate is still impressive compared to other European countries (5.2% YoY in real terms). Hard macroeconomic data points to rather healthy levels of growth, which should be confirmed on Valentine's Day, the 14th of February.Figure 3: Romania Industrial Sales (2022 - 2025)