Risk assets continue to rally in spite of Russia - Ukraine war, hawkish Fed

Stock markets and risk assets generally posted impressive moves last week, discounting the impact of the Russian invasion of Ukraine and treating Fed hawkishness as a case of "buy the rumour, sell the news".

FX Market Updates

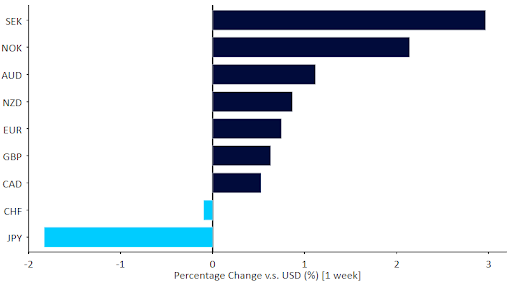

Stock markets and risk assets generally posted impressive moves last week, discounting the impact of the Russian invasion of Ukraine and treating Fed hawkishness as a case of "buy the rumour, sell the news".As an example of the optimism pervading financial markets, European stock indices closed the week at essentially the level they were the day of the invasion. In currency markets, the Swedish krona was the best performer of the week, with the safe-haven Japanese yen at the bottom of the G10 rankings. Emerging markets continue to post gains, with Latin American currencies benefiting particularly from their commodity exporting economies and the distance from the war. We note that our favourite, the Brazilian real, tops the performance tables among all major currencies so far this year, up well over 10% against the dollar.Focus this week will be on the Thursday release of the Eurozone and UK PMIs (now renamed S&P) indices of business activity. They are the first ones to reflect the impact of the invasion of Ukraine, so uncertainty is unusually high, but market consensus expects a retracement towards still highly expansionary levels. Aside from that, no fewer than six Federal Reserve officials are scheduled to speak this week. We expect them to clarify the timing and extent of hikes in what looks like a very front-loaded tightening cycle out of the US, though so far the dollar has conspicuously failed to benefit from the Fed hawkish communications last week. Finally, the UK February inflation report on Wednesday should see yet another jump to a fresh multi-decade record.Figure 1: G10 FX Performance Tracker (1 week)

GBP

The Bank of England delivered yet another head fake to markets at its March meeting last Thursday. Though it hiked rates as expected, there was one dovish dissent and the statement was revised in a decidedly dovish direction. We would not overreact to this change, as the MPC communications have been quite erratic during this tightening cycle, but it warrants revising some of our optimism on sterling downwards.We expect another strong inflation report out of the UK on Wednesday, with fresh 30-year records printed in both the core and headline numbers, which should further puzzle traders about the Bank of England's apparent dovish turn last week.EUR

A quiet week in the Eurozone, with only a lagged report on industrial production from January, and a massive though expected fall in investors expectations for future growth after the shock of the Russian invasion. The latter index has not been particularly useful in predicting growth lately, but it bears noting.The common currency had a volatile week but managed to rally and end up solidly above the 1.10 level versus the US dollar. ECB President Lagarde and chief economist Philip Lane are both scheduled to speak this week, but the main event will be the release of the flash PMI numbers for March, a first look at the stagflationary impact of the war on the European economy.USD

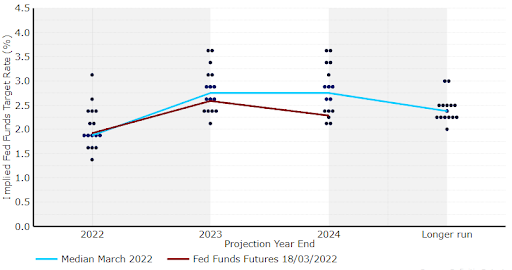

The Federal Reserve validated expectations for a hike in every remaining meeting in 2022 last week, with its ‘dot plot’ suggesting members expect seven 25 basis point hikes this year. Its long term forecasts were more dovish, but given its forecasting track record we would not place too much store in those.The failure of the dollar to rally in the wake of the meeting is due to two factors. First, the general increase in risk appetite, which hurt the dollar, as it has acted as a safe-haven since the Ukraine invasion started. Second, a sense by markets that at current levels a lot is in the price already, and upside may be limited from here. This week we should see some clarification as to which one of these factors dominates.Figure 2: FOMC Dot Plot [March 2022]