Rising US rates buoy dollar, but Euro resilient on hawkish ECB turn

The sell-off in US fixed income is now spreading to other markets, with European yields moving higher as the long-awaited (by us, at least) hawkish turn in ECB communications begins to take place.

FX Market Updates

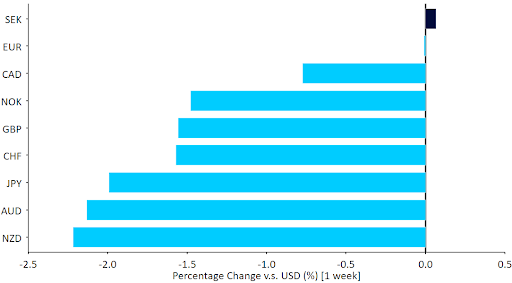

The relentless march towards higher rates in the US continued last week.The key 10-year Treasury rate rose another 6 basis points to end the week above 2.90%. The sell-off in US fixed income is now spreading to other markets, with European yields moving higher as the long-awaited (by us, at least) hawkish turn in ECB communications begins to take place. On the back of this shift, the euro managed to hang on to the dollar and rally against all other G10 currencies, save the Swedish krona. Commodity and emerging market currencies had a rough go of it as the massive increase in rates worldwide begins to take its toll on risk assets and dent the rally in commodity prices.  Over the weekend, Emmanuel Macron was re-elected as French president which, together with reports that the ECB is ready to move more aggressively in response to inflation, should be supporting the common currency. We have, however, seen a sharp sell-off in risk assets so far this morning at the expense of the safe havens, particularly the US dollar and Japanese yen. Investors are fretting over the possibility of a slowdown in global growth in response to fresh concerns over additional lockdowns in China and tighter monetary policy globally. Investor risk appetite looks likely to remain the main driver of currencies in the coming days. On the data front, the April flash inflation report in the Eurozone on Thursday is shaping up to be a key event of the trading week, though we will also see a slew of growth and inflation data points out of the US. An upward surprise in Eurozone inflation could see the headline number dangerously close to 8%. We think that this would help the case for a July hike, forcing further repricing of European rates and helping the common currency along.Figure 1: G10 FX Performance Tracker [base: USD] (1 week)

Over the weekend, Emmanuel Macron was re-elected as French president which, together with reports that the ECB is ready to move more aggressively in response to inflation, should be supporting the common currency. We have, however, seen a sharp sell-off in risk assets so far this morning at the expense of the safe havens, particularly the US dollar and Japanese yen. Investors are fretting over the possibility of a slowdown in global growth in response to fresh concerns over additional lockdowns in China and tighter monetary policy globally. Investor risk appetite looks likely to remain the main driver of currencies in the coming days. On the data front, the April flash inflation report in the Eurozone on Thursday is shaping up to be a key event of the trading week, though we will also see a slew of growth and inflation data points out of the US. An upward surprise in Eurozone inflation could see the headline number dangerously close to 8%. We think that this would help the case for a July hike, forcing further repricing of European rates and helping the common currency along.Figure 1: G10 FX Performance Tracker [base: USD] (1 week)

Over the weekend, Emmanuel Macron was re-elected as French president which, together with reports that the ECB is ready to move more aggressively in response to inflation, should be supporting the common currency. We have, however, seen a sharp sell-off in risk assets so far this morning at the expense of the safe havens, particularly the US dollar and Japanese yen. Investors are fretting over the possibility of a slowdown in global growth in response to fresh concerns over additional lockdowns in China and tighter monetary policy globally. Investor risk appetite looks likely to remain the main driver of currencies in the coming days. On the data front, the April flash inflation report in the Eurozone on Thursday is shaping up to be a key event of the trading week, though we will also see a slew of growth and inflation data points out of the US. An upward surprise in Eurozone inflation could see the headline number dangerously close to 8%. We think that this would help the case for a July hike, forcing further repricing of European rates and helping the common currency along.Figure 1: G10 FX Performance Tracker [base: USD] (1 week)GBP

Weak numbers across the board last week helped sink the pound below the 1.30 level against the dollar. Retail sales, consumer confidence, and the PMIs of business activity were all weaker than expected, and the Bank of England´s muddled communications about its response to the inflationary wave are not helping. We note, however, that the PMIs are still consistent with strong growth and the economy is at or very near full employment, and we regard the latest move lower in sterling as a significant overreaction.This week sees no significant macroeconomic news and the Bank of England has entered its pre-meeting blackout period, so expect the pound to trade off events elsewhere.EUR

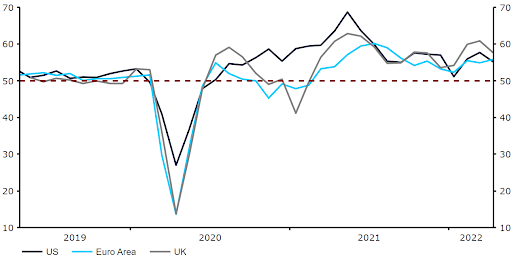

In spite of the volatility, the outlook turned somewhat more positive for the euro last week. The April PMIs were better than expected, suggesting that the Eurozone economy is weathering the impact of the Ukraine war rather well. Just as importantly, rhetoric out of the ECB has taken a hawkish turn. Remarks from both De Guindos and President Lagarde last week suggest that a July hike is possible, with both policymakers sounding increasingly alarmed by inflationary pressures.The April flash inflation print out on Thursday could seal the case for a July hike; a headline number near 8% is definitely possible, and the march higher in the core index should continue, making it increasingly difficult to blame the spike in energy prices.Figure 2: G3 PMIs (2019 - 2022)