Latin America FX Forecast Revision - July 2020

Read our latest analysis of the Latin America currencies: Brazilian Real (BRL), Mexican Peso (MXN), Chilean Peso (CLP), Peruvian New Sol (PEN) and Colombian Peso (COP).

FX Market Updates

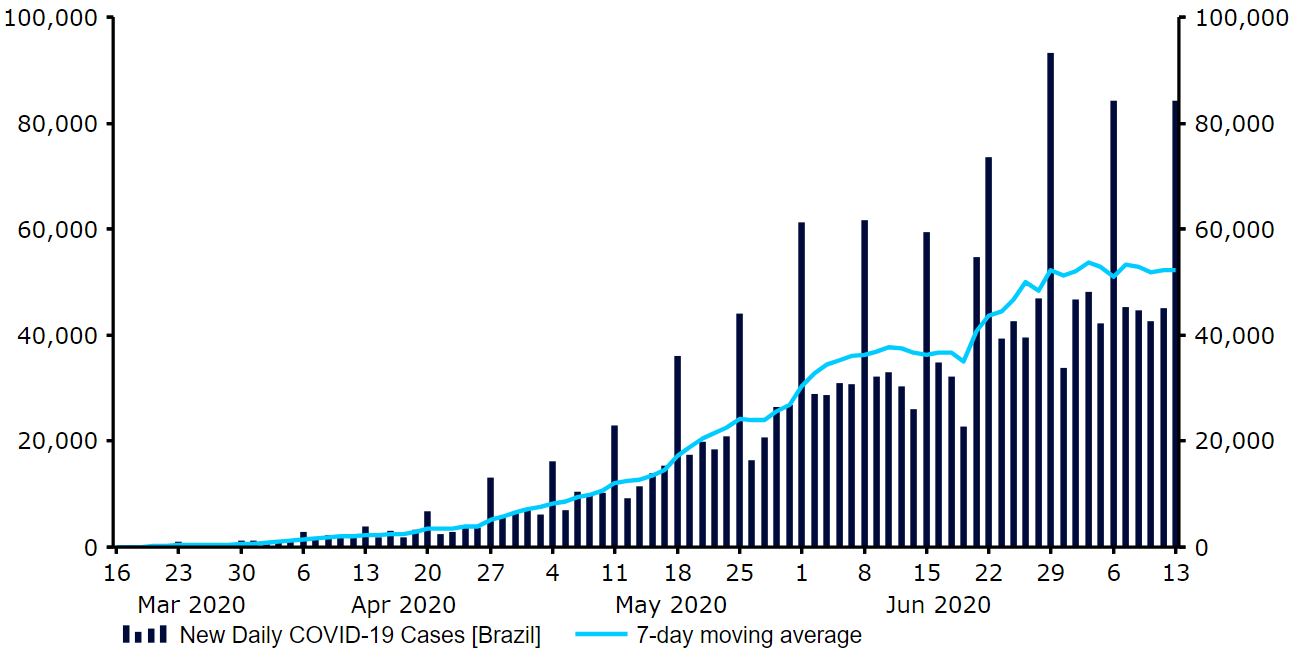

Find below our latest analysis of the Latin America currencies: Brazilian Real (BRL), Mexican Peso (MXN), Chilean Peso (CLP), Peruvian New Sol (PEN) and Colombian Peso (COP). Source: Refinitiv Datastream Date: 14/07/2020Ongoing political unrest in Brazil and criticism of authorities’ handling of the pandemic has significantly soured sentiment towards the real so far in 2020 and has been behind much of the currency’s underperformance. Far-right President Jair Bolsonaro has, like many of his predecessors, faced allegations of corruption in the last few months that have resulted in calls for his impeachment. Until recently, investors were compensated for Brazil’s heightened political risk premium by the country’s very high real interest rates, which peaked at almost 8% in 2017. A series of interest rate cuts from the Central Bank of Brazil so far this year in response to the crisis has, however, significantly lowered the currency’s appeal. Rates have been slashed by a total of 200 basis points since the onset of the pandemic to 2.25%, which has significantly dented Brazil’s appeal from a carry trade perspective. Even more troubling for investors has been the President’s approach to dealing with the COVID-19 virus outbreak. Bolsonaro has actively encouraged people to defy social distancing, ignore regional lockdown and partake in large gatherings. Brazil has racked up the second largest number of reported cases of the virus in the world and over 70,000 deaths at the time of writing - numbers that are likely much higher in reality due to very limited levels of testing. The country remains in the high growth phase of the virus, at a time when healthcare systems in some of the worst affected regions are already reportedly approaching full capacity. Reports that the majority of the population in some of Brazil’s largest cities, including Sao Paulo, are ignoring isolation orders is unlikely to help suppress the spread of the virus at the rate that we have witnessed across much of the rest of the world. An inability to rein in the number of new infections could lead to an even more severe recession in Brazil this year, in our view.Figure 2: New Daily COVID-19 Cases [Brazil] (March ‘20 - July ‘20)

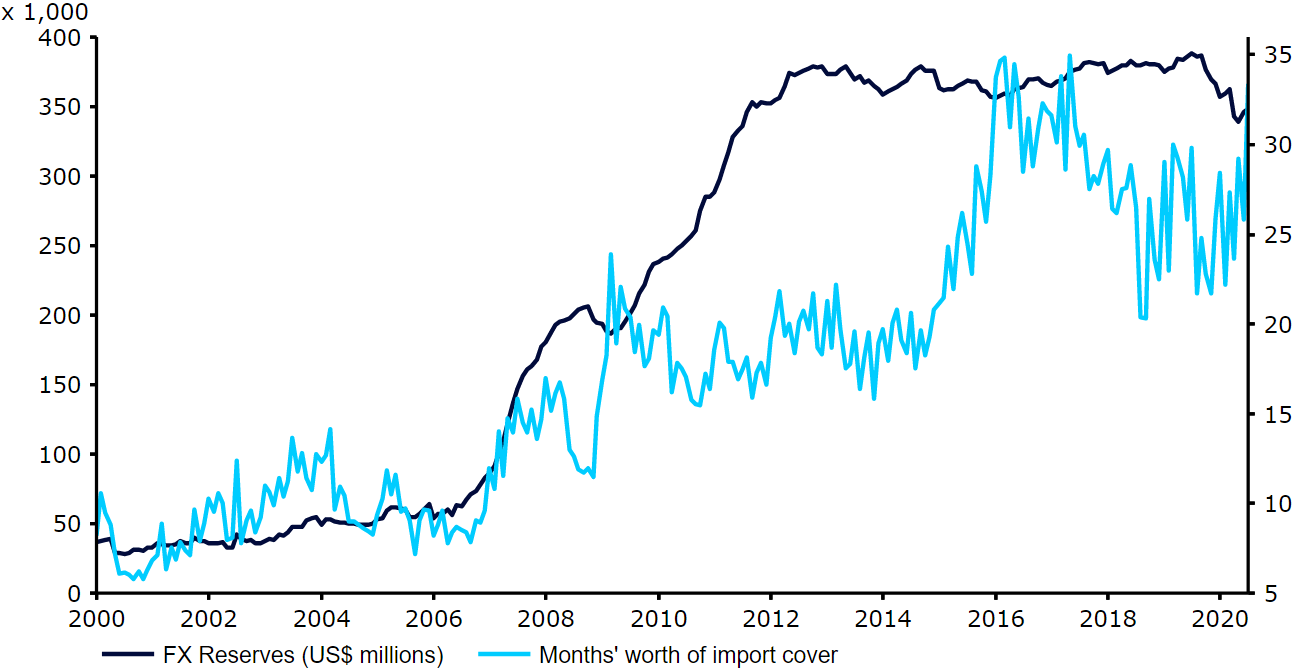

Source: Refinitiv Datastream Date: 14/07/2020Ongoing political unrest in Brazil and criticism of authorities’ handling of the pandemic has significantly soured sentiment towards the real so far in 2020 and has been behind much of the currency’s underperformance. Far-right President Jair Bolsonaro has, like many of his predecessors, faced allegations of corruption in the last few months that have resulted in calls for his impeachment. Until recently, investors were compensated for Brazil’s heightened political risk premium by the country’s very high real interest rates, which peaked at almost 8% in 2017. A series of interest rate cuts from the Central Bank of Brazil so far this year in response to the crisis has, however, significantly lowered the currency’s appeal. Rates have been slashed by a total of 200 basis points since the onset of the pandemic to 2.25%, which has significantly dented Brazil’s appeal from a carry trade perspective. Even more troubling for investors has been the President’s approach to dealing with the COVID-19 virus outbreak. Bolsonaro has actively encouraged people to defy social distancing, ignore regional lockdown and partake in large gatherings. Brazil has racked up the second largest number of reported cases of the virus in the world and over 70,000 deaths at the time of writing - numbers that are likely much higher in reality due to very limited levels of testing. The country remains in the high growth phase of the virus, at a time when healthcare systems in some of the worst affected regions are already reportedly approaching full capacity. Reports that the majority of the population in some of Brazil’s largest cities, including Sao Paulo, are ignoring isolation orders is unlikely to help suppress the spread of the virus at the rate that we have witnessed across much of the rest of the world. An inability to rein in the number of new infections could lead to an even more severe recession in Brazil this year, in our view.Figure 2: New Daily COVID-19 Cases [Brazil] (March ‘20 - July ‘20) Source: Refinitiv Datastream Date: 14/07/2020There is some good news in Brazil’s solid macroeconomic fundamentals. From a fundamental perspective, we think BRL is one of the better placed EM currencies to weather additional losses:High FX reserves that equate to almost 30 months’ worth of import cover. This is an ample level of ammunition for the Central Bank of Brazil to successfully intervene in the market in order to reverse the currency’s sell-off. Central bank President Roberto Campos Neto stated in May that the bank had plenty of room to intervene and may step up its efforts to support the currency, should it deem necessary. Figure 3: Brazil FX Reserves (2000 - 2020)

Source: Refinitiv Datastream Date: 14/07/2020There is some good news in Brazil’s solid macroeconomic fundamentals. From a fundamental perspective, we think BRL is one of the better placed EM currencies to weather additional losses:High FX reserves that equate to almost 30 months’ worth of import cover. This is an ample level of ammunition for the Central Bank of Brazil to successfully intervene in the market in order to reverse the currency’s sell-off. Central bank President Roberto Campos Neto stated in May that the bank had plenty of room to intervene and may step up its efforts to support the currency, should it deem necessary. Figure 3: Brazil FX Reserves (2000 - 2020) Source: Refinitiv Datastream Date: 14/07/2020Low levels of external debt that equate to approximately 18% of GDP - among the lowest in South America. The recent sharp depreciation in BRL does, however, increase the real value of the debt payments. A manageable, albeit rising, current account deficit. This deficit increased to 2.7% of GDP in 2019, although remained comfortably financed by foreign direct investment (FDI).Depreciation in FX does not seem to be filtering through to higher inflation, so an inflationary spiral in which currency depreciation feeds on itself seems unlikely.Given the above supportive factors, and our view that the currency is very cheap at current levels, we do not think that a continued sell-off in the real at the rate witnessed since the onset of the crisis is likely in the long-term. We are instead continuing to pencil in a recovery for the currency against the dollar through to the end of 2021, and think that Brazil’s solid macroeconomic fundamentals should allow the currency to successfully bounce back once the worst of the crisis is over. The main issue for the real is, of course, the extent to which Brazil is able to contain the spread of the COVID-19 virus. An inability to do so relative to most of the rest of the world, and subsequent economic damage that this would cause, presents itself as a significant downside risk to our outlook.

Source: Refinitiv Datastream Date: 14/07/2020Low levels of external debt that equate to approximately 18% of GDP - among the lowest in South America. The recent sharp depreciation in BRL does, however, increase the real value of the debt payments. A manageable, albeit rising, current account deficit. This deficit increased to 2.7% of GDP in 2019, although remained comfortably financed by foreign direct investment (FDI).Depreciation in FX does not seem to be filtering through to higher inflation, so an inflationary spiral in which currency depreciation feeds on itself seems unlikely.Given the above supportive factors, and our view that the currency is very cheap at current levels, we do not think that a continued sell-off in the real at the rate witnessed since the onset of the crisis is likely in the long-term. We are instead continuing to pencil in a recovery for the currency against the dollar through to the end of 2021, and think that Brazil’s solid macroeconomic fundamentals should allow the currency to successfully bounce back once the worst of the crisis is over. The main issue for the real is, of course, the extent to which Brazil is able to contain the spread of the COVID-19 virus. An inability to do so relative to most of the rest of the world, and subsequent economic damage that this would cause, presents itself as a significant downside risk to our outlook.

Brazilian Real BRL

The Brazilian real (BRL) has been one the worst performing major currencies in the world since the rapid spread of the COVID-19 virus turned it into a full-blown pandemic.The currency has lost around one-fifth of its value versus the US dollar since the beginning of March (Figure 1), as investors flocked to low beta assets and sold those deemed as higher risk. This sell-off sent the currency to its lowest ever level at just shy of 6 to the USD, although it has since recovered some of these losses.Figure 1: USD/BRL (July ‘19 - July ‘20)Source: Refinitiv Datastream Date: 14/07/2020Ongoing political unrest in Brazil and criticism of authorities’ handling of the pandemic has significantly soured sentiment towards the real so far in 2020 and has been behind much of the currency’s underperformance. Far-right President Jair Bolsonaro has, like many of his predecessors, faced allegations of corruption in the last few months that have resulted in calls for his impeachment. Until recently, investors were compensated for Brazil’s heightened political risk premium by the country’s very high real interest rates, which peaked at almost 8% in 2017. A series of interest rate cuts from the Central Bank of Brazil so far this year in response to the crisis has, however, significantly lowered the currency’s appeal. Rates have been slashed by a total of 200 basis points since the onset of the pandemic to 2.25%, which has significantly dented Brazil’s appeal from a carry trade perspective. Even more troubling for investors has been the President’s approach to dealing with the COVID-19 virus outbreak. Bolsonaro has actively encouraged people to defy social distancing, ignore regional lockdown and partake in large gatherings. Brazil has racked up the second largest number of reported cases of the virus in the world and over 70,000 deaths at the time of writing - numbers that are likely much higher in reality due to very limited levels of testing. The country remains in the high growth phase of the virus, at a time when healthcare systems in some of the worst affected regions are already reportedly approaching full capacity. Reports that the majority of the population in some of Brazil’s largest cities, including Sao Paulo, are ignoring isolation orders is unlikely to help suppress the spread of the virus at the rate that we have witnessed across much of the rest of the world. An inability to rein in the number of new infections could lead to an even more severe recession in Brazil this year, in our view.Figure 2: New Daily COVID-19 Cases [Brazil] (March ‘20 - July ‘20)Source: Refinitiv Datastream Date: 14/07/2020There is some good news in Brazil’s solid macroeconomic fundamentals. From a fundamental perspective, we think BRL is one of the better placed EM currencies to weather additional losses:High FX reserves that equate to almost 30 months’ worth of import cover. This is an ample level of ammunition for the Central Bank of Brazil to successfully intervene in the market in order to reverse the currency’s sell-off. Central bank President Roberto Campos Neto stated in May that the bank had plenty of room to intervene and may step up its efforts to support the currency, should it deem necessary. Figure 3: Brazil FX Reserves (2000 - 2020)Source: Refinitiv Datastream Date: 14/07/2020Low levels of external debt that equate to approximately 18% of GDP - among the lowest in South America. The recent sharp depreciation in BRL does, however, increase the real value of the debt payments. A manageable, albeit rising, current account deficit. This deficit increased to 2.7% of GDP in 2019, although remained comfortably financed by foreign direct investment (FDI).Depreciation in FX does not seem to be filtering through to higher inflation, so an inflationary spiral in which currency depreciation feeds on itself seems unlikely.Given the above supportive factors, and our view that the currency is very cheap at current levels, we do not think that a continued sell-off in the real at the rate witnessed since the onset of the crisis is likely in the long-term. We are instead continuing to pencil in a recovery for the currency against the dollar through to the end of 2021, and think that Brazil’s solid macroeconomic fundamentals should allow the currency to successfully bounce back once the worst of the crisis is over. The main issue for the real is, of course, the extent to which Brazil is able to contain the spread of the COVID-19 virus. An inability to do so relative to most of the rest of the world, and subsequent economic damage that this would cause, presents itself as a significant downside risk to our outlook.