Gulf Currencies Market Update - June 2021

The COVID-19 pandemic has presented a challenging period for the gulf currencies, particularly following the slump in oil prices at the start of the crisis. Read our Special Report to find out what to expect from SAR, AED, QAR, OMR, BHD, AED, KWD, EGP, and TRY.

FX Market Updates

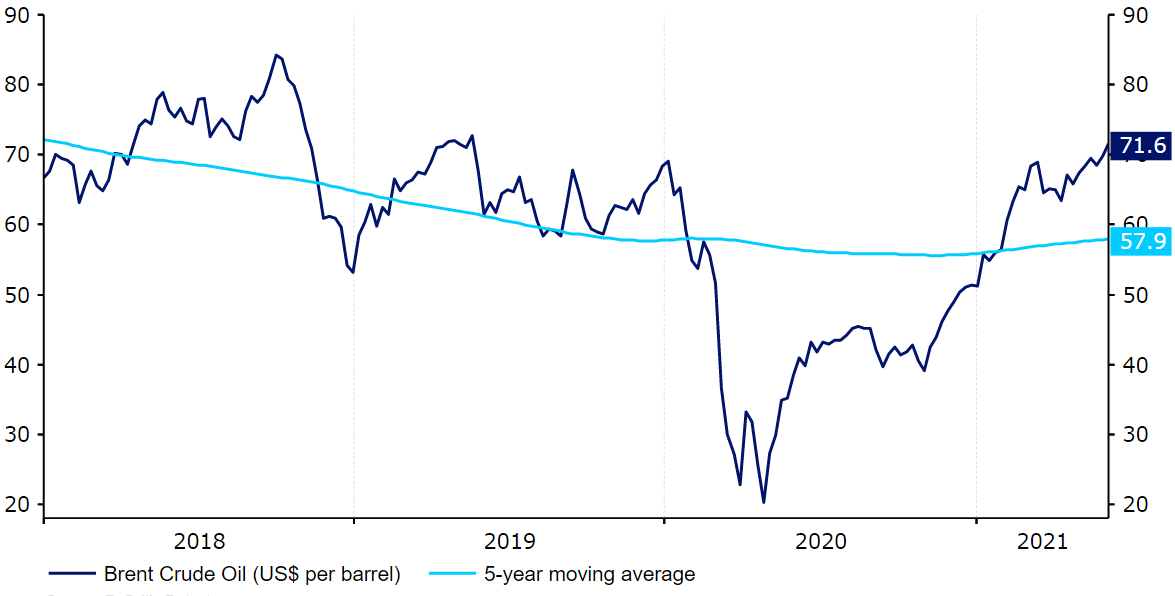

The COVID-19 pandemic has presented a challenging period for the gulf currencies, particularly following the slump in oil prices at the start of the crisis.Crude oil futures tumbled to record lows in April 2020 as lockdowns around the world sapped demand for commodities. This put pressure on the currency pegs in the Gulf Cooperation Council (GCC) and rekindled bets among some investors that one or two of these pegs were at risk of being ditched. The Omani riyal, for instance, fell to an all-time low against the dollar in the forward market, with ratings agency Standard & Poor’s cutting the country’s outlook and warning that confidence in the currency’s peg could diminish.The situation has taken a dramatic turn for the better since then. The rapid rollout of the various COVID-19 vaccines around the world fuelled hopes of a swift recovery in the global economy and has contributed to the sharp uptrend in oil prices - Brent crude oil futures are now back up to around $70 a barrel at the time of writing. While this remains below the breakeven oil price for some GCC nations, the minimum price required for spending needs to be met while balancing its state budget, pressure on the pegs has dramatically lessened. We now see little to no risk at all that any of them will be abandoned any time soon.Figure 1: Global Brent Crude Oil Futures (2018 - 2021) Source: Refinitiv Datastream Date: 08/06/2021We have outlined in this report our view as to the vulnerability of each peg to devaluation. We believe that this vulnerability depends heavily on both the ability of the country’s central bank to defend the peg and also the suitability of the exchange rate for each country’s domestic economy. The key factors that we look at in considering each currency’s vulnerability are:

Source: Refinitiv Datastream Date: 08/06/2021We have outlined in this report our view as to the vulnerability of each peg to devaluation. We believe that this vulnerability depends heavily on both the ability of the country’s central bank to defend the peg and also the suitability of the exchange rate for each country’s domestic economy. The key factors that we look at in considering each currency’s vulnerability are:

*as of 2019 We have outlined below the rationale for our assigned evaluation likelihoods for each of the six currencies in the GCC. We have also included our latest forecasts for both the Egyptian pound and Turkish lira, two nations that have close ties with the economies in the GCC.  Source: Refinitiv Datastream Date: 08/06/2021The Saudi Arabian Monetary Agency (SAMA) reaffirmed its commitment to maintaining the peg during the peak of the speculative pressure in May 2020. During a press conference it noted “SAMA remains committed to maintaining the exchange rate at the official rate of 3.75 riyals to the dollar as an anchor of monetary and financial stability”. We think the ample FX reserves should be more than sufficient for the SAMA to continue to intervene in order to maintain the existing peg for the foreseeable future.

Source: Refinitiv Datastream Date: 08/06/2021The Saudi Arabian Monetary Agency (SAMA) reaffirmed its commitment to maintaining the peg during the peak of the speculative pressure in May 2020. During a press conference it noted “SAMA remains committed to maintaining the exchange rate at the official rate of 3.75 riyals to the dollar as an anchor of monetary and financial stability”. We think the ample FX reserves should be more than sufficient for the SAMA to continue to intervene in order to maintain the existing peg for the foreseeable future. Source: Refinitiv Datastream Date: 08/06/2021Official communications from the central bank on the suitability of the peg have been scarce since the bank affirmed its commitment to protecting it in March last year, although we don’t think that such communications have been particularly necessary. The currency’s one-year forward discount rate peaked at around -0.2% at the height of the pandemic, suggesting that speculative pressure on the currency in the past year or so has been relatively modest.

Source: Refinitiv Datastream Date: 08/06/2021Official communications from the central bank on the suitability of the peg have been scarce since the bank affirmed its commitment to protecting it in March last year, although we don’t think that such communications have been particularly necessary. The currency’s one-year forward discount rate peaked at around -0.2% at the height of the pandemic, suggesting that speculative pressure on the currency in the past year or so has been relatively modest.

Source: Refinitiv Datastream Date: 08/06/2021We have outlined in this report our view as to the vulnerability of each peg to devaluation. We believe that this vulnerability depends heavily on both the ability of the country’s central bank to defend the peg and also the suitability of the exchange rate for each country’s domestic economy. The key factors that we look at in considering each currency’s vulnerability are:- Foreign exchange reserves & sovereign funds in relation to imports.

- Current account balance as a percentage of GDP.

- Public debt levels as a percentage of GDP.

| SAD | UAE | Qatar | Oman | Bahrain | Kuwait | |

| Spot Exchange Rate vs. USD | 3.75 | 3.67 | 3.69 | 0.38 | 0.38 | 0.30 |

| FX Reserves (US$ billions) | 449 | 105 | 55.6 | 17.4 | 3.2 | 44.5 |

| Sovereign Funds (US$ billions) | 900 | 1363 | 345 | 14.3 | 18.6 | 534 |

| FX reserves and sovereign funds as total months' worth of imports | 42 | 83 | 166 | 14 | 10 | 85 |

| Current Account Balance (% of GDP) [2020] | -2.8% | +5.9% | -2.5% | -5.2% | -2.1%* | +0.8% |

| Public Debt (% of GDP) | 32.5% | 36.9% | 71.8% | 55.9% | 128.3% | 11.5% |

| 1 Year Forward (28/05/21) | 3.7525 | 3.6735 | 3.7064 | 0.3860 | 0.3786 | 0.3031 |

| Forward Discount (28/05/21) | -0.06% | -0.02% | -0.21% | -0.29% | -0.45% | -0.90% |

| Forward Discount (23/04/20) | -0.68% | -0.22% | -0.18% | -5.18% | -0.15% | -1.74% |

| Likelihood of Devaluation | Very Low | Very Low | Very Low | Low | Low | Very Low |

Saudi Arabian Riyal (SAR)

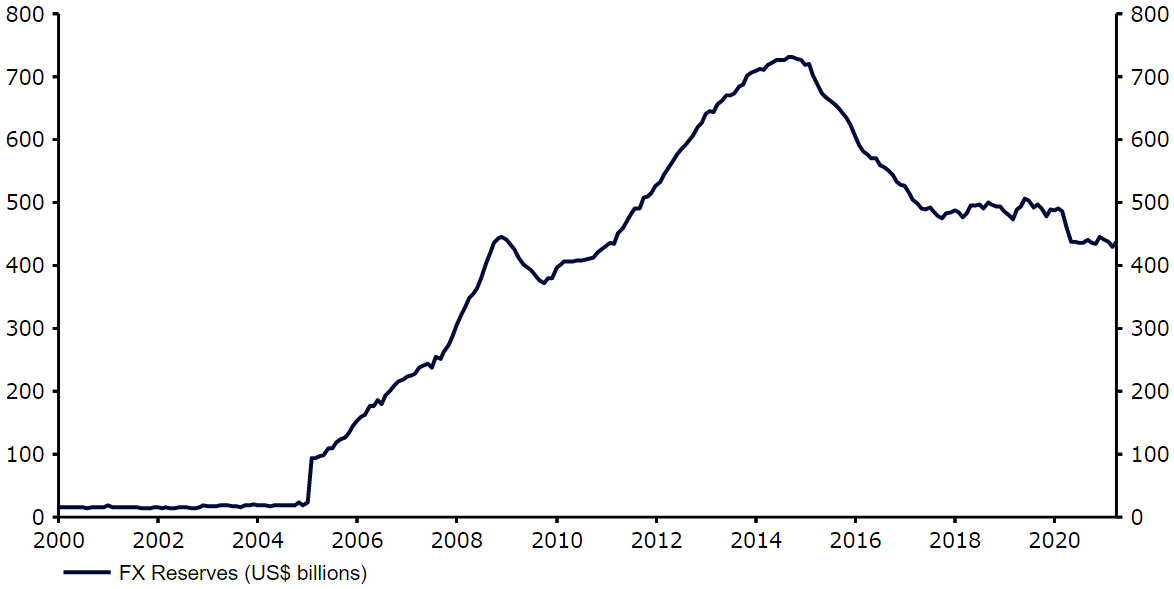

Saudia Arabia is one of the world’s largest oil producers. The sharp downturn experienced in oil prices at the beginning of the COVID-19 crisis was, therefore, particularly bad news for the heavily oil-reliant Saudi economy. Oil revenues account for around 75% of Saudi Arabia’s total export revenue and 40% of overall output. The country’s oil revenues unsurprisingly declined sharply in 2020, contributing to the record contraction in economic activity experienced in the country in Q2 of last year. Activity rebounded in the second half of the year as virus restrictions were eased and oil prices picked up. Saudi Arabia has done remarkably well in suppressing rates of virus contagion following the initial peak in June last year. The country is also so far making steady progress towards building up immunity levels through vaccinations, having now administered more than 40 doses per 100 people at the time of writing. This provides reason for optimism that we’ll see a return to near-normal economic capacity in Saudi Arabia later in the year.Despite the aforementioned rebound late-last year, real oil GDP still ended 2020 6.7% lower than where it began the year. This downturn in oil revenues plunged the economy deep into recession and has accelerated the need to diversify away from oil production. GDP fell by another 0.1% quarter-on-quarter in Q1, leading to the seventh consecutive quarter of negative annual growth (-3.3%). Oil GDP collapsed by 12% YoY in the first quarter, in large part a result of production cuts by the OPEC countries since May 2020. The rebound in global oil prices has, however, significantly lessened pressure on the USD/SAR peg, which came under unwanted speculative pressure in mid-2020 at the height of the downturn. Brent crude oil prices increased to $70 a barrel in May, just shy of its highest level since May 2019. While this remains short of Saudi Arabia’s reported breakeven oil price for this year, which is estimated to be around $76 a barrel, we think that the riyal’s peg is under little risk of being abandoned any time soon. Saudi Arabia amassed huge amounts of oil wealth during the periods of high oil prices and its FX reserves are now among the largest in the world. Saudi Arabia’s sovereign funds, a de facto FX reserves, are also massive at approximately US$900 billion. Combined, these total the equivalent of around 42 months’ worth of import cover - more than enough for continued intervention. Figure 2: Saudi Arabia Foreign Exchange Reserves (US$ billions) (2002 - 2021)Source: Refinitiv Datastream Date: 08/06/2021The Saudi Arabian Monetary Agency (SAMA) reaffirmed its commitment to maintaining the peg during the peak of the speculative pressure in May 2020. During a press conference it noted “SAMA remains committed to maintaining the exchange rate at the official rate of 3.75 riyals to the dollar as an anchor of monetary and financial stability”. We think the ample FX reserves should be more than sufficient for the SAMA to continue to intervene in order to maintain the existing peg for the foreseeable future.United Arab Emirates Dirham (AED)

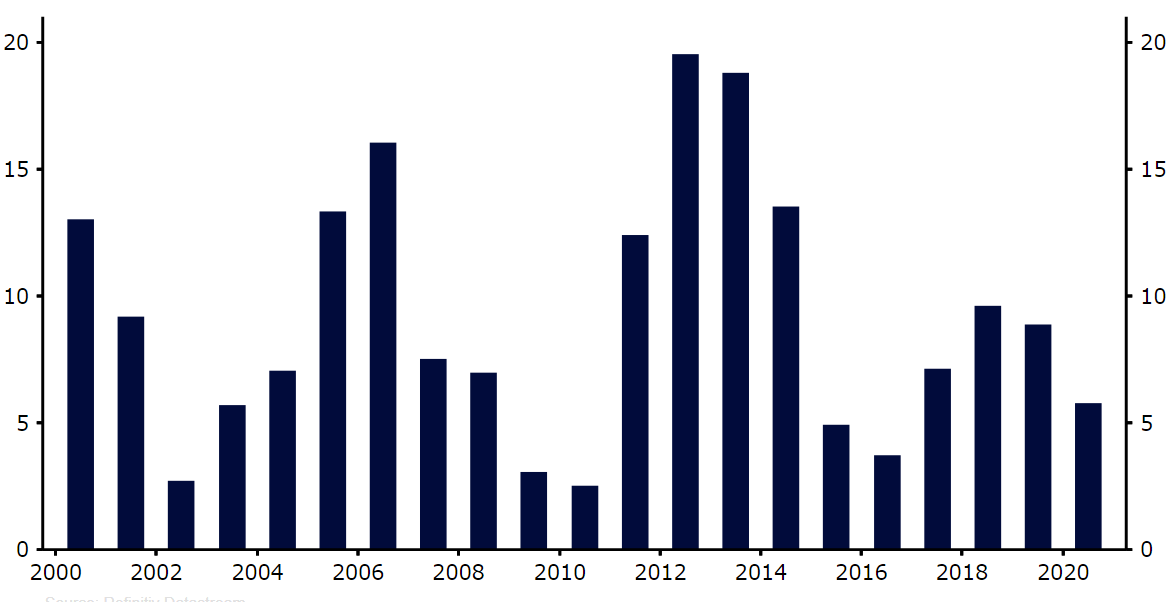

The UAE dirham is not vulnerable to a devaluation, in our view, and is indeed one of the best equipped in the GCC to maintain its peg.Similarly to many of its regional peers, the UAE is also fairly reliant on oil production as a share of overall output. The UAE’s GDP collapsed by 5.8% in 2020, a product of both the downturn in oil revenues and a loss of tourism receipts. The country’s central bank expects growth to return in 2021, with activity set to expand by 2.5% this year and 3.5% in 2022.We have been particularly encouraged by the country’s vaccination efforts so far, which has seen the country administer approximately 135 vaccine doses per 100 people at the time of writing - among the highest in the world. This, in our view, should allow a swift return to near-normal economic capacity in the second half of the year. The Dubai Expo world fair and Fifa World Cup in neighbouring Qatar should further help support economic growth over the central bank’s forecast horizon. The UAE is also one of the most diversified economies in the GCC, so the collapse in oil prices at the start of the COVID-19 pandemic was not quite as damaging to the domestic economy as witnessed elsewhere in the region.We think that the Central Bank of the UAE should have little issue maintaining the existing USD peg. Hard currency foreign exchange reserves are relatively low at around $105 billion, but the UAE stores wealth in other areas including sovereign wealth funds of more than $1360 billion (a combined 83 months’ worth of import cover). This is second only to China’s as the largest sovereign wealth fund in the world and should provide plenty of room for the central bank to continue intervening in the currency market for a long while yet.An increase in government debt as a share of GDP to 36.9% in 2020 is not ideal, but the country’s current account remains firmly in positive territory at 5.9% of GDP last year. The latter should help warn off any speculative attacks against the currency during future periods of market uncertainty. We also don’t expect this surplus to be eroded any time soon. Global oil prices would need to average around $30 a barrel over a one-year period for this to be the case, which appears highly unlikely for the foreseeable future.Figure 3: UAE Current Account Balance [% of GDP] (2002 - 2021)Source: Refinitiv Datastream Date: 08/06/2021Official communications from the central bank on the suitability of the peg have been scarce since the bank affirmed its commitment to protecting it in March last year, although we don’t think that such communications have been particularly necessary. The currency’s one-year forward discount rate peaked at around -0.2% at the height of the pandemic, suggesting that speculative pressure on the currency in the past year or so has been relatively modest.