G3 FX Forecast Revision 2021

Vaccination progress has been one of the most important determinants of exchange rates so far in 2021. We do, however, think that with the reopening of economies, vaccination numbers will be less relevant in the eyes of investors. Attention now turns to the performance of the G3 economies and the response of central banks to both the rebound in economic activity and the sharp increase in global inflationary pressures.

FX Market Updates

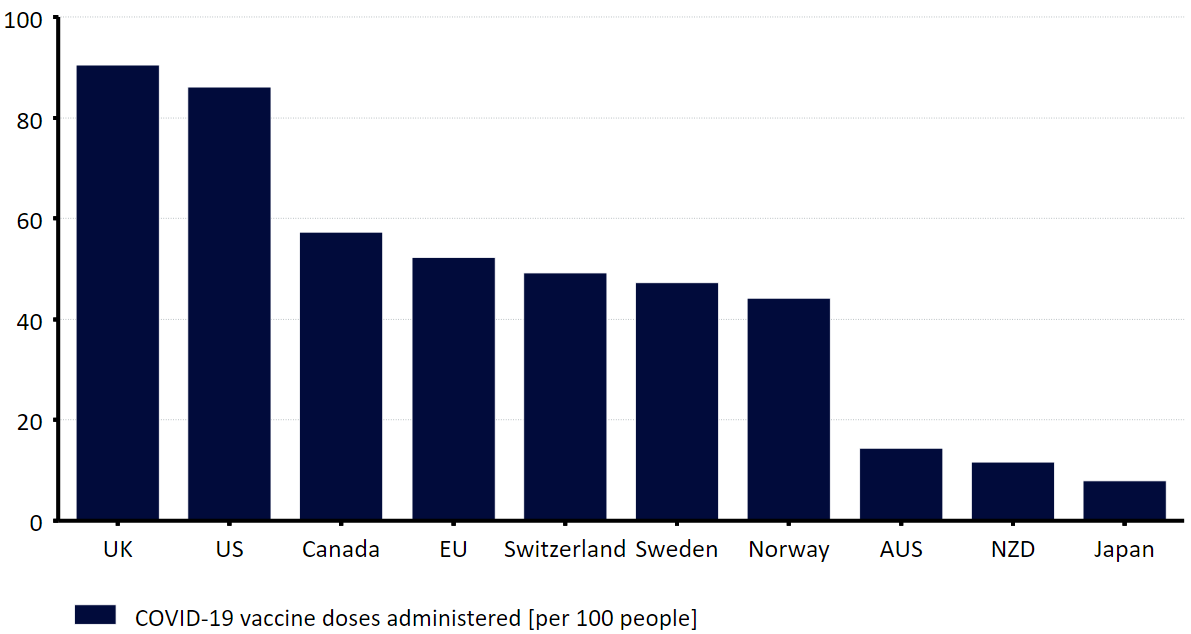

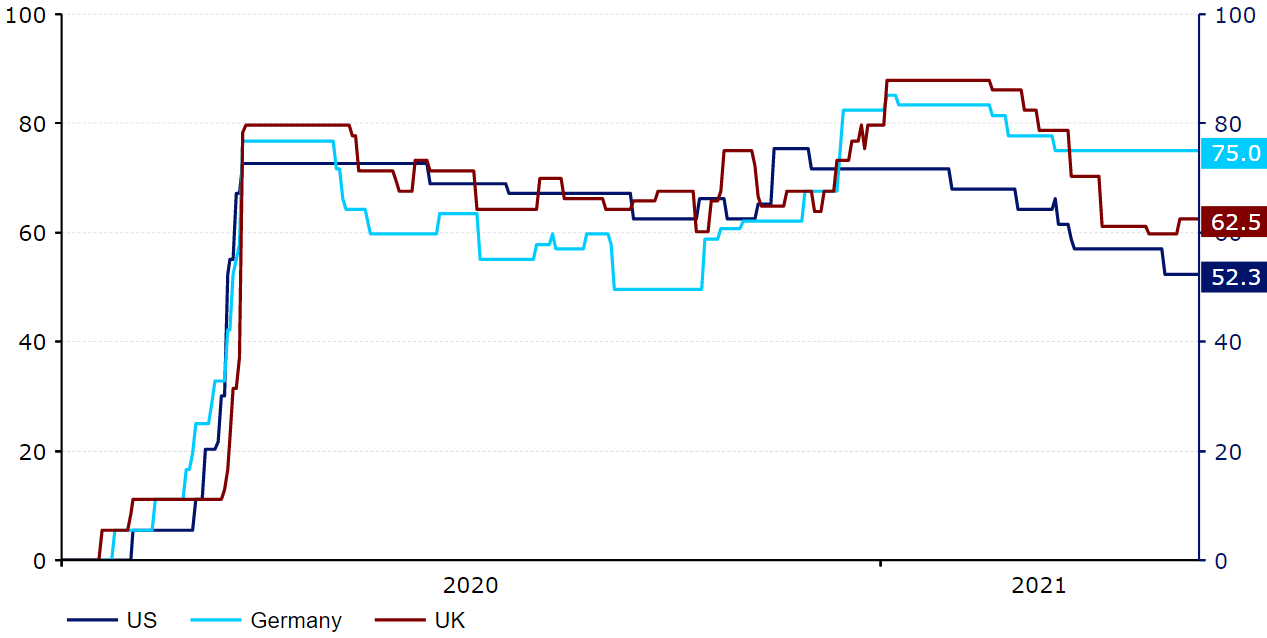

News on the COVID-19 pandemic has been largely positive so far in 2021, creating a bullish environment for risk currencies and a negative one for safe-havens.Most of the major economic areas have now rolled out the various vaccines to most or all of their most vulnerable demographics. The US and UK have now administered more than 85 vaccine doses per 100 people, with 49% and 56% of their populations respectively having received at least one dose at the time of writing. The European Union has lagged behind with vaccinations since the beginning of the bloc’s inoculation programme (50 doses per 100), although it has managed to close the gap in the pace of daily vaccination in recent weeks. This explains much of the rally in EUR/USD since the start of April that has seen it trade back above the 1.22 level for the first time since late-February.Figure 1: G10 COVID-19 Vaccines Doses Administered (per 100 people)  Source: Refinitiv Datastream Date: 26/05/2021A combination of the immunity levels built up through vaccinations and a sharp decline in rates of virus contagion has allowed a fairly material unwinding of containment measures in the UK and, to an even greater extent, the US. This is evident in the COVID-19 Government Response Stringency index, which is currently around the lowest that it has been in both countries since March 2020 (Figure 2). The US economy has, in particular, managed to power ahead of most of its major peers in the past few months, expanding at a very healthy clip again in the first quarter of the year. This has raised a few concerns among market participants that the US economy may be at risk of overheating, particularly given the extraordinarily accommodative policy stances adopted by both the Federal Reserve and the US government. Figure 2: G3 COVID-19 Government Response Stringency Index (March ‘20 - May ‘21)

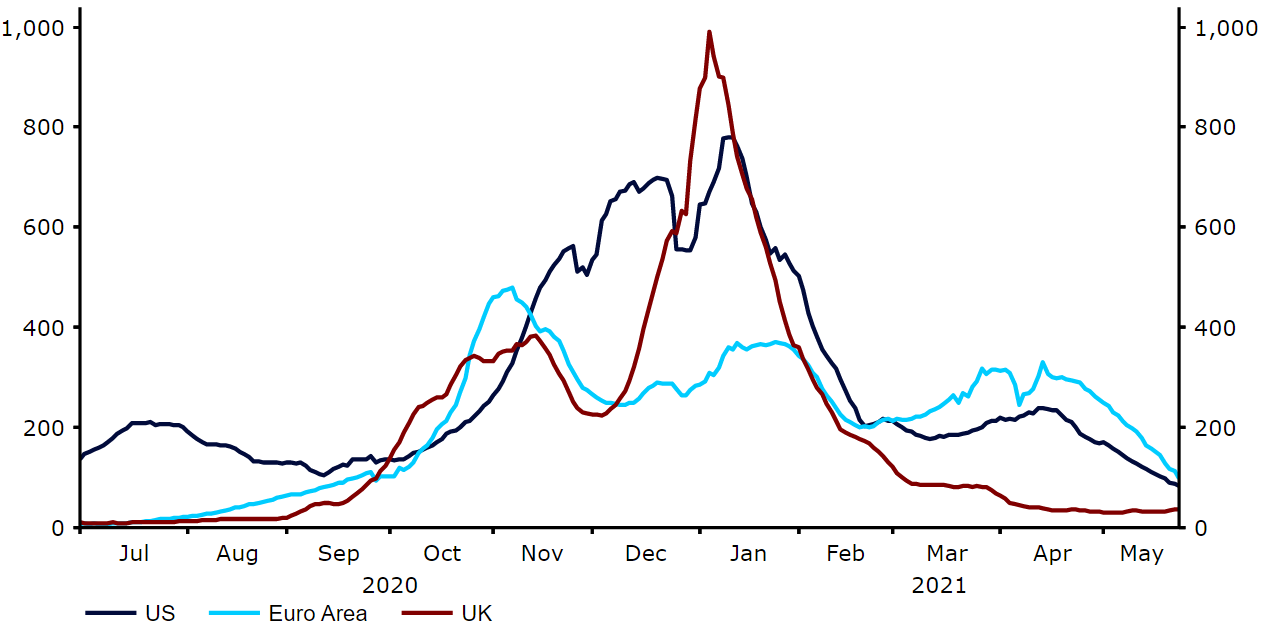

Source: Refinitiv Datastream Date: 26/05/2021A combination of the immunity levels built up through vaccinations and a sharp decline in rates of virus contagion has allowed a fairly material unwinding of containment measures in the UK and, to an even greater extent, the US. This is evident in the COVID-19 Government Response Stringency index, which is currently around the lowest that it has been in both countries since March 2020 (Figure 2). The US economy has, in particular, managed to power ahead of most of its major peers in the past few months, expanding at a very healthy clip again in the first quarter of the year. This has raised a few concerns among market participants that the US economy may be at risk of overheating, particularly given the extraordinarily accommodative policy stances adopted by both the Federal Reserve and the US government. Figure 2: G3 COVID-19 Government Response Stringency Index (March ‘20 - May ‘21) Source: Refinitiv Datastream Date: 26/05/2021By contrast, the Euro Area economy contracted again in Q1, entering into a ‘double-dip’ recession for the first time since 2012. Virus restrictions remain rather strict in much of Europe following the third wave of virus infection that swept throughout the continent in March and April. New daily virus cases have eased in the bloc in the past few weeks, although the slower vaccine rollout has delayed reopening. That being said, we are optimistic that we’ll see a strong recovery in the second and third quarters that will close the gap in economic performance between the US and Euro Area. Figure 3: G3 New COVID-19 Cases [per 1M people] (March ‘20 - May ‘21)

Source: Refinitiv Datastream Date: 26/05/2021By contrast, the Euro Area economy contracted again in Q1, entering into a ‘double-dip’ recession for the first time since 2012. Virus restrictions remain rather strict in much of Europe following the third wave of virus infection that swept throughout the continent in March and April. New daily virus cases have eased in the bloc in the past few weeks, although the slower vaccine rollout has delayed reopening. That being said, we are optimistic that we’ll see a strong recovery in the second and third quarters that will close the gap in economic performance between the US and Euro Area. Figure 3: G3 New COVID-19 Cases [per 1M people] (March ‘20 - May ‘21) Source: Refinitiv Datastream Date: 26/05/2021Vaccination progress has been one of the most important determinants of exchange rates so far in 2021. We do, however, think that we are now at a stage where the reopening of economies has made vaccination numbers much less relevant in the eyes of investors. Market participants have instead shifted their focus back towards the relative performance of the G3 economies and the response of central banks to both the rebound in economic activity and sharp increase in global inflationary pressures.

Source: Refinitiv Datastream Date: 26/05/2021Vaccination progress has been one of the most important determinants of exchange rates so far in 2021. We do, however, think that we are now at a stage where the reopening of economies has made vaccination numbers much less relevant in the eyes of investors. Market participants have instead shifted their focus back towards the relative performance of the G3 economies and the response of central banks to both the rebound in economic activity and sharp increase in global inflationary pressures.

Source: Refinitiv Datastream Date: 26/05/2021A combination of the immunity levels built up through vaccinations and a sharp decline in rates of virus contagion has allowed a fairly material unwinding of containment measures in the UK and, to an even greater extent, the US. This is evident in the COVID-19 Government Response Stringency index, which is currently around the lowest that it has been in both countries since March 2020 (Figure 2). The US economy has, in particular, managed to power ahead of most of its major peers in the past few months, expanding at a very healthy clip again in the first quarter of the year. This has raised a few concerns among market participants that the US economy may be at risk of overheating, particularly given the extraordinarily accommodative policy stances adopted by both the Federal Reserve and the US government. Figure 2: G3 COVID-19 Government Response Stringency Index (March ‘20 - May ‘21)Source: Refinitiv Datastream Date: 26/05/2021By contrast, the Euro Area economy contracted again in Q1, entering into a ‘double-dip’ recession for the first time since 2012. Virus restrictions remain rather strict in much of Europe following the third wave of virus infection that swept throughout the continent in March and April. New daily virus cases have eased in the bloc in the past few weeks, although the slower vaccine rollout has delayed reopening. That being said, we are optimistic that we’ll see a strong recovery in the second and third quarters that will close the gap in economic performance between the US and Euro Area. Figure 3: G3 New COVID-19 Cases [per 1M people] (March ‘20 - May ‘21)Source: Refinitiv Datastream Date: 26/05/2021Vaccination progress has been one of the most important determinants of exchange rates so far in 2021. We do, however, think that we are now at a stage where the reopening of economies has made vaccination numbers much less relevant in the eyes of investors. Market participants have instead shifted their focus back towards the relative performance of the G3 economies and the response of central banks to both the rebound in economic activity and sharp increase in global inflationary pressures.