G3 Forecast Revision - January 2021

One of the main talking points among the countries of the G3 currencies has been the divergence in new virus caseloads that we’ve witnessed between the US and Europe. Read on to find out what to expect from US dollar, Euro and Sterling this year.

FX Market Updates

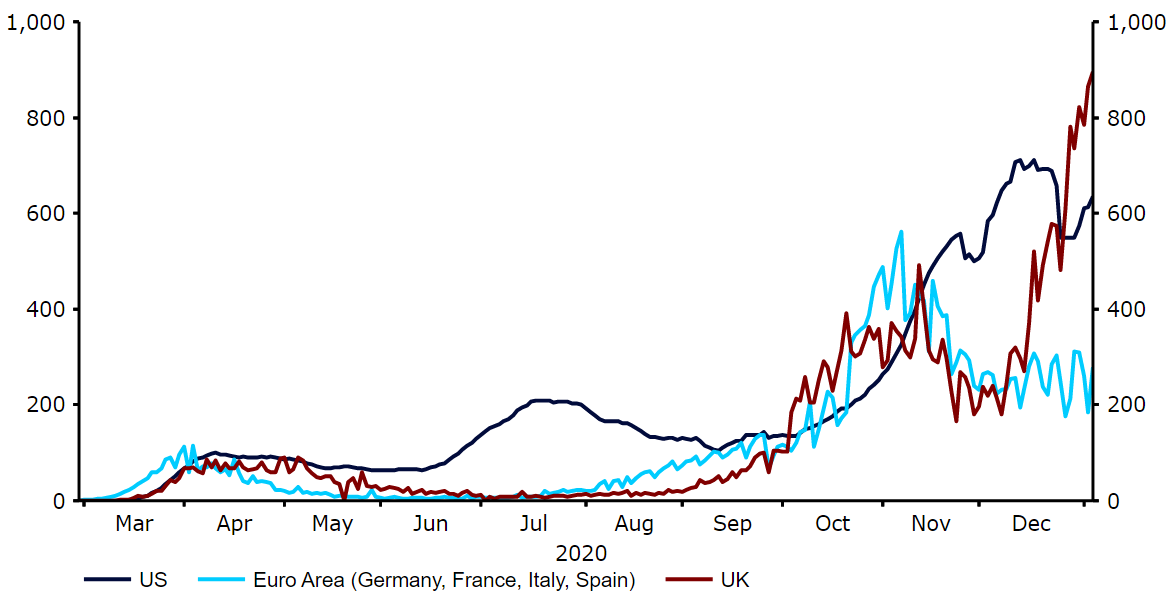

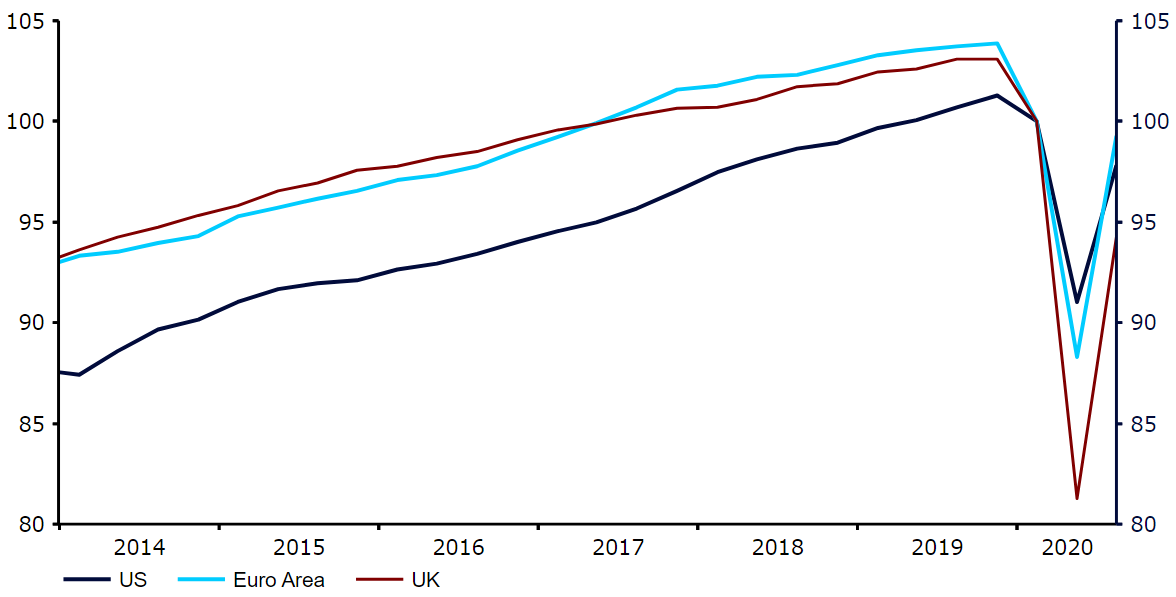

News headlines out of the foreign exchange market have continued to be dominated by the latest developments surrounding the COVID-19 pandemic in the past few weeks.One of the main talking points among the countries of the G3 currencies has been the divergence in new virus caseloads that we’ve witnessed between the US and Europe. Following a sharp jump in new virus cases in October, authorities across the European continent were quick to reimpose strict containment measures in order to halt its spread, including the reintroduction of lockdowns. By contrast, the US has adopted a more haphazard, state-by-state approach, whereby some areas have been placed under tough restrictions and others have not. As a result, case numbers and deaths caused by the virus in the US have surged to record highs, while the same measures in most of Europe have either stabilised or fallen to multi-week lows (Figure 1). An exception to this is the UK, where the more aggressive spreading strain of the virus has caused caseloads to spiral sharply higher since the beginning of December, leading to the reimposition of further strict lockdowns in Britain in early-January.Figure 1: G3 New COVID-19 Cases [per 1M people] (March ‘20 - Jan ‘21) Source: Refinitiv Datastream Date: 06/01/2021The tough virus restrictions put in place during the fourth quarter have also once again weighed on economic activity. Most major economic areas around the world bounced back strongly in Q3, posting record expansions as containment measures were gradually unwound. It does, however, look likely that both the Euro Area and the UK economy suffered from contractions once again in Q4, with overall activity still well below pre-pandemic levels (Figure 2).Figure 2: GDP (US, Euro Area & UK) [Q1 2020=100] (2014 - 2020)

Source: Refinitiv Datastream Date: 06/01/2021The tough virus restrictions put in place during the fourth quarter have also once again weighed on economic activity. Most major economic areas around the world bounced back strongly in Q3, posting record expansions as containment measures were gradually unwound. It does, however, look likely that both the Euro Area and the UK economy suffered from contractions once again in Q4, with overall activity still well below pre-pandemic levels (Figure 2).Figure 2: GDP (US, Euro Area & UK) [Q1 2020=100] (2014 - 2020) Source: Refinitiv Datastream Date: 06/01/2021That being said, encouraging news of progress towards multiple COVID-19 vaccines has buoyed financial markets and raised hopes that a return to normalcy could take place sooner than had previously been anticipated. The UK was the first country in the world to begin mass vaccinations using the Pfizer/BioNTech vaccine on 8th December, with vaccinations using the AstraZeneca jab commencing in early-January. The US also began its vaccination programme in December, with the EU not too far behind. Risk assets have rallied sharply on the news with the safe-havens, including the US dollar, falling markedly. We think that news of progress towards the mass rolling out of vaccines among the developed nations will be one of the main drivers for the G3 currencies in 2021.

Source: Refinitiv Datastream Date: 06/01/2021That being said, encouraging news of progress towards multiple COVID-19 vaccines has buoyed financial markets and raised hopes that a return to normalcy could take place sooner than had previously been anticipated. The UK was the first country in the world to begin mass vaccinations using the Pfizer/BioNTech vaccine on 8th December, with vaccinations using the AstraZeneca jab commencing in early-January. The US also began its vaccination programme in December, with the EU not too far behind. Risk assets have rallied sharply on the news with the safe-havens, including the US dollar, falling markedly. We think that news of progress towards the mass rolling out of vaccines among the developed nations will be one of the main drivers for the G3 currencies in 2021.  Source: Refinitiv Datastream Date: 05/01/2021November’s presidential election was perhaps the biggest event risk in financial markets in the past few months, outside the COVID pandemic. Investors had a case of deja vu on the night of the election, as early results suggested that Trump had once again outperformed the opinion polls. With the vast majority of mail-in votes cast by Democrats it did, however, become increasingly clear that Biden was heading for victory fairly early on, even though the final outcome in a handful of states was not known until a few days after election night. Investors ditched the safe-haven dollar and favoured risky assets long before the final result was officially adjudicated. A Biden presidency has been perceived as a positive for risk assets and negative for the safe-haven US dollar, given the likelihood of a larger fiscal stimulus programme and decreased trade uncertainty under a Democratic administration. An issue for Biden at the time was that the Democrats were unable to win control of the Senate and achieve a so-called ‘blue wave’. Two run-off Senate elections in Georgia on 5th January took on an unusual amount of significance and were closely watched by financial markets. The Democrats required a double-win in order to obtain full control of Congress, thus granting Biden a much better chance of passing legislative changes once he takes office later this month. In the end, the Democrats surprised our and indeed the markets’ expectations in winning both votes. So far, currencies have reacted as we anticipated that they would in such a scenario, with the dollar selling off across the board. We think that the dollar could come under a bit of additional selling pressure in the short-term, as investors continue to price in larger fiscal support from the Biden administration.One of the most contentious issues leading up to the election was President Trump’s handling of the ongoing pandemic. Since our last G3 update, the virus situation has worsened in the US, as it has done throughout much of the developed world. New daily cases have jumped to record highs (Figure 4), as have deaths caused by the virus. According to Worldometer, the US now has one of the top fifteen worst COVID death rates in the world (more than 1,100 per 1 million people) and a cases per capita ratio that far outstrips most other developed nations (approximately 65,000 per 1M). Figure 4: New Daily COVID-19 Cases [US] [per 1M people] (March ‘20 - Jan ‘21)

Source: Refinitiv Datastream Date: 05/01/2021November’s presidential election was perhaps the biggest event risk in financial markets in the past few months, outside the COVID pandemic. Investors had a case of deja vu on the night of the election, as early results suggested that Trump had once again outperformed the opinion polls. With the vast majority of mail-in votes cast by Democrats it did, however, become increasingly clear that Biden was heading for victory fairly early on, even though the final outcome in a handful of states was not known until a few days after election night. Investors ditched the safe-haven dollar and favoured risky assets long before the final result was officially adjudicated. A Biden presidency has been perceived as a positive for risk assets and negative for the safe-haven US dollar, given the likelihood of a larger fiscal stimulus programme and decreased trade uncertainty under a Democratic administration. An issue for Biden at the time was that the Democrats were unable to win control of the Senate and achieve a so-called ‘blue wave’. Two run-off Senate elections in Georgia on 5th January took on an unusual amount of significance and were closely watched by financial markets. The Democrats required a double-win in order to obtain full control of Congress, thus granting Biden a much better chance of passing legislative changes once he takes office later this month. In the end, the Democrats surprised our and indeed the markets’ expectations in winning both votes. So far, currencies have reacted as we anticipated that they would in such a scenario, with the dollar selling off across the board. We think that the dollar could come under a bit of additional selling pressure in the short-term, as investors continue to price in larger fiscal support from the Biden administration.One of the most contentious issues leading up to the election was President Trump’s handling of the ongoing pandemic. Since our last G3 update, the virus situation has worsened in the US, as it has done throughout much of the developed world. New daily cases have jumped to record highs (Figure 4), as have deaths caused by the virus. According to Worldometer, the US now has one of the top fifteen worst COVID death rates in the world (more than 1,100 per 1 million people) and a cases per capita ratio that far outstrips most other developed nations (approximately 65,000 per 1M). Figure 4: New Daily COVID-19 Cases [US] [per 1M people] (March ‘20 - Jan ‘21)

Source: Refinitiv Datastream Date: 06/01/2021The tough virus restrictions put in place during the fourth quarter have also once again weighed on economic activity. Most major economic areas around the world bounced back strongly in Q3, posting record expansions as containment measures were gradually unwound. It does, however, look likely that both the Euro Area and the UK economy suffered from contractions once again in Q4, with overall activity still well below pre-pandemic levels (Figure 2).Figure 2: GDP (US, Euro Area & UK) [Q1 2020=100] (2014 - 2020)Source: Refinitiv Datastream Date: 06/01/2021That being said, encouraging news of progress towards multiple COVID-19 vaccines has buoyed financial markets and raised hopes that a return to normalcy could take place sooner than had previously been anticipated. The UK was the first country in the world to begin mass vaccinations using the Pfizer/BioNTech vaccine on 8th December, with vaccinations using the AstraZeneca jab commencing in early-January. The US also began its vaccination programme in December, with the EU not too far behind. Risk assets have rallied sharply on the news with the safe-havens, including the US dollar, falling markedly. We think that news of progress towards the mass rolling out of vaccines among the developed nations will be one of the main drivers for the G3 currencies in 2021. US Dollar (USD)

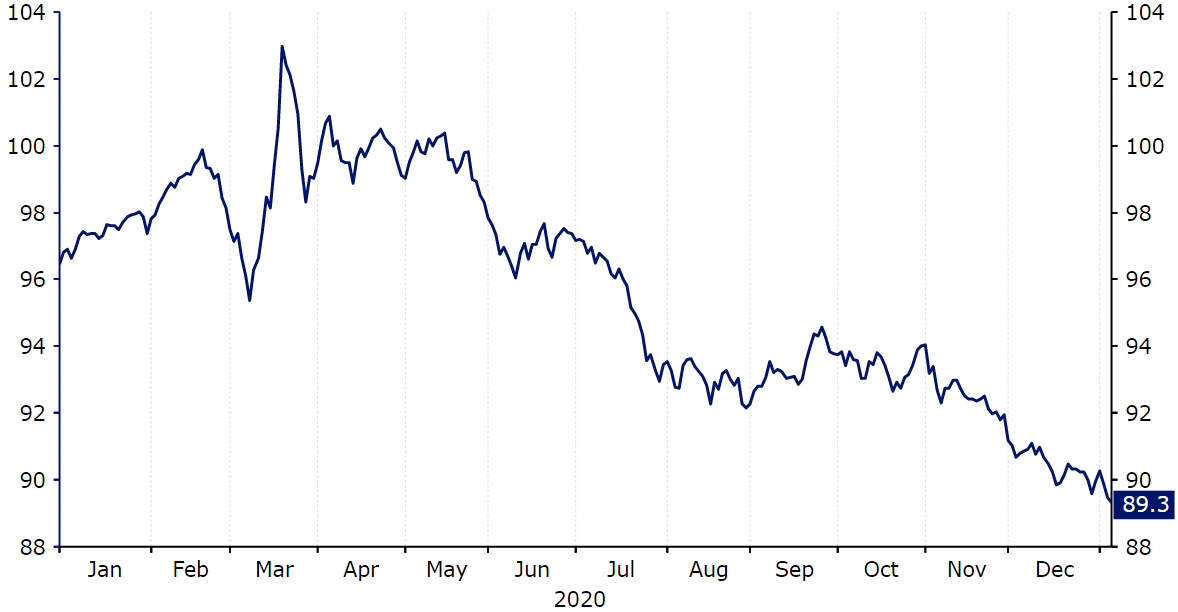

The US dollar was on the back foot against most of its major peers throughout much of the final quarter of 2020.Investors had flocked to the dollar during the worst of the market panic earlier in the year. The currency jumped to its strongest position against its major peers in over three years at the end of March, although these safe-haven bets were reversed in the second and third quarters. Since the beginning of the fourth quarter, the dollar has been back under selling pressure again as markets cheered both the outcome of the US presidential election and news of progress towards multiple COVID-19 vaccines. The US dollar index is currently trading around its lowest level since April 2018 (Figure 3).Figure 3: US Dollar Index (January ‘20 - January ‘21)Source: Refinitiv Datastream Date: 05/01/2021November’s presidential election was perhaps the biggest event risk in financial markets in the past few months, outside the COVID pandemic. Investors had a case of deja vu on the night of the election, as early results suggested that Trump had once again outperformed the opinion polls. With the vast majority of mail-in votes cast by Democrats it did, however, become increasingly clear that Biden was heading for victory fairly early on, even though the final outcome in a handful of states was not known until a few days after election night. Investors ditched the safe-haven dollar and favoured risky assets long before the final result was officially adjudicated. A Biden presidency has been perceived as a positive for risk assets and negative for the safe-haven US dollar, given the likelihood of a larger fiscal stimulus programme and decreased trade uncertainty under a Democratic administration. An issue for Biden at the time was that the Democrats were unable to win control of the Senate and achieve a so-called ‘blue wave’. Two run-off Senate elections in Georgia on 5th January took on an unusual amount of significance and were closely watched by financial markets. The Democrats required a double-win in order to obtain full control of Congress, thus granting Biden a much better chance of passing legislative changes once he takes office later this month. In the end, the Democrats surprised our and indeed the markets’ expectations in winning both votes. So far, currencies have reacted as we anticipated that they would in such a scenario, with the dollar selling off across the board. We think that the dollar could come under a bit of additional selling pressure in the short-term, as investors continue to price in larger fiscal support from the Biden administration.One of the most contentious issues leading up to the election was President Trump’s handling of the ongoing pandemic. Since our last G3 update, the virus situation has worsened in the US, as it has done throughout much of the developed world. New daily cases have jumped to record highs (Figure 4), as have deaths caused by the virus. According to Worldometer, the US now has one of the top fifteen worst COVID death rates in the world (more than 1,100 per 1 million people) and a cases per capita ratio that far outstrips most other developed nations (approximately 65,000 per 1M). Figure 4: New Daily COVID-19 Cases [US] [per 1M people] (March ‘20 - Jan ‘21)