The euro finished the week at the bottom of the G10 rankings on concerns that the war in Ukraine will not stop any time soon, as well as jitters about the French presidential election.

The carnage in the US bond market continues, with 10-year Treasury yields up an astounding 30 basis points on the week, and the dollar reacted in an expected way by topping every major currency in the world, save a handful of volatile EM ones. Ruble volatility continues and the currency is now higher than before Russia launched its invasion, but it is extremely illiquid and market quotations increasingly meaningless. The Chinese yuan is proving a rock of stability amid currency market uncertainty, with the currency edging higher on a trade-weighted basis in spite of the Chinese economic slowdown and Draconian COVID lockdowns.

This week's ECB meeting is shaping up to be a critical one. The conflict between hawks and doves we had predicted for some time has erupted, as the minutes from the previous meeting make clear, and we expect communications from the central bank on Thursday to reflect that, after some really ugly inflation readings. March inflation data will also be released out of the US (Tuesday) and the UK (Wednesday). It will be an unusually busy week for the pound, as we will also get the February employment report on Tuesday.

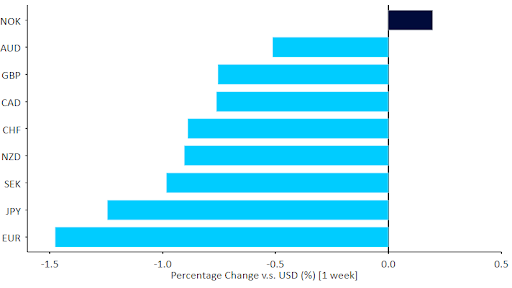

Figure 1: G10 FX Performance Tracker [base: USD] (1 week)

GBP

Sterling has had a rough time of it over the past few weeks after dovish rhetoric from the Bank of England. The pound has briefly traded below the 1.30 level versus the US dollar in the past couple of trading sessions as a result, and continues to hover around its weakest position since November 2020 at the time of writing. The very strong March PMIs and what we expect to be equally strong labour market and inflation data should, however, put a floor under the currency as we wait for the MPC members to acknowledge the reality of a fresh inflationary wave hitting an economy already at full capacity. We expect cable to find a floor around current levels as the Bank of England stance becomes increasingly untenable.

Figure 2: GBP/USD (YTD)

EUR

The first round of the French presidential elections was a mild euro positive, as Macron appears to go into the second round against Le Pen in a slightly stronger position than expected. More euro positive news were a chorus of hawkish remarks from ECB members, as well as some scathing remarks in the March meeting minutes about its staff's almost incredibly optimistic inflation forecasts. which expect a return to just on target inflation by 2023.

Neither of these seems to have had much of an impact on the market, and all eyes now turn to this week's ECB meeting. We think that even a slight change in tone from the heretofore dovish Lagarde could have a disproportionately positive effect on the common currency.

USD

The minutes from the Federal Reserve meeting revealed a more aggressive than expected plan to wind down the Fed's gigantic holdings of Treasury and mortgage bonds. Markets continued to ratchet up expectations of Fed hikes, and now expect rates to be above 3% at some point in the first half of 2023.

It will be difficult to price in even more hawkishness from the Fed without the ECB at least closing the gap somewhat, which makes us think that the euro may be due for a rebound soon, particularly if, as we expect, Macron wins the second round of the French presidential election two weeks hence.

CHF

The Swiss franc ended the week around the middle of the G10 dashboard, edging higher against the broadly weaker euro. SNB sight deposits rose again, increasing by 2.2 bn CHF last week, less than in the previous one but still quite a notice increase. This could indicate that the bank is trying to stem the franc’s strength by deploying FX interventions. The currency’s performance is quite impressive, particularly in comparison to another safe haven peer, the Japanese yen.

The Swiss economic calendar is largely empty this week, hence we’ll focus on outside news, particularly from Ukraine, China, and France. In addition to shifts in sentiment, Thursday’s ECB meeting also has the potential to affect the EUR/CHF rate.

AUD

The Australian dollar rallied to its strongest position in ten months at the start of last week, although it has since lost its gains and ended the week lower against the US dollar. AUD jumped after the Reserve Bank of Australia abandoned its language of patience and signalled it could begin raising interest rates within months if wages and inflation data produce strong results. The central bank kept the cash rate unchanged at a record low of 0.1%, as widely expected. Even so, markets continue to price in a non-negligible chance of a first rate hike in May in order to rein in inflation.

Thursday will see the release of the March labour market report, which is expected to show further improvements. Throughout the week, the Australian dollar will likely continue being driven by shifts in commodity prices.

CAD

The Canadian dollar ended last week lower against the US dollar, pressured down by a stronger US dollar and a decline in oil prices. Canada’s jobless rate fell lower to a fresh record low of 5.3% in March from 5.5% in February. It was the lowest rate on record, marking a robust recovery for the labour market from the Covid-19 pandemic.

Figure 3: Canada Unemployment Rate (2012 - 2022)