Europe FX Forecast Revision - April 2021

While the sell-off in Eastern European currencies was not quite as dramatic as other regions in 2020, the moves lower witnessed in the region was of a magnitude unseen in years. Read our latest FX Forecast Report of the European Market. Focus on: CZK, HUF, PLN and RON.

FX Market Updates

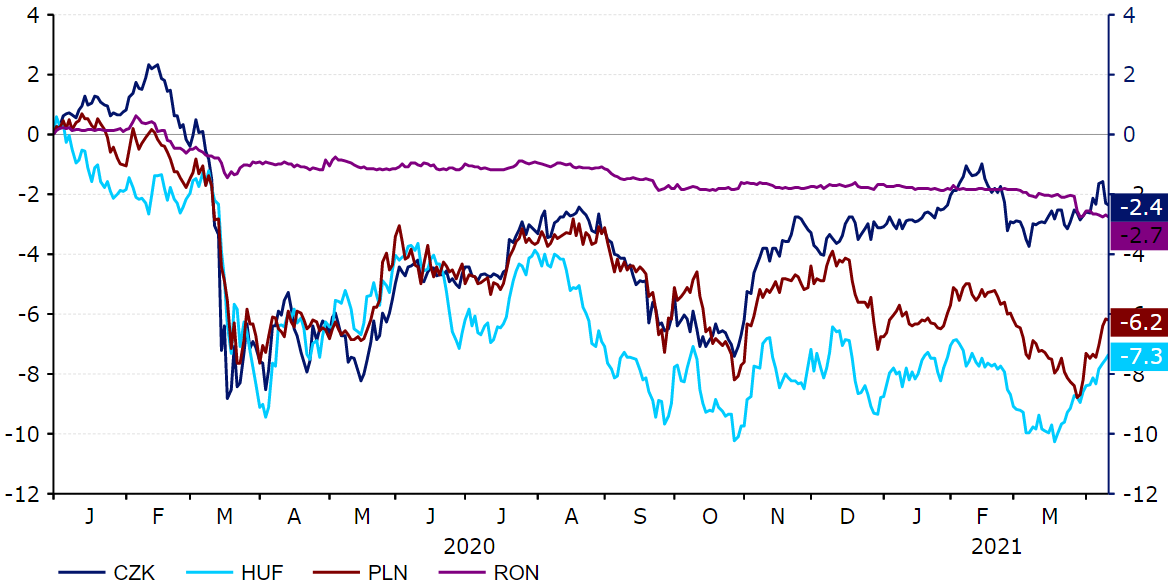

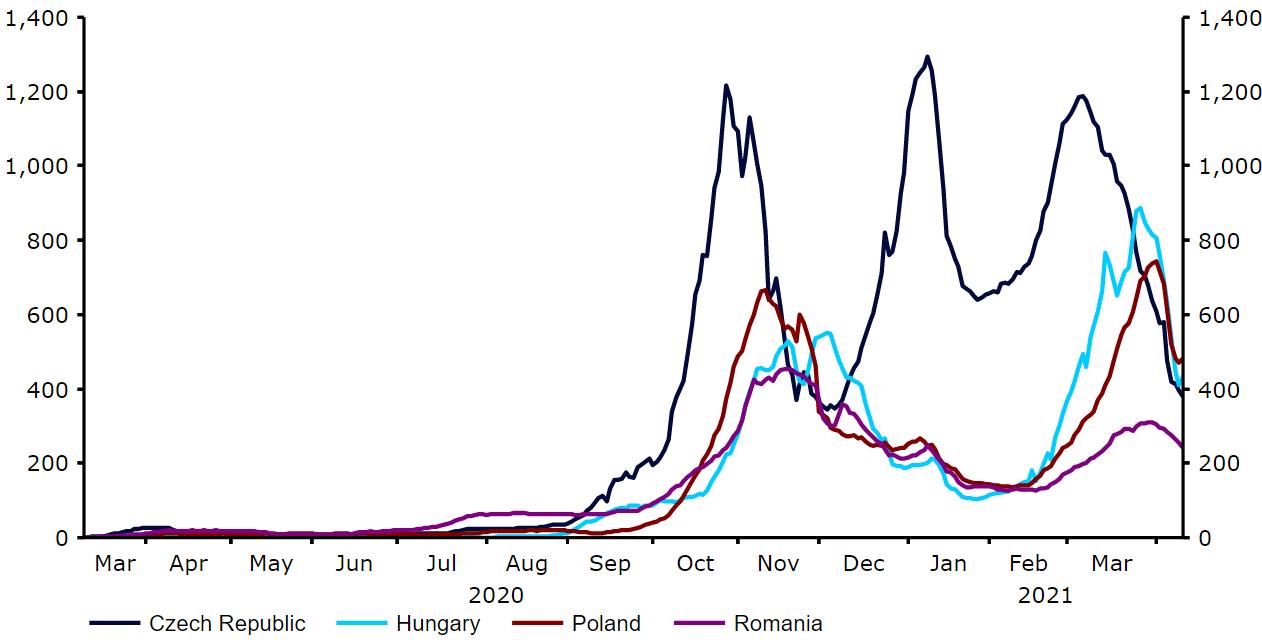

While the sell-off in Eastern European currencies was not quite as dramatic as other regions in 2020, the moves lower witnessed in the region was of a magnitude unseen in years. The CEE currencies have not fully recovered yet, with most of them suffering additional losses in the first quarter of 2021. A third wave of virus infection in Europe and rising US bond yields have pressured EM currencies lower, while supporting the US dollar. We do, however, believe that the path of least resistance for most of the CEE currencies is higher - indeed they already appear to have begun on this appreciation trend so far in the second quarter of the year. Figure 1: CZK, HUF, PLN & RON [% change vs. euro] (April ‘20 - April ‘21) Source: Refinitiv Datastream Date: 13/04/2021Since our latest European forecast revision in December, most of the currencies in the region have seen gains reversed, with both internal and external factors turning unfavourable. The pandemic situation has worsened in the region since late-February, partly a result of the emergence of faster-spreading strains of the virus. The most rapid increase in new cases took place in the Czech Republic, where the 7-day moving average of new cases reached a peak in early-March, just below the previous one set in early-January. In other countries covered in this report, this peak in caseloads has taken longer, although the worst of the third wave of infection in the region as a whole tentatively appears to be behind us. Figure 2: New COVID-19 Cases [CEE] (March ‘20 - April ‘21)

Source: Refinitiv Datastream Date: 13/04/2021Since our latest European forecast revision in December, most of the currencies in the region have seen gains reversed, with both internal and external factors turning unfavourable. The pandemic situation has worsened in the region since late-February, partly a result of the emergence of faster-spreading strains of the virus. The most rapid increase in new cases took place in the Czech Republic, where the 7-day moving average of new cases reached a peak in early-March, just below the previous one set in early-January. In other countries covered in this report, this peak in caseloads has taken longer, although the worst of the third wave of infection in the region as a whole tentatively appears to be behind us. Figure 2: New COVID-19 Cases [CEE] (March ‘20 - April ‘21) Source: Refinitiv Datastream Date: 13/04/2021Of the four countries, Romania has so far experienced the lowest rate of infection per capita (around 51,000 per 1 million people) - partly a product of relatively limited testing. The Czech Republic has fared the worst (more than 145,000 per 1M) (Figure 2), although we note that the 7-day average of Poland’s test positive rate, which represents the number of confirmed virus cases per 100 tests, is now at around 30%. This continues to outstrip the other three nations throughout the third wave of the virus. That being said, Poland’s COVID-19 death rate per 1 million people remains the second-lowest (1,473) after Romania (1,283), with the Czech Republic having the highest (2,548)*.Figure 3: COVID-19 Confirmed Cases and Deaths [per 1M people] [CEE] (as of 13/04)

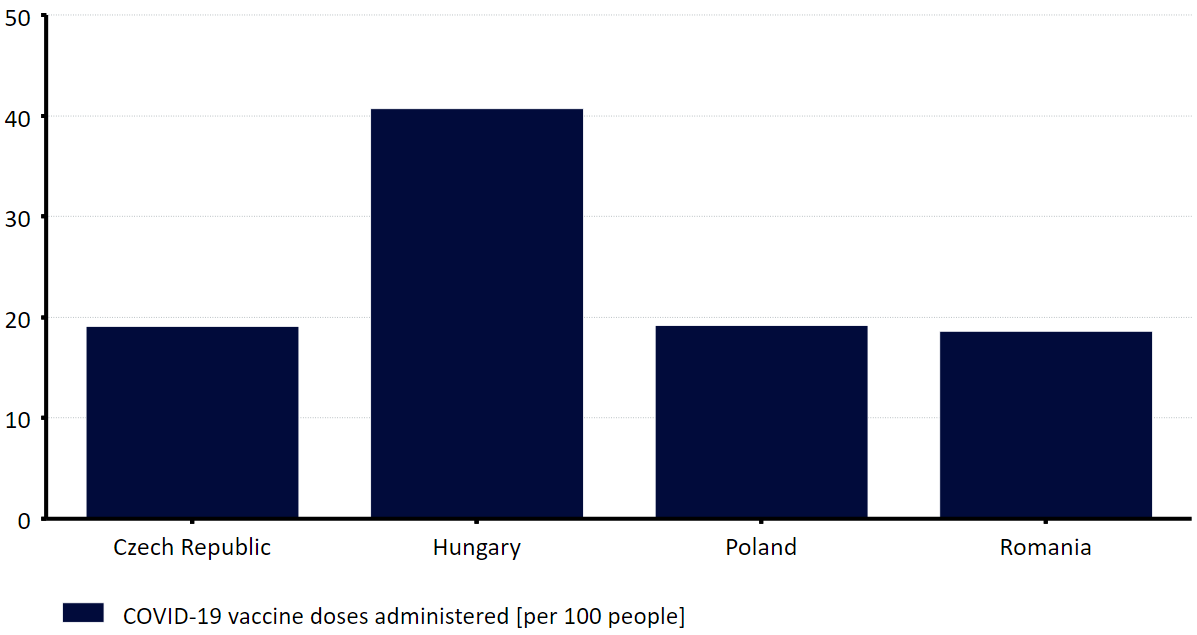

Source: Refinitiv Datastream Date: 13/04/2021Of the four countries, Romania has so far experienced the lowest rate of infection per capita (around 51,000 per 1 million people) - partly a product of relatively limited testing. The Czech Republic has fared the worst (more than 145,000 per 1M) (Figure 2), although we note that the 7-day average of Poland’s test positive rate, which represents the number of confirmed virus cases per 100 tests, is now at around 30%. This continues to outstrip the other three nations throughout the third wave of the virus. That being said, Poland’s COVID-19 death rate per 1 million people remains the second-lowest (1,473) after Romania (1,283), with the Czech Republic having the highest (2,548)*.Figure 3: COVID-19 Confirmed Cases and Deaths [per 1M people] [CEE] (as of 13/04) Source: Refinitiv Datastream Date: 13/04/2021As has been the case in other EU countries, vaccine progress in the CEE region has been rather slow. Most of them have distributed around 17 doses of the vaccine per 100 people at the time of writing. The outlier, Hungary, has distributed around 37 doses of vaccine per 100 people so far using the Russian (Sputnik V) and Chinese (Sinpoharm) vaccines. The pace of vaccinations eased somewhat in the EU and most CEE countries on two occasions: in mid-March (which we attribute to concerns regarding possible side effects of the AstraZeneca vaccine) and in early-April (which we attribute to the Easter holidays). Inoculations are, however, expected to accelerate in the next few months. Based on the available information, we expect the pace of vaccinations to increase notably in the region in the second and third quarters of 2021. Figure 4: COVID-19 vaccine doses administered [CEE] [per 100 people] (as of 13/04)

Source: Refinitiv Datastream Date: 13/04/2021As has been the case in other EU countries, vaccine progress in the CEE region has been rather slow. Most of them have distributed around 17 doses of the vaccine per 100 people at the time of writing. The outlier, Hungary, has distributed around 37 doses of vaccine per 100 people so far using the Russian (Sputnik V) and Chinese (Sinpoharm) vaccines. The pace of vaccinations eased somewhat in the EU and most CEE countries on two occasions: in mid-March (which we attribute to concerns regarding possible side effects of the AstraZeneca vaccine) and in early-April (which we attribute to the Easter holidays). Inoculations are, however, expected to accelerate in the next few months. Based on the available information, we expect the pace of vaccinations to increase notably in the region in the second and third quarters of 2021. Figure 4: COVID-19 vaccine doses administered [CEE] [per 100 people] (as of 13/04)

Source: Refinitiv Datastream Date: 13/04/2021Since our latest European forecast revision in December, most of the currencies in the region have seen gains reversed, with both internal and external factors turning unfavourable. The pandemic situation has worsened in the region since late-February, partly a result of the emergence of faster-spreading strains of the virus. The most rapid increase in new cases took place in the Czech Republic, where the 7-day moving average of new cases reached a peak in early-March, just below the previous one set in early-January. In other countries covered in this report, this peak in caseloads has taken longer, although the worst of the third wave of infection in the region as a whole tentatively appears to be behind us. Figure 2: New COVID-19 Cases [CEE] (March ‘20 - April ‘21)Source: Refinitiv Datastream Date: 13/04/2021Of the four countries, Romania has so far experienced the lowest rate of infection per capita (around 51,000 per 1 million people) - partly a product of relatively limited testing. The Czech Republic has fared the worst (more than 145,000 per 1M) (Figure 2), although we note that the 7-day average of Poland’s test positive rate, which represents the number of confirmed virus cases per 100 tests, is now at around 30%. This continues to outstrip the other three nations throughout the third wave of the virus. That being said, Poland’s COVID-19 death rate per 1 million people remains the second-lowest (1,473) after Romania (1,283), with the Czech Republic having the highest (2,548)*.Figure 3: COVID-19 Confirmed Cases and Deaths [per 1M people] [CEE] (as of 13/04)Source: Refinitiv Datastream Date: 13/04/2021As has been the case in other EU countries, vaccine progress in the CEE region has been rather slow. Most of them have distributed around 17 doses of the vaccine per 100 people at the time of writing. The outlier, Hungary, has distributed around 37 doses of vaccine per 100 people so far using the Russian (Sputnik V) and Chinese (Sinpoharm) vaccines. The pace of vaccinations eased somewhat in the EU and most CEE countries on two occasions: in mid-March (which we attribute to concerns regarding possible side effects of the AstraZeneca vaccine) and in early-April (which we attribute to the Easter holidays). Inoculations are, however, expected to accelerate in the next few months. Based on the available information, we expect the pace of vaccinations to increase notably in the region in the second and third quarters of 2021. Figure 4: COVID-19 vaccine doses administered [CEE] [per 100 people] (as of 13/04)