ECB February Meeting Preview: Will the ECB follow the Fed?

Like many of its global peers, the European Central Bank faces stubbornly high inflation. In contrast to many of them, the central bank has, so far, taken only limited steps towards exiting its ultra-loose policy. Is a shift towards higher rates about to get quicker?

Central Bank Meetings

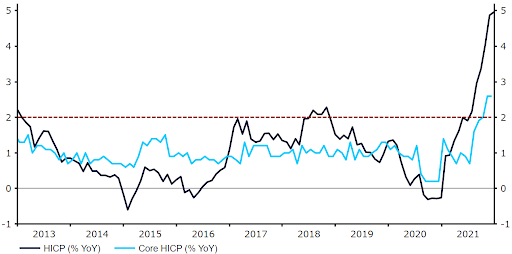

Like many of its global peers, the European Central Bank faces stubbornly high inflation. In contrast to many of them, the central bank has, so far, taken only limited steps towards exiting its ultra-loose policy. Is a shift towards higher rates about to get quicker?Last week’s communications after the Fed meeting were even more hawkish than the market expected. Following Powell’s comments, where he didn’t rule out rate increases at every meeting this year, the market priced in five US rate hikes in 2022 and EUR/USD fell below the 1.12 mark to its lowest level since June 2020 (Figure 1).Figure 1: EUR/USD (2021 - 2022) The Fed’s hawkish turn has added extra importance to this Thursday’s ECB meeting, as has the latest surprise to the upside in Eurozone inflation. Headline inflation increased to 5% in December, with core prices growing by 2.6%, both record highs.This inflation overshoot has caught the attention of policymakers, with a number of Governing Council members voicing some uneasiness over rising prices and, in particular, the ECB’s inflation forecast, which assumes price growth will decline markedly to 1.8% in 2023 and 2024.Figure 2: Euro Area Inflation Rate (2013 - 2021)

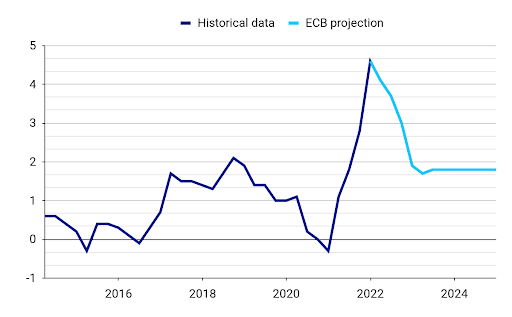

The Fed’s hawkish turn has added extra importance to this Thursday’s ECB meeting, as has the latest surprise to the upside in Eurozone inflation. Headline inflation increased to 5% in December, with core prices growing by 2.6%, both record highs.This inflation overshoot has caught the attention of policymakers, with a number of Governing Council members voicing some uneasiness over rising prices and, in particular, the ECB’s inflation forecast, which assumes price growth will decline markedly to 1.8% in 2023 and 2024.Figure 2: Euro Area Inflation Rate (2013 - 2021) While a number of members foresee inflation moderating before falling to target in the next two years, the hawkish voices among committee members appear to be getting louder. A representative of the hawkish wing of the ECB’s Governing Council, Robert Holzmann, recently suggested that the inflation outlook is highly uncertain and pointed to weakness of the ECB’s models. Vice President Luis de Guindos also said in mid-January that risks to inflation were ‘moderately tilted to the upside’ in the next twelve months, and that inflation may not be as transitory as believed some months prior.Figure 3: ECB December HICP Inflation Forecast [annual percentage changes] (2014 - 2024)

While a number of members foresee inflation moderating before falling to target in the next two years, the hawkish voices among committee members appear to be getting louder. A representative of the hawkish wing of the ECB’s Governing Council, Robert Holzmann, recently suggested that the inflation outlook is highly uncertain and pointed to weakness of the ECB’s models. Vice President Luis de Guindos also said in mid-January that risks to inflation were ‘moderately tilted to the upside’ in the next twelve months, and that inflation may not be as transitory as believed some months prior.Figure 3: ECB December HICP Inflation Forecast [annual percentage changes] (2014 - 2024)

The Fed’s hawkish turn has added extra importance to this Thursday’s ECB meeting, as has the latest surprise to the upside in Eurozone inflation. Headline inflation increased to 5% in December, with core prices growing by 2.6%, both record highs.This inflation overshoot has caught the attention of policymakers, with a number of Governing Council members voicing some uneasiness over rising prices and, in particular, the ECB’s inflation forecast, which assumes price growth will decline markedly to 1.8% in 2023 and 2024.Figure 2: Euro Area Inflation Rate (2013 - 2021)While a number of members foresee inflation moderating before falling to target in the next two years, the hawkish voices among committee members appear to be getting louder. A representative of the hawkish wing of the ECB’s Governing Council, Robert Holzmann, recently suggested that the inflation outlook is highly uncertain and pointed to weakness of the ECB’s models. Vice President Luis de Guindos also said in mid-January that risks to inflation were ‘moderately tilted to the upside’ in the next twelve months, and that inflation may not be as transitory as believed some months prior.Figure 3: ECB December HICP Inflation Forecast [annual percentage changes] (2014 - 2024)