Central banks return to the centre of attention

In light of its significant impact on public health and the global economy, the COVID-19 pandemic has been the number one topic of interest for financial markets since early-2020.

FX Market Updates

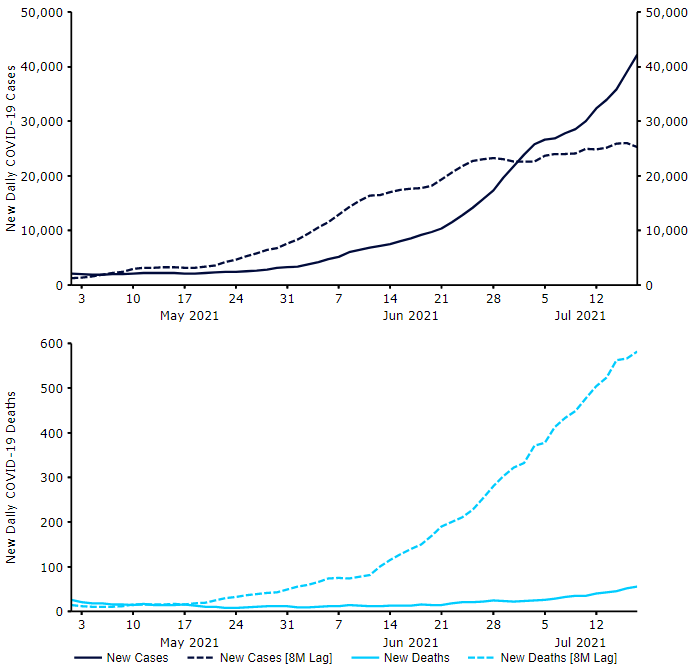

In light of its significant impact on public health and the global economy, the COVID-19 pandemic has been the number one topic of interest for financial markets since early-2020.The aggressive spread of the virus resulted in a serious reshuffling in the FX market, initially boosting safe-haven currencies and leaving a number of EM ones at all-time lows (Figure 1). Since the height of the market panic, those trends have, however, largely reversed with market sentiment recovering well of late following the successful vaccination campaigns in many countries, particularly developed ones. This has enabled an unwinding in the tough restrictions imposed as a result of the virus and has led to a broad revival of economic activity. We have seen significant improvements in a number of indicators, particularly the most timely and forward-looking PMI data.Figure 1: US Dollar Index vs. MSCI EM Currency Index [base = 100] (2020 - 2021) Source: Refinitiv Datastream Date: 27/07/2021The battle against the virus still has some way to go, but vaccinations have accelerated. In countries with high vaccination rates, the risk of significant curbs being reimposed has diminished, despite the fast spread of new variants. One of the main examples is the UK, where nearly 70% of the population have received at least one vaccine dose. While caseloads have rocketed back up to more than 40,000 per day this month, the number of new hospitalisations and deaths caused by the virus in this wave has, so far, been significantly lower than at the same stage in previous waves (Figure 2). The UK can be viewed as somewhat of a proxy for other developed nations with similar vaccination rates, particularly the US and most of the EU.Figure 2: UK New COVID-19 Cases & Deaths [2nd Wave vs. 3rd Wave]

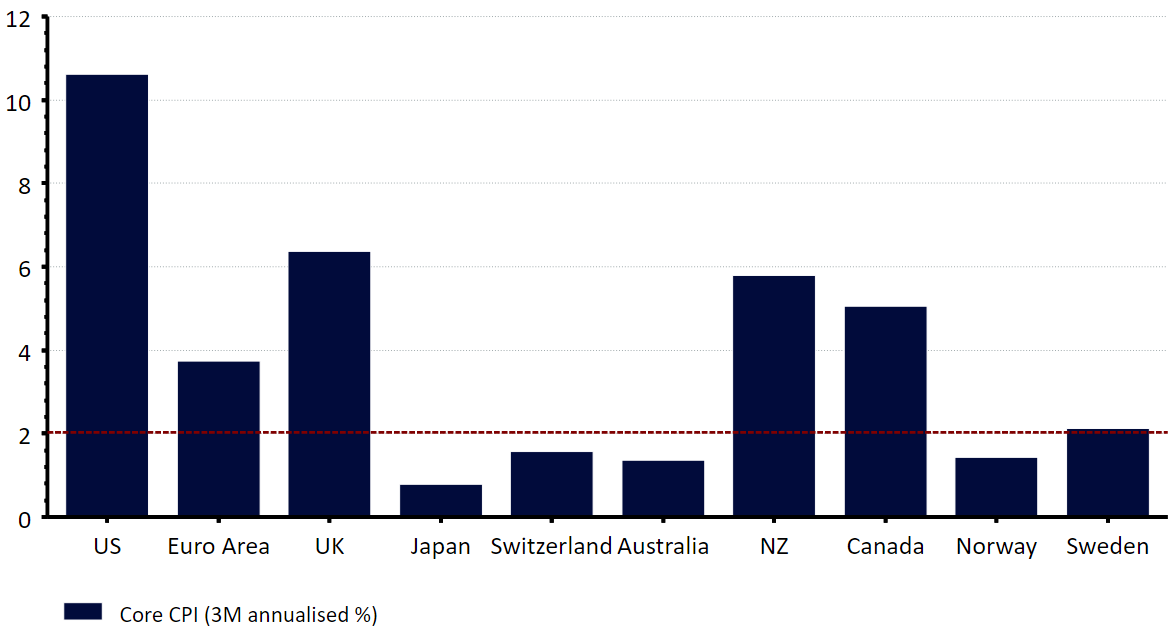

Source: Refinitiv Datastream Date: 27/07/2021The battle against the virus still has some way to go, but vaccinations have accelerated. In countries with high vaccination rates, the risk of significant curbs being reimposed has diminished, despite the fast spread of new variants. One of the main examples is the UK, where nearly 70% of the population have received at least one vaccine dose. While caseloads have rocketed back up to more than 40,000 per day this month, the number of new hospitalisations and deaths caused by the virus in this wave has, so far, been significantly lower than at the same stage in previous waves (Figure 2). The UK can be viewed as somewhat of a proxy for other developed nations with similar vaccination rates, particularly the US and most of the EU.Figure 2: UK New COVID-19 Cases & Deaths [2nd Wave vs. 3rd Wave] Source: Refinitiv Datastream Date: 27/07/2021Countries with low vaccination rates, particularly emerging market ones, remain vulnerable. In many of them the new variants have resulted in a significant increase in contagion levels. India has been a prime example of this, although we’ve also seen a surge in infection in other countries in Southeast Asia as a result of the delta variant. Now that most of the populations have been vaccinated in the key economic areas, risks related to the spread of these variants have largely eased. For the most part, we are seeing idiosyncratic moves in exchange rates of those countries that are posting sharp increases in cases coupled with significant jumps in hospitalisations and deaths.With vaccination programmes now in full swing, and inflationary pressures rising around the world, market attention has shifted towards the more conventional topic of monetary policy. Following the sharp increase in global inflation, we have witnessed a number of central banks becoming less dovish since the beginning of the year. A handful of emerging market ones have already begun the process of raising interest rates. In March, central banks in both Brazil and Russia commenced hiking cycles. Since then, both central banks have raised rates by a total of 225 basis points, while keeping the door open to further tightening.We saw similar developments in Central and Eastern Europe in June, with central banks in both Hungary and Czech Republic hiking rates and suggesting they might continue doing so at upcoming meetings. In the case of Hungary, it was the first such move in a decade and was followed by a larger-than-expected hike in July. Mexico also tightened policy in the summer, with Banxico unexpectedly hiking its base rate by 25 basis points to 4.25% in June, although it’s unclear whether this marks the start of a tightening cycle.The main developed economies have seen so far few actual steps towards monetary or fiscal tightening, but are seeing a tentative shift in tone nonetheless as inflationary pressures increase globally (Figure 3). A sharp increase in commodity prices, faster than expected rebounds in economic activity and a tightening in labour market conditions have forced major central banks to revise upwards their inflation projections. A number of policymakers expect the period of ultra-loose monetary policy to end sooner than previously thought.Figure 3: G10 3-month Annualised Core Inflation Rate (latest available)

Source: Refinitiv Datastream Date: 27/07/2021Countries with low vaccination rates, particularly emerging market ones, remain vulnerable. In many of them the new variants have resulted in a significant increase in contagion levels. India has been a prime example of this, although we’ve also seen a surge in infection in other countries in Southeast Asia as a result of the delta variant. Now that most of the populations have been vaccinated in the key economic areas, risks related to the spread of these variants have largely eased. For the most part, we are seeing idiosyncratic moves in exchange rates of those countries that are posting sharp increases in cases coupled with significant jumps in hospitalisations and deaths.With vaccination programmes now in full swing, and inflationary pressures rising around the world, market attention has shifted towards the more conventional topic of monetary policy. Following the sharp increase in global inflation, we have witnessed a number of central banks becoming less dovish since the beginning of the year. A handful of emerging market ones have already begun the process of raising interest rates. In March, central banks in both Brazil and Russia commenced hiking cycles. Since then, both central banks have raised rates by a total of 225 basis points, while keeping the door open to further tightening.We saw similar developments in Central and Eastern Europe in June, with central banks in both Hungary and Czech Republic hiking rates and suggesting they might continue doing so at upcoming meetings. In the case of Hungary, it was the first such move in a decade and was followed by a larger-than-expected hike in July. Mexico also tightened policy in the summer, with Banxico unexpectedly hiking its base rate by 25 basis points to 4.25% in June, although it’s unclear whether this marks the start of a tightening cycle.The main developed economies have seen so far few actual steps towards monetary or fiscal tightening, but are seeing a tentative shift in tone nonetheless as inflationary pressures increase globally (Figure 3). A sharp increase in commodity prices, faster than expected rebounds in economic activity and a tightening in labour market conditions have forced major central banks to revise upwards their inflation projections. A number of policymakers expect the period of ultra-loose monetary policy to end sooner than previously thought.Figure 3: G10 3-month Annualised Core Inflation Rate (latest available) Source: Refinitiv Datastream Date: 27/07/2021Looking at G10 countries, the Bank of Canada has already begun tapering its QE programme, reducing the pace of weekly purchases from CAD$4 billion to CAD$2 billion. The Bank of England slowed the pace of its weekly purchases from £4.4 billion from £3.4 billion in May, albeit emphasised that the action ‘should not be interpreted as a change in the stance of monetary policy’. Nonetheless, with the bank expecting inflation to reach 3% or more in late-2021, the need for tapering appears to have been brought forward. At its July meeting, the Reserve Bank of New Zealand also surprised investors by announcing it will end its NZ$100 billion QE programme effective on 23rd July.Among the G10 nations, a handful have already started talking about increasing interest rates or are, at least, flirting with the idea. We think that Norway is likely to be the first to raise rates. Norway is, however, somewhat of an outlier given that it has among the most negative real rates in the G10 and hasn’t launched a QE programme during the pandemic period. The bank’s June communication suggests that a hike may be just around the corner. Øystein Olsen, Norges Bank Governor, stated after the meeting that ‘the policy rate will most likely be raised in September’. New Zealand’s QE announcement has also raised expectations of higher rates, possibly as soon as the bank’s August meeting. We think we’ll see at least these two announce their first hikes before the end of 2021, with more G10 central banks set to commence their hiking cycle in 2022. The currencies of those G10 countries on course to raise rates before the end of 2022 look well placed to outperform and are, indeed, among those that we expect to perform the best over our forecast horizon.Figure 4: Expected Timing of G10 Interest Rate Hikes [based on market pricing*]

Source: Refinitiv Datastream Date: 27/07/2021Looking at G10 countries, the Bank of Canada has already begun tapering its QE programme, reducing the pace of weekly purchases from CAD$4 billion to CAD$2 billion. The Bank of England slowed the pace of its weekly purchases from £4.4 billion from £3.4 billion in May, albeit emphasised that the action ‘should not be interpreted as a change in the stance of monetary policy’. Nonetheless, with the bank expecting inflation to reach 3% or more in late-2021, the need for tapering appears to have been brought forward. At its July meeting, the Reserve Bank of New Zealand also surprised investors by announcing it will end its NZ$100 billion QE programme effective on 23rd July.Among the G10 nations, a handful have already started talking about increasing interest rates or are, at least, flirting with the idea. We think that Norway is likely to be the first to raise rates. Norway is, however, somewhat of an outlier given that it has among the most negative real rates in the G10 and hasn’t launched a QE programme during the pandemic period. The bank’s June communication suggests that a hike may be just around the corner. Øystein Olsen, Norges Bank Governor, stated after the meeting that ‘the policy rate will most likely be raised in September’. New Zealand’s QE announcement has also raised expectations of higher rates, possibly as soon as the bank’s August meeting. We think we’ll see at least these two announce their first hikes before the end of 2021, with more G10 central banks set to commence their hiking cycle in 2022. The currencies of those G10 countries on course to raise rates before the end of 2022 look well placed to outperform and are, indeed, among those that we expect to perform the best over our forecast horizon.Figure 4: Expected Timing of G10 Interest Rate Hikes [based on market pricing*]

Source: Refinitiv Datastream Date: 27/07/2021The battle against the virus still has some way to go, but vaccinations have accelerated. In countries with high vaccination rates, the risk of significant curbs being reimposed has diminished, despite the fast spread of new variants. One of the main examples is the UK, where nearly 70% of the population have received at least one vaccine dose. While caseloads have rocketed back up to more than 40,000 per day this month, the number of new hospitalisations and deaths caused by the virus in this wave has, so far, been significantly lower than at the same stage in previous waves (Figure 2). The UK can be viewed as somewhat of a proxy for other developed nations with similar vaccination rates, particularly the US and most of the EU.Figure 2: UK New COVID-19 Cases & Deaths [2nd Wave vs. 3rd Wave]Source: Refinitiv Datastream Date: 27/07/2021Countries with low vaccination rates, particularly emerging market ones, remain vulnerable. In many of them the new variants have resulted in a significant increase in contagion levels. India has been a prime example of this, although we’ve also seen a surge in infection in other countries in Southeast Asia as a result of the delta variant. Now that most of the populations have been vaccinated in the key economic areas, risks related to the spread of these variants have largely eased. For the most part, we are seeing idiosyncratic moves in exchange rates of those countries that are posting sharp increases in cases coupled with significant jumps in hospitalisations and deaths.With vaccination programmes now in full swing, and inflationary pressures rising around the world, market attention has shifted towards the more conventional topic of monetary policy. Following the sharp increase in global inflation, we have witnessed a number of central banks becoming less dovish since the beginning of the year. A handful of emerging market ones have already begun the process of raising interest rates. In March, central banks in both Brazil and Russia commenced hiking cycles. Since then, both central banks have raised rates by a total of 225 basis points, while keeping the door open to further tightening.We saw similar developments in Central and Eastern Europe in June, with central banks in both Hungary and Czech Republic hiking rates and suggesting they might continue doing so at upcoming meetings. In the case of Hungary, it was the first such move in a decade and was followed by a larger-than-expected hike in July. Mexico also tightened policy in the summer, with Banxico unexpectedly hiking its base rate by 25 basis points to 4.25% in June, although it’s unclear whether this marks the start of a tightening cycle.The main developed economies have seen so far few actual steps towards monetary or fiscal tightening, but are seeing a tentative shift in tone nonetheless as inflationary pressures increase globally (Figure 3). A sharp increase in commodity prices, faster than expected rebounds in economic activity and a tightening in labour market conditions have forced major central banks to revise upwards their inflation projections. A number of policymakers expect the period of ultra-loose monetary policy to end sooner than previously thought.Figure 3: G10 3-month Annualised Core Inflation Rate (latest available)Source: Refinitiv Datastream Date: 27/07/2021Looking at G10 countries, the Bank of Canada has already begun tapering its QE programme, reducing the pace of weekly purchases from CAD$4 billion to CAD$2 billion. The Bank of England slowed the pace of its weekly purchases from £4.4 billion from £3.4 billion in May, albeit emphasised that the action ‘should not be interpreted as a change in the stance of monetary policy’. Nonetheless, with the bank expecting inflation to reach 3% or more in late-2021, the need for tapering appears to have been brought forward. At its July meeting, the Reserve Bank of New Zealand also surprised investors by announcing it will end its NZ$100 billion QE programme effective on 23rd July.Among the G10 nations, a handful have already started talking about increasing interest rates or are, at least, flirting with the idea. We think that Norway is likely to be the first to raise rates. Norway is, however, somewhat of an outlier given that it has among the most negative real rates in the G10 and hasn’t launched a QE programme during the pandemic period. The bank’s June communication suggests that a hike may be just around the corner. Øystein Olsen, Norges Bank Governor, stated after the meeting that ‘the policy rate will most likely be raised in September’. New Zealand’s QE announcement has also raised expectations of higher rates, possibly as soon as the bank’s August meeting. We think we’ll see at least these two announce their first hikes before the end of 2021, with more G10 central banks set to commence their hiking cycle in 2022. The currencies of those G10 countries on course to raise rates before the end of 2022 look well placed to outperform and are, indeed, among those that we expect to perform the best over our forecast horizon.Figure 4: Expected Timing of G10 Interest Rate Hikes [based on market pricing*]