BRICS FX Forecast Special Report

How has Covid-19 affected the BRICS countries? Read our latest Special FX Forecast report

FX Market Updates

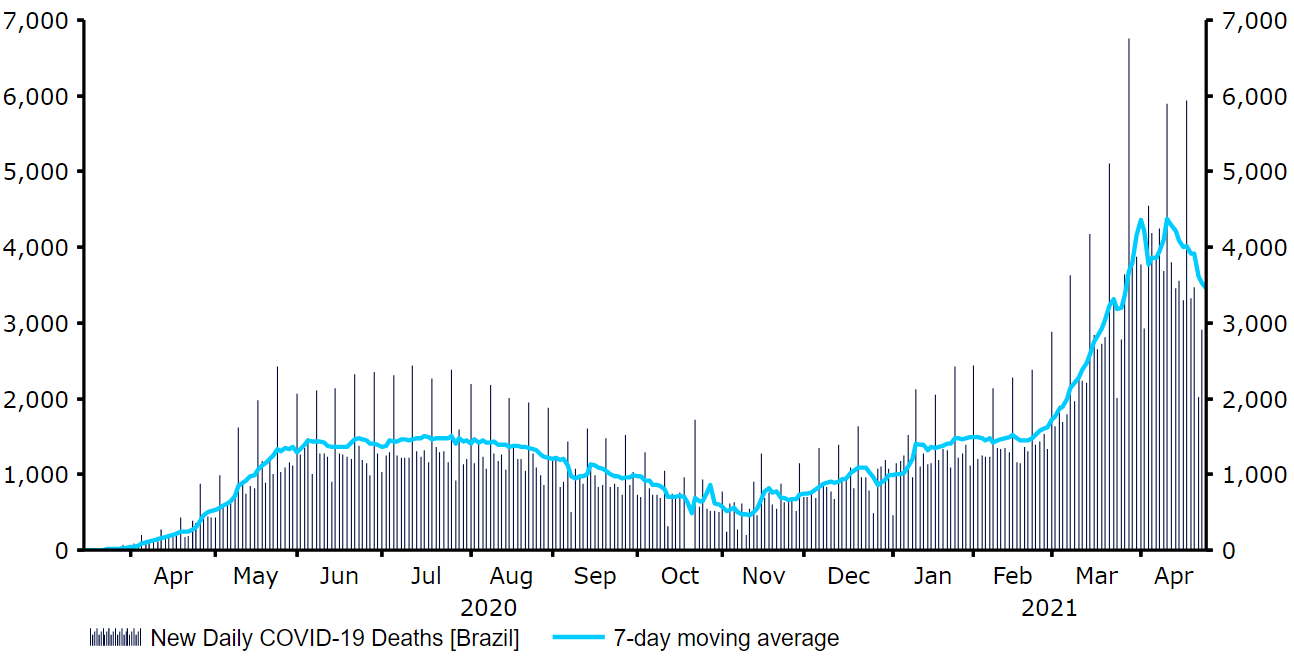

How has Covid-19 affected the BRICS countries? Read our latest Special FX Forecast report or download it here.Focus on: Brazilian Real, Chinese Yuan, Russian Ruble, South African Rand and Indian Rupee. Source: Refinitiv Datastream Date: 27/04/2021Ongoing criticism of authorities’ handling of the pandemic has significantly soured sentiment towards the real since the early stages of the crisis. Far-right President Jair Bolsonaro has adopted a troublesome approach to dealing with the pandemic. Bolsonaro has actively encouraged people to defy social distancing, ignore regional lockdown and partake in large gatherings. As a consequence, Brazil has racked up the second highest number of COVID-related deaths in the world, behind only the far more populous US, despite relatively limited levels of testing. Brazil now accounts for 12.5% of the world’s COVID-19 death toll, despite only making up 2.7% just of the population. The latest wave of infection has been the worst so far, in large part due to the prevalence of the P.1 strain of the virus that was first identified in January. This variant is said to not only be twice as contagious as the original strain, but also more than 60% likely to reinfect people than other versions of the COVID-19 virus. Hospital admissions have surged in Brazil, with many intensive care units reportedly either at or close to full capacity. Bolsonaro has, however, continued to criticise regional state governors for enforcing lockdowns, with the president instead prioritising the health of the economy. Deaths caused by the virus surged to record highs above 4,000 a day in early-April (Figure 2), and have remained elevated ever since. Authorities in Brazil have also been rather slow to both approve and adminiterd the various COVID vaccines - so far only approximately 18 vaccine doses per 100 people have been administered in Brazil, not too far above the world average.Figure 2: Brazil New COVID-19 Deaths (April ‘20 - April ‘21)

Source: Refinitiv Datastream Date: 27/04/2021Ongoing criticism of authorities’ handling of the pandemic has significantly soured sentiment towards the real since the early stages of the crisis. Far-right President Jair Bolsonaro has adopted a troublesome approach to dealing with the pandemic. Bolsonaro has actively encouraged people to defy social distancing, ignore regional lockdown and partake in large gatherings. As a consequence, Brazil has racked up the second highest number of COVID-related deaths in the world, behind only the far more populous US, despite relatively limited levels of testing. Brazil now accounts for 12.5% of the world’s COVID-19 death toll, despite only making up 2.7% just of the population. The latest wave of infection has been the worst so far, in large part due to the prevalence of the P.1 strain of the virus that was first identified in January. This variant is said to not only be twice as contagious as the original strain, but also more than 60% likely to reinfect people than other versions of the COVID-19 virus. Hospital admissions have surged in Brazil, with many intensive care units reportedly either at or close to full capacity. Bolsonaro has, however, continued to criticise regional state governors for enforcing lockdowns, with the president instead prioritising the health of the economy. Deaths caused by the virus surged to record highs above 4,000 a day in early-April (Figure 2), and have remained elevated ever since. Authorities in Brazil have also been rather slow to both approve and adminiterd the various COVID vaccines - so far only approximately 18 vaccine doses per 100 people have been administered in Brazil, not too far above the world average.Figure 2: Brazil New COVID-19 Deaths (April ‘20 - April ‘21) Source: Refinitiv Datastream Date: 27/04/2021We do, however, think that the real has been spared even larger losses by the hawkish policy stance adopted by the Central Bank of Brazil. The central bank raised interest rates by a larger-than-expected 75 basis points to 2.75% in March, the first in six years, while also suggesting that a hike of the same magnitude was on the way at the bank’s May meeting. The decision to raise rates this early has been controversial, but policymakers have cited the recent increase in domestic inflation, which rose above 6% in March for the first time in more than four years. The rate setting committee noted in its March communications ‘barring a significant change in inflation projections or the balance of risks facing the economy, the committee foresees continuing the process of partially winding down its monetary stimulus with another adjustment of the same magnitude [in May].’ The decision to engage in a tightening cycle is a bold one, given the current challenges to growth. Brazil’s economy has bounced back strongly following last year’s recession, registering positive growth of 7.7% and 3.2% QoQ in Q3 and Q4 respectively. The government is, however, coming under increasing pressure to enforce tougher lockdown restrictions. Heads of Brazil’s army, navy and airforce all resigned in opposition of Bolsonaro’s covid policies in March, with the president’s approval rating also plunging to around 30%.Despite the clearly concerning pandemic situation in the country, we are encouraged by Brazil’s strong macroeconomic fundamentals. These should, in our view, allow BRL to recover most of its recent losses once the pandemic is brought under control:1. Still high, albeit declining, FX reserves that equate to more than 15 months’ worth of import cover (Figure 3). This remains an ample level of ammunition for the Central Bank of Brazil to successfully intervene in the market in order to reverse the currency’s sell-off. The central bank has been increasingly active in the FX market in recent weeks, selling around $5.6 billion in the spot FX market and $6 billion in the FX swaps market in the first two-and-a-half months of the year alone. We expect this proactivity to continue in the near-term. Figure 3: Brazil FX Reserves (2000 - 2021)

Source: Refinitiv Datastream Date: 27/04/2021We do, however, think that the real has been spared even larger losses by the hawkish policy stance adopted by the Central Bank of Brazil. The central bank raised interest rates by a larger-than-expected 75 basis points to 2.75% in March, the first in six years, while also suggesting that a hike of the same magnitude was on the way at the bank’s May meeting. The decision to raise rates this early has been controversial, but policymakers have cited the recent increase in domestic inflation, which rose above 6% in March for the first time in more than four years. The rate setting committee noted in its March communications ‘barring a significant change in inflation projections or the balance of risks facing the economy, the committee foresees continuing the process of partially winding down its monetary stimulus with another adjustment of the same magnitude [in May].’ The decision to engage in a tightening cycle is a bold one, given the current challenges to growth. Brazil’s economy has bounced back strongly following last year’s recession, registering positive growth of 7.7% and 3.2% QoQ in Q3 and Q4 respectively. The government is, however, coming under increasing pressure to enforce tougher lockdown restrictions. Heads of Brazil’s army, navy and airforce all resigned in opposition of Bolsonaro’s covid policies in March, with the president’s approval rating also plunging to around 30%.Despite the clearly concerning pandemic situation in the country, we are encouraged by Brazil’s strong macroeconomic fundamentals. These should, in our view, allow BRL to recover most of its recent losses once the pandemic is brought under control:1. Still high, albeit declining, FX reserves that equate to more than 15 months’ worth of import cover (Figure 3). This remains an ample level of ammunition for the Central Bank of Brazil to successfully intervene in the market in order to reverse the currency’s sell-off. The central bank has been increasingly active in the FX market in recent weeks, selling around $5.6 billion in the spot FX market and $6 billion in the FX swaps market in the first two-and-a-half months of the year alone. We expect this proactivity to continue in the near-term. Figure 3: Brazil FX Reserves (2000 - 2021)  Source: Refinitiv Datastream Date: 27/04/20212. A manageable current account deficit that remains comfortably financed by foreign direct investment (FDI). This deficit decreased to 0.7% in 2020 from 2.7% in 2019. An increase in Brazil’s external debt since the start of the COVID-19 pandemic to relatively high levels is a slight cause for concern, although as a percentage of GDP debt eased in the second half of last year to 37.2% of GDP. The recent sharp depreciation in BRL does, however, increase the real value of the debt payments. Given the above supportive factors, and our view that the currency is very cheap at current levels, we do not think that a continued sell-off in the real at the rate witnessed since the onset of the crisis is likely in the long-term. We are instead continuing to pencil in a recovery for the currency against the dollar through to the end of 2021, and think that Brazil’s solid macroeconomic fundamentals should allow the currency to successfully bounce back once the worst of the crisis is over. This view is reinforced by the hawkish policy stance adopted by the Central Bank of Brazil, which looks likely to continue raising rates in 2021.That being said, we are revising our near-term forecasts slightly higher in acknowledgment of the worsening pandemic situation in Brazil in recent weeks.

Source: Refinitiv Datastream Date: 27/04/20212. A manageable current account deficit that remains comfortably financed by foreign direct investment (FDI). This deficit decreased to 0.7% in 2020 from 2.7% in 2019. An increase in Brazil’s external debt since the start of the COVID-19 pandemic to relatively high levels is a slight cause for concern, although as a percentage of GDP debt eased in the second half of last year to 37.2% of GDP. The recent sharp depreciation in BRL does, however, increase the real value of the debt payments. Given the above supportive factors, and our view that the currency is very cheap at current levels, we do not think that a continued sell-off in the real at the rate witnessed since the onset of the crisis is likely in the long-term. We are instead continuing to pencil in a recovery for the currency against the dollar through to the end of 2021, and think that Brazil’s solid macroeconomic fundamentals should allow the currency to successfully bounce back once the worst of the crisis is over. This view is reinforced by the hawkish policy stance adopted by the Central Bank of Brazil, which looks likely to continue raising rates in 2021.That being said, we are revising our near-term forecasts slightly higher in acknowledgment of the worsening pandemic situation in Brazil in recent weeks.

Brazilian Real (BRL)

The Brazilian real (BRL) remains one of the worst performing currencies in the world since the start of the COVID-19 pandemic. The currency lost around one-quarter of its value against the US dollar in the first four-and-a-half months of last year, falling to just shy of 6 to the US dollar in May 2020, its lowest ever level. By June last year, BRL had recovered almost half of these losses, although it has since sold-off again, bouncing around the 5.5 level (Figure 1). The real has been the worst performing major emerging market currency in the world since the start of last year.Figure 1: USD/BRL (April ‘20 - April ‘21)Source: Refinitiv Datastream Date: 27/04/2021Ongoing criticism of authorities’ handling of the pandemic has significantly soured sentiment towards the real since the early stages of the crisis. Far-right President Jair Bolsonaro has adopted a troublesome approach to dealing with the pandemic. Bolsonaro has actively encouraged people to defy social distancing, ignore regional lockdown and partake in large gatherings. As a consequence, Brazil has racked up the second highest number of COVID-related deaths in the world, behind only the far more populous US, despite relatively limited levels of testing. Brazil now accounts for 12.5% of the world’s COVID-19 death toll, despite only making up 2.7% just of the population. The latest wave of infection has been the worst so far, in large part due to the prevalence of the P.1 strain of the virus that was first identified in January. This variant is said to not only be twice as contagious as the original strain, but also more than 60% likely to reinfect people than other versions of the COVID-19 virus. Hospital admissions have surged in Brazil, with many intensive care units reportedly either at or close to full capacity. Bolsonaro has, however, continued to criticise regional state governors for enforcing lockdowns, with the president instead prioritising the health of the economy. Deaths caused by the virus surged to record highs above 4,000 a day in early-April (Figure 2), and have remained elevated ever since. Authorities in Brazil have also been rather slow to both approve and adminiterd the various COVID vaccines - so far only approximately 18 vaccine doses per 100 people have been administered in Brazil, not too far above the world average.Figure 2: Brazil New COVID-19 Deaths (April ‘20 - April ‘21)Source: Refinitiv Datastream Date: 27/04/2021We do, however, think that the real has been spared even larger losses by the hawkish policy stance adopted by the Central Bank of Brazil. The central bank raised interest rates by a larger-than-expected 75 basis points to 2.75% in March, the first in six years, while also suggesting that a hike of the same magnitude was on the way at the bank’s May meeting. The decision to raise rates this early has been controversial, but policymakers have cited the recent increase in domestic inflation, which rose above 6% in March for the first time in more than four years. The rate setting committee noted in its March communications ‘barring a significant change in inflation projections or the balance of risks facing the economy, the committee foresees continuing the process of partially winding down its monetary stimulus with another adjustment of the same magnitude [in May].’ The decision to engage in a tightening cycle is a bold one, given the current challenges to growth. Brazil’s economy has bounced back strongly following last year’s recession, registering positive growth of 7.7% and 3.2% QoQ in Q3 and Q4 respectively. The government is, however, coming under increasing pressure to enforce tougher lockdown restrictions. Heads of Brazil’s army, navy and airforce all resigned in opposition of Bolsonaro’s covid policies in March, with the president’s approval rating also plunging to around 30%.Despite the clearly concerning pandemic situation in the country, we are encouraged by Brazil’s strong macroeconomic fundamentals. These should, in our view, allow BRL to recover most of its recent losses once the pandemic is brought under control:1. Still high, albeit declining, FX reserves that equate to more than 15 months’ worth of import cover (Figure 3). This remains an ample level of ammunition for the Central Bank of Brazil to successfully intervene in the market in order to reverse the currency’s sell-off. The central bank has been increasingly active in the FX market in recent weeks, selling around $5.6 billion in the spot FX market and $6 billion in the FX swaps market in the first two-and-a-half months of the year alone. We expect this proactivity to continue in the near-term. Figure 3: Brazil FX Reserves (2000 - 2021) Source: Refinitiv Datastream Date: 27/04/20212. A manageable current account deficit that remains comfortably financed by foreign direct investment (FDI). This deficit decreased to 0.7% in 2020 from 2.7% in 2019. An increase in Brazil’s external debt since the start of the COVID-19 pandemic to relatively high levels is a slight cause for concern, although as a percentage of GDP debt eased in the second half of last year to 37.2% of GDP. The recent sharp depreciation in BRL does, however, increase the real value of the debt payments. Given the above supportive factors, and our view that the currency is very cheap at current levels, we do not think that a continued sell-off in the real at the rate witnessed since the onset of the crisis is likely in the long-term. We are instead continuing to pencil in a recovery for the currency against the dollar through to the end of 2021, and think that Brazil’s solid macroeconomic fundamentals should allow the currency to successfully bounce back once the worst of the crisis is over. This view is reinforced by the hawkish policy stance adopted by the Central Bank of Brazil, which looks likely to continue raising rates in 2021.That being said, we are revising our near-term forecasts slightly higher in acknowledgment of the worsening pandemic situation in Brazil in recent weeks.