Dollar stabilises as markets shift focus to FOMC rate decision

The clearing out of stale dollar long positions over the last few weeks appears to have allowed the greenback to stabilise somewhat after its sharp sell-off so far in March.

FX Market Updates

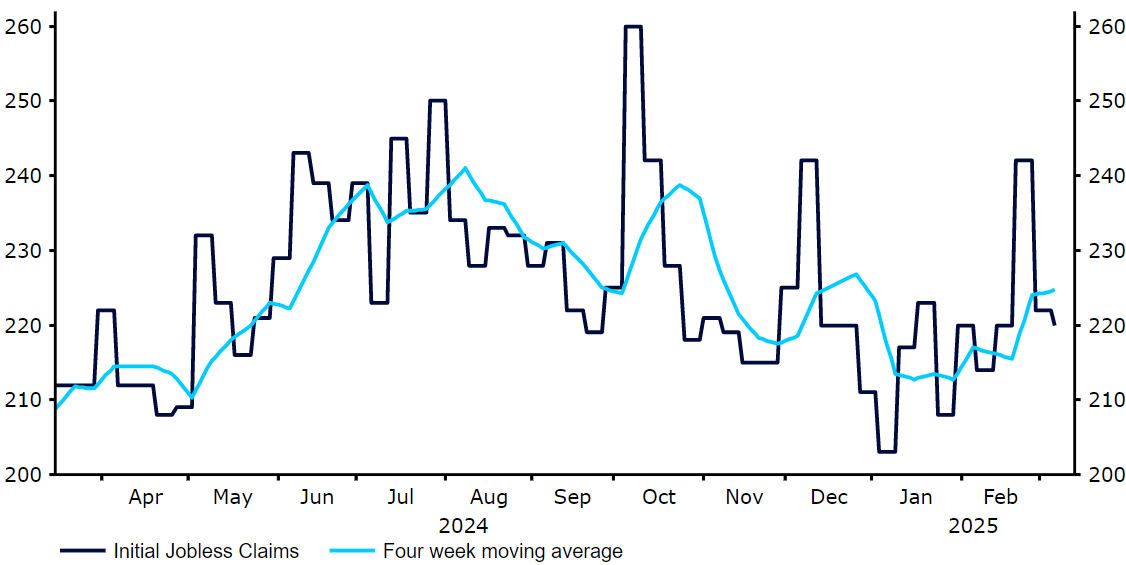

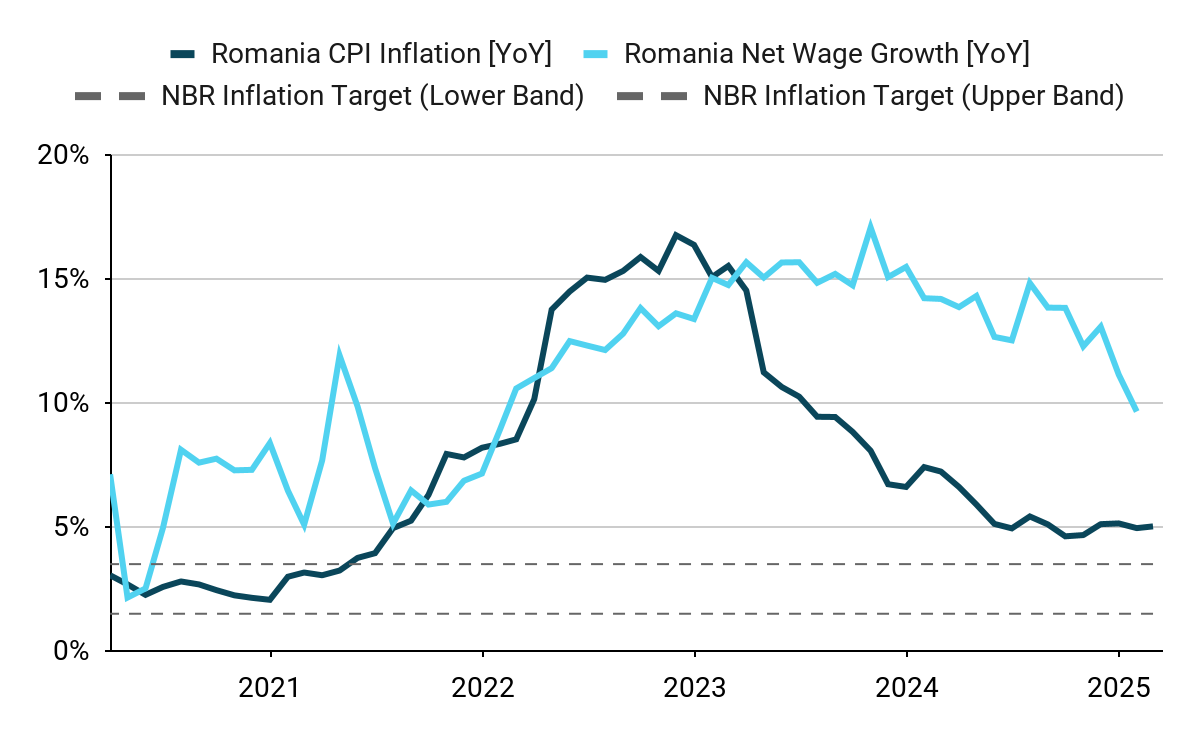

The clearing out of stale dollar long positions over the last few weeks appears to have allowed the greenback to stabilise somewhat after its sharp sell-off so far in March.This mild rebound in the dollar has happened even as President Trump continues dropping tape bombs on tariffs, and stocks and credit drop in tandem as investors grow fearful about the possibility of a slowdown in the US economy. We think that recent data out of the world’s largest economy has been disappointing, but not disastrous, and that there are reasons to believe that fears over a dreaded recession are currently overdone. For more of our thoughts on this, read our latest report covering the fallout and economic and geopolitical ramifications of Trump’s first 50 days in office.It's just possible that the spotlight this week will temporarily shift away from Trump's erratic policies and towards the raft of central bank announcements on tap. In the span of less than 24 hours from Wednesday to Thursday we will hear from the Fed, the BoJ, the Riksbank, the BoE and the SNB. Of those, only the last one is expected to lower rates, but markets will be closely following the Fed’s and the BoE's reaction to the apparent slowdown experienced by both economies.USDFears of a US economic slowdown, brought on by Trump's erratic policymaking and hefty import levies, have driven down US stocks and the dollar in the last few weeks. Interestingly, Treasury yields have not moved down in tandem, as one would expect, and are fairly close to where they were when the stock market sell off began. We note that labour market data out of the US economy has yet to indicate any meaningful weakening. This includes the most timely read on the jobs markets, initial jobless claims, which are largely continuing to hover at very healthy levels around the 220k mark.The Federal Reserve will likely commit to a wait-and-see stance this week. There will be no change in rates, and the updated ‘dot plot’ will probably leave options open to lower rates at only a gradual pace. With a potential slowdown in the US economy on the way, the raft of economic reports out this week will take on added importance, in particular retail sales figures for February (Monday).Figure 1: US Initial Jobless Claims (2024 - 2025) Source: LSEG Datastream Date: 17/03/2025EURThe euro continues to ride the wave of optimism around massive German fiscal loosening and the tweaking to the debt brake, which was agreed upon in the Bundestag last week. The deal will allow Europe’s largest economy to massively overhaul its fiscal policy, enabling a €500 billion infrastructure investment over the next decade or so, and an exemption that will allow defence spending to rise above 1% of the country’s GDP. Markets are betting that the news will provide a much needed boost to the economy, while also limiting the need for further aggressive interest rate cuts from the ECB, both of which are bullish for the euro.Hints of capital reallocation from US stocks to cheaper European ones, a thesis supported by the strong outperformance in the latter in 2025, also appear to be providing the euro with some tailwinds. In a week with little newsflow of note out of the Eurozone, we expect tariff headlines to be the main driver of the common currency. GBPThe Bank of England is expected to hold interest rates at a relatively high 4.5% level at its March meeting on Thursday, with swap markets currently pricing in no more than around a 1-in-10 chance of another cut. Of greater unpredictability will be the actual voting split among MPC members. All nine officials on the committee were in support of an immediate rate reduction at the last meeting in February, with two unexpectedly opting for a 50bp cut. We suspect that the vote will be split 7-2 on this occasion, with the two hawks to favour a 25bp move, while the rest vote for no change.Prior to the meeting, however, we will get some crucial labour market data for January and February. Arguably the most important will be the wage growth figures, which are expected to remain around 6% - a level incompatible with a return to inflation targets, hence the Bank of England's caution. It will be interesting to see whether the government’s NI business tax raid is reflected in the data. If so, we could see some softness in GBP this week.RONInflation, which has remained almost unchanged since November, oscillating around the 5% level, continued to be the main theme in Romania too. What is perhaps more interesting is, however, wage growth, posted an increasde over the previous month for the first time since September, coming in at 11.7%. At still double-digit levels, it is a very serious pro-inflationary threat. As in Poland and Hungary, it is difficult to expect the NBR to cut rates in the coming months.Figure 2: Romania CPI Inflation & Net Wage Growth [YoY, NSA] (2020 - 2025)

Source: LSEG Datastream Date: 17/03/2025EURThe euro continues to ride the wave of optimism around massive German fiscal loosening and the tweaking to the debt brake, which was agreed upon in the Bundestag last week. The deal will allow Europe’s largest economy to massively overhaul its fiscal policy, enabling a €500 billion infrastructure investment over the next decade or so, and an exemption that will allow defence spending to rise above 1% of the country’s GDP. Markets are betting that the news will provide a much needed boost to the economy, while also limiting the need for further aggressive interest rate cuts from the ECB, both of which are bullish for the euro.Hints of capital reallocation from US stocks to cheaper European ones, a thesis supported by the strong outperformance in the latter in 2025, also appear to be providing the euro with some tailwinds. In a week with little newsflow of note out of the Eurozone, we expect tariff headlines to be the main driver of the common currency. GBPThe Bank of England is expected to hold interest rates at a relatively high 4.5% level at its March meeting on Thursday, with swap markets currently pricing in no more than around a 1-in-10 chance of another cut. Of greater unpredictability will be the actual voting split among MPC members. All nine officials on the committee were in support of an immediate rate reduction at the last meeting in February, with two unexpectedly opting for a 50bp cut. We suspect that the vote will be split 7-2 on this occasion, with the two hawks to favour a 25bp move, while the rest vote for no change.Prior to the meeting, however, we will get some crucial labour market data for January and February. Arguably the most important will be the wage growth figures, which are expected to remain around 6% - a level incompatible with a return to inflation targets, hence the Bank of England's caution. It will be interesting to see whether the government’s NI business tax raid is reflected in the data. If so, we could see some softness in GBP this week.RONInflation, which has remained almost unchanged since November, oscillating around the 5% level, continued to be the main theme in Romania too. What is perhaps more interesting is, however, wage growth, posted an increasde over the previous month for the first time since September, coming in at 11.7%. At still double-digit levels, it is a very serious pro-inflationary threat. As in Poland and Hungary, it is difficult to expect the NBR to cut rates in the coming months.Figure 2: Romania CPI Inflation & Net Wage Growth [YoY, NSA] (2020 - 2025) Source: Bloomberg, 17/03/2025A crucial thread is also, obviously, a presidential election re-run, which, as Romania's Central Electoral Bureau (BEC) has announced, will not feature Calin Georgescu, the winner of the first round of the primary vote. The first polls indicate a strong position of the far right (George Simion or Anamaria Gavrila). However, the same polls suggest that the second round should end in a victory for the centrist mayor of Bucharest, Nicusor Dan. Yet, worth recalling, same polls have proved highly inaccurate last year. HUFInflation again exceeded expectations, coming in at the highest level in 15 months (5.6%) in February. More importantly, however, the 3MAA points to inflation exceeding 10% for both measures for the second month in a row. It could be said that the conclusion is simple - the first meeting under Mihaly Varga's tenure will certainly not bring an interest rate cut. However, lately, a discussion over an interest rate hike sparked, with some economists finding it viable. In our opinion, these speculations are a bit over the top, particularly looking at the food price cap introduced by the Hungarian government in the past few days, which should have a somewhat delayed effect on the economy.Figure 3: Hungary CPI & Core CPI Inflation [3MAA, NSA] (2020 - 2025)

Source: Bloomberg, 17/03/2025A crucial thread is also, obviously, a presidential election re-run, which, as Romania's Central Electoral Bureau (BEC) has announced, will not feature Calin Georgescu, the winner of the first round of the primary vote. The first polls indicate a strong position of the far right (George Simion or Anamaria Gavrila). However, the same polls suggest that the second round should end in a victory for the centrist mayor of Bucharest, Nicusor Dan. Yet, worth recalling, same polls have proved highly inaccurate last year. HUFInflation again exceeded expectations, coming in at the highest level in 15 months (5.6%) in February. More importantly, however, the 3MAA points to inflation exceeding 10% for both measures for the second month in a row. It could be said that the conclusion is simple - the first meeting under Mihaly Varga's tenure will certainly not bring an interest rate cut. However, lately, a discussion over an interest rate hike sparked, with some economists finding it viable. In our opinion, these speculations are a bit over the top, particularly looking at the food price cap introduced by the Hungarian government in the past few days, which should have a somewhat delayed effect on the economy.Figure 3: Hungary CPI & Core CPI Inflation [3MAA, NSA] (2020 - 2025)

Source: LSEG Datastream Date: 17/03/2025EURThe euro continues to ride the wave of optimism around massive German fiscal loosening and the tweaking to the debt brake, which was agreed upon in the Bundestag last week. The deal will allow Europe’s largest economy to massively overhaul its fiscal policy, enabling a €500 billion infrastructure investment over the next decade or so, and an exemption that will allow defence spending to rise above 1% of the country’s GDP. Markets are betting that the news will provide a much needed boost to the economy, while also limiting the need for further aggressive interest rate cuts from the ECB, both of which are bullish for the euro.Hints of capital reallocation from US stocks to cheaper European ones, a thesis supported by the strong outperformance in the latter in 2025, also appear to be providing the euro with some tailwinds. In a week with little newsflow of note out of the Eurozone, we expect tariff headlines to be the main driver of the common currency. GBPThe Bank of England is expected to hold interest rates at a relatively high 4.5% level at its March meeting on Thursday, with swap markets currently pricing in no more than around a 1-in-10 chance of another cut. Of greater unpredictability will be the actual voting split among MPC members. All nine officials on the committee were in support of an immediate rate reduction at the last meeting in February, with two unexpectedly opting for a 50bp cut. We suspect that the vote will be split 7-2 on this occasion, with the two hawks to favour a 25bp move, while the rest vote for no change.Prior to the meeting, however, we will get some crucial labour market data for January and February. Arguably the most important will be the wage growth figures, which are expected to remain around 6% - a level incompatible with a return to inflation targets, hence the Bank of England's caution. It will be interesting to see whether the government’s NI business tax raid is reflected in the data. If so, we could see some softness in GBP this week.RONInflation, which has remained almost unchanged since November, oscillating around the 5% level, continued to be the main theme in Romania too. What is perhaps more interesting is, however, wage growth, posted an increasde over the previous month for the first time since September, coming in at 11.7%. At still double-digit levels, it is a very serious pro-inflationary threat. As in Poland and Hungary, it is difficult to expect the NBR to cut rates in the coming months.Figure 2: Romania CPI Inflation & Net Wage Growth [YoY, NSA] (2020 - 2025)Source: Bloomberg, 17/03/2025A crucial thread is also, obviously, a presidential election re-run, which, as Romania's Central Electoral Bureau (BEC) has announced, will not feature Calin Georgescu, the winner of the first round of the primary vote. The first polls indicate a strong position of the far right (George Simion or Anamaria Gavrila). However, the same polls suggest that the second round should end in a victory for the centrist mayor of Bucharest, Nicusor Dan. Yet, worth recalling, same polls have proved highly inaccurate last year. HUFInflation again exceeded expectations, coming in at the highest level in 15 months (5.6%) in February. More importantly, however, the 3MAA points to inflation exceeding 10% for both measures for the second month in a row. It could be said that the conclusion is simple - the first meeting under Mihaly Varga's tenure will certainly not bring an interest rate cut. However, lately, a discussion over an interest rate hike sparked, with some economists finding it viable. In our opinion, these speculations are a bit over the top, particularly looking at the food price cap introduced by the Hungarian government in the past few days, which should have a somewhat delayed effect on the economy.Figure 3: Hungary CPI & Core CPI Inflation [3MAA, NSA] (2020 - 2025)