Dollar rally on pause ahead of Trump inauguration

Financial markets breathed easier after better than expected inflation data out of the US last week.

FX Market Updates

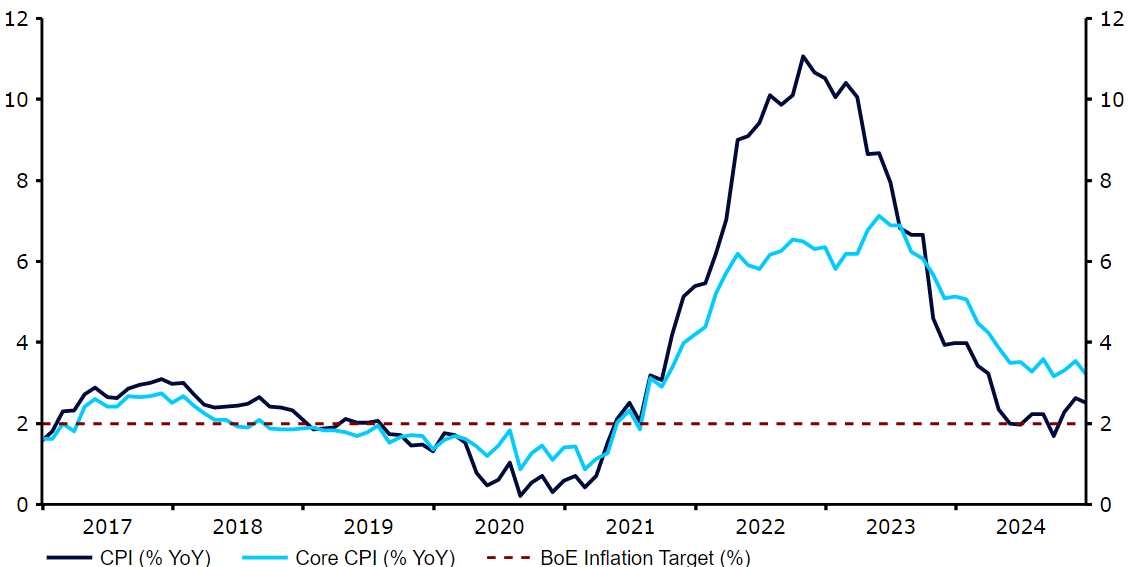

Financial markets breathed easier after better than expected inflation data out of the US last week.Treasury yields dropped sharply across the curve, risk assets rallied, and the dollar fell against all its G10 peers, including the pound and the Canadian dollar, both of which are mired in domestic troubles. Most emerging market currencies rebounded as well off the back of the inflation news. The moves were, however, mostly quite shallow, as financial markets await details on the Trump administration's tariffs, with investors unwilling to push too hard on any trend until there is more visibility on that front.The Martin Luther King holiday means a relatively light economic and policy calendar in the US on Monday, so all eyes will be on Trump’s inauguration at 5pm GMT today. This looks set to accelerate the newsflow around all aspects of economic policy, particularly his tariff plans, which are likely to drive moves in financial markets in the near future. Trump has already planned a ‘blizzard’ of executive orders on his first day back in the White House, so investors will be awaiting his upcoming communications with baited breath.USDLast week’s inflation report brought some very welcome relief for the Federal Reserve. Our favourite indicator, the annualised three-month average in the core index, fell noticeably, from 3.7% to 3.3%, while the underlying measure printed below 0.3% on the month for the first time in five months. Markets are now pricing in almost two 25 basis point cuts from the Fed in 2025 and a terminal rate of about 4%.The 10-year Treasury rate fell back for the first time this year, bringing a pause to the dollar rally for now, and boosting risk assets worldwide. In this holiday-shortened week, we will focus almost exclusively on news and hints emanating from Trump's economic team, primarily on his plans for tariffs. Any details on his fiscal policy, and the administration’s attitude towards the Federal Reserve, could also prove to be market moving.Figure 1: US 10-year Treasury Yield (2024 - 2025) Source: LSEG Datastream Date: 20/01/2025 EURThe lack of timely data out of the Eurozone makes it particularly difficult to gauge the strength of the common bloc economy. For instance, we have seen some tentative signs of stabilisation in the downbeat industrial sector, although the latest data we have is from November. Last week’s HICP data matched the initial estimate, confirming that the main inflation rate edged up to a five month high in December. Yet, communications from the ECB have remained dovish, notably from member de guindos last week, and markets still see at least two more cuts at the next two meetings as a near certainty.This lack of economic news makes the release of the January PMI surveys on Friday particularly important for the euro and the prospects for ECB cuts in the near-term. A number above the key level of 50 in the composite index would signal that the economy is expanding again, and could provide some badly needed relief for the euro - this appears a very long way from guaranteed, however. GBPSterling continues to struggle in the aftermath of the sharp 2025 sell off in gilts, which essentially amount to a vote of no confidence in Labour's fiscal policies and the prospect of a widening deficit. The sell-off in sterling was compounded last week, after UK inflation also came in lower than expected in December. To make matters worse, we saw another miss in the latest monthly GDP report, with Britain’s economy barely growing in November, following consecutive periods of contraction in the two preceding months.The generally weaker tone of the latest economic releases has revived the prospect of Bank of England interest rate cuts, which is not helping the pound either. Indeed, markets now see a strong chance of another rate reduction at the next MPC meeting in February, with a 25 basis point cut currently more than 80% priced in by swaps. We’ll see a raft of labour data out of the UK on Tuesday. This will be followed by the key PMI numbers for January on Friday, which may confirm the increasingly bleak near-term outlook for the UK economy.Figure 2: UK Inflation Rate (2017 - 2024)

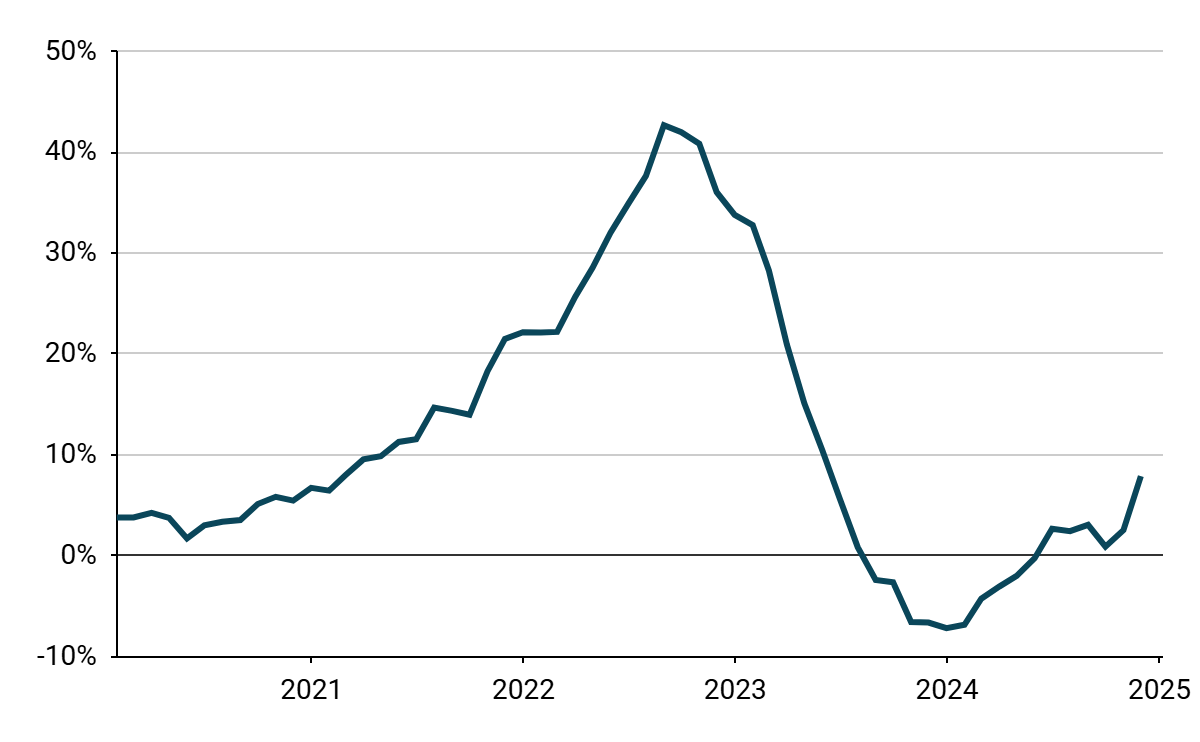

Source: LSEG Datastream Date: 20/01/2025 EURThe lack of timely data out of the Eurozone makes it particularly difficult to gauge the strength of the common bloc economy. For instance, we have seen some tentative signs of stabilisation in the downbeat industrial sector, although the latest data we have is from November. Last week’s HICP data matched the initial estimate, confirming that the main inflation rate edged up to a five month high in December. Yet, communications from the ECB have remained dovish, notably from member de guindos last week, and markets still see at least two more cuts at the next two meetings as a near certainty.This lack of economic news makes the release of the January PMI surveys on Friday particularly important for the euro and the prospects for ECB cuts in the near-term. A number above the key level of 50 in the composite index would signal that the economy is expanding again, and could provide some badly needed relief for the euro - this appears a very long way from guaranteed, however. GBPSterling continues to struggle in the aftermath of the sharp 2025 sell off in gilts, which essentially amount to a vote of no confidence in Labour's fiscal policies and the prospect of a widening deficit. The sell-off in sterling was compounded last week, after UK inflation also came in lower than expected in December. To make matters worse, we saw another miss in the latest monthly GDP report, with Britain’s economy barely growing in November, following consecutive periods of contraction in the two preceding months.The generally weaker tone of the latest economic releases has revived the prospect of Bank of England interest rate cuts, which is not helping the pound either. Indeed, markets now see a strong chance of another rate reduction at the next MPC meeting in February, with a 25 basis point cut currently more than 80% priced in by swaps. We’ll see a raft of labour data out of the UK on Tuesday. This will be followed by the key PMI numbers for January on Friday, which may confirm the increasingly bleak near-term outlook for the UK economy.Figure 2: UK Inflation Rate (2017 - 2024) Source: LSEG Datastream Date: 20/01/2025 RONThe prospect for rate cuts in Romania seems to be pushed away further. Inflation remains higher than expected, as highlighted in the NBR's post-meeting announcement. Its CORE2 measure placed at 5.6% in December, which underlined that these pressures are indeed quite complex in their nature and not solely dependent on rising fuel prices or severe drought conditions last summer. Wage growth remains high, too (13.1% net in December), which may keep it higher for longer. Given the above, we stand by the view that the NBR is likely to resume its cutting cycle rather late, perhaps not until the second half of the year.Figure 3: Romania CPI Inflation & Net Wage Growth (2020 - 2025)Source: Bloomberg, 20/01/2025The coming days will bring some respite, following a rather intense week for the Romanian economists, as no tier-1 macroeconomic readings are scheduled for publication in the coming days. HUFEven though the uptick in inflation was widely expected, its extent came as a surprise to many, with December's 4.6% print being the highest in a year. While this uptick could partly be justified by a lower reference base (a significant drop in inflation towards the end of 2023), we once again saw a 0.5% month-on-month increase in prices, meaning that momentum is not all too favourable - which could become a significant concern.In the face of rather sparse macroeconomic releases, these figures have dominated the local FX discourse over the past week, all the more so as the first MNB meeting of the year is fast approaching (28 January). The inflationary surprise reinforces our belief that there will be no interest rate cut next week, with the pause likely to extend into subsequent meetings.Figure 4: Hungary CPI & Core CPI Inflation [3MAA] (2020 - 2024)

Source: LSEG Datastream Date: 20/01/2025 RONThe prospect for rate cuts in Romania seems to be pushed away further. Inflation remains higher than expected, as highlighted in the NBR's post-meeting announcement. Its CORE2 measure placed at 5.6% in December, which underlined that these pressures are indeed quite complex in their nature and not solely dependent on rising fuel prices or severe drought conditions last summer. Wage growth remains high, too (13.1% net in December), which may keep it higher for longer. Given the above, we stand by the view that the NBR is likely to resume its cutting cycle rather late, perhaps not until the second half of the year.Figure 3: Romania CPI Inflation & Net Wage Growth (2020 - 2025)Source: Bloomberg, 20/01/2025The coming days will bring some respite, following a rather intense week for the Romanian economists, as no tier-1 macroeconomic readings are scheduled for publication in the coming days. HUFEven though the uptick in inflation was widely expected, its extent came as a surprise to many, with December's 4.6% print being the highest in a year. While this uptick could partly be justified by a lower reference base (a significant drop in inflation towards the end of 2023), we once again saw a 0.5% month-on-month increase in prices, meaning that momentum is not all too favourable - which could become a significant concern.In the face of rather sparse macroeconomic releases, these figures have dominated the local FX discourse over the past week, all the more so as the first MNB meeting of the year is fast approaching (28 January). The inflationary surprise reinforces our belief that there will be no interest rate cut next week, with the pause likely to extend into subsequent meetings.Figure 4: Hungary CPI & Core CPI Inflation [3MAA] (2020 - 2024) Source: Bloomberg, 20/01/2025Soft sentiment data (economic, business & consumer confidence) and labour market releases (wage growth and unemployment rate) will reach us in the coming days. Given renewed price pressure concerns, the payroll data, in particular, may prove to be meaningful (albeit not likely to have a significant impact on volatility). PLNAmid a relatively favourable external and domestic environment, the zloty ended the week with minor gains against the euro. A sharp decline in US yields after relentless increases provided room for the dollar to fall and risky assets, such as the PLN, to take a breath. Domestically, the hawkishness of Governor Glapiński at Friday’s press conference has been welcomed by the zloty.His comments suggesting a very cautious approach of the MPC even amid weaker inflation were quite surprising but convince us that we will likely wait a little longer than March for the next rate cuts. This week is set to bring plenty of readings from Poland that will provide some new information on economic activity and trends in the labour market towards the end of the year. The zloty should, however, take more cues from outside signals, particularly as Trump’s inauguration could open door for more volatility.

Source: Bloomberg, 20/01/2025Soft sentiment data (economic, business & consumer confidence) and labour market releases (wage growth and unemployment rate) will reach us in the coming days. Given renewed price pressure concerns, the payroll data, in particular, may prove to be meaningful (albeit not likely to have a significant impact on volatility). PLNAmid a relatively favourable external and domestic environment, the zloty ended the week with minor gains against the euro. A sharp decline in US yields after relentless increases provided room for the dollar to fall and risky assets, such as the PLN, to take a breath. Domestically, the hawkishness of Governor Glapiński at Friday’s press conference has been welcomed by the zloty.His comments suggesting a very cautious approach of the MPC even amid weaker inflation were quite surprising but convince us that we will likely wait a little longer than March for the next rate cuts. This week is set to bring plenty of readings from Poland that will provide some new information on economic activity and trends in the labour market towards the end of the year. The zloty should, however, take more cues from outside signals, particularly as Trump’s inauguration could open door for more volatility.

Source: LSEG Datastream Date: 20/01/2025 EURThe lack of timely data out of the Eurozone makes it particularly difficult to gauge the strength of the common bloc economy. For instance, we have seen some tentative signs of stabilisation in the downbeat industrial sector, although the latest data we have is from November. Last week’s HICP data matched the initial estimate, confirming that the main inflation rate edged up to a five month high in December. Yet, communications from the ECB have remained dovish, notably from member de guindos last week, and markets still see at least two more cuts at the next two meetings as a near certainty.This lack of economic news makes the release of the January PMI surveys on Friday particularly important for the euro and the prospects for ECB cuts in the near-term. A number above the key level of 50 in the composite index would signal that the economy is expanding again, and could provide some badly needed relief for the euro - this appears a very long way from guaranteed, however. GBPSterling continues to struggle in the aftermath of the sharp 2025 sell off in gilts, which essentially amount to a vote of no confidence in Labour's fiscal policies and the prospect of a widening deficit. The sell-off in sterling was compounded last week, after UK inflation also came in lower than expected in December. To make matters worse, we saw another miss in the latest monthly GDP report, with Britain’s economy barely growing in November, following consecutive periods of contraction in the two preceding months.The generally weaker tone of the latest economic releases has revived the prospect of Bank of England interest rate cuts, which is not helping the pound either. Indeed, markets now see a strong chance of another rate reduction at the next MPC meeting in February, with a 25 basis point cut currently more than 80% priced in by swaps. We’ll see a raft of labour data out of the UK on Tuesday. This will be followed by the key PMI numbers for January on Friday, which may confirm the increasingly bleak near-term outlook for the UK economy.Figure 2: UK Inflation Rate (2017 - 2024)Source: LSEG Datastream Date: 20/01/2025 RONThe prospect for rate cuts in Romania seems to be pushed away further. Inflation remains higher than expected, as highlighted in the NBR's post-meeting announcement. Its CORE2 measure placed at 5.6% in December, which underlined that these pressures are indeed quite complex in their nature and not solely dependent on rising fuel prices or severe drought conditions last summer. Wage growth remains high, too (13.1% net in December), which may keep it higher for longer. Given the above, we stand by the view that the NBR is likely to resume its cutting cycle rather late, perhaps not until the second half of the year.Figure 3: Romania CPI Inflation & Net Wage Growth (2020 - 2025)Source: Bloomberg, 20/01/2025The coming days will bring some respite, following a rather intense week for the Romanian economists, as no tier-1 macroeconomic readings are scheduled for publication in the coming days. HUFEven though the uptick in inflation was widely expected, its extent came as a surprise to many, with December's 4.6% print being the highest in a year. While this uptick could partly be justified by a lower reference base (a significant drop in inflation towards the end of 2023), we once again saw a 0.5% month-on-month increase in prices, meaning that momentum is not all too favourable - which could become a significant concern.In the face of rather sparse macroeconomic releases, these figures have dominated the local FX discourse over the past week, all the more so as the first MNB meeting of the year is fast approaching (28 January). The inflationary surprise reinforces our belief that there will be no interest rate cut next week, with the pause likely to extend into subsequent meetings.Figure 4: Hungary CPI & Core CPI Inflation [3MAA] (2020 - 2024)Source: Bloomberg, 20/01/2025Soft sentiment data (economic, business & consumer confidence) and labour market releases (wage growth and unemployment rate) will reach us in the coming days. Given renewed price pressure concerns, the payroll data, in particular, may prove to be meaningful (albeit not likely to have a significant impact on volatility). PLNAmid a relatively favourable external and domestic environment, the zloty ended the week with minor gains against the euro. A sharp decline in US yields after relentless increases provided room for the dollar to fall and risky assets, such as the PLN, to take a breath. Domestically, the hawkishness of Governor Glapiński at Friday’s press conference has been welcomed by the zloty.His comments suggesting a very cautious approach of the MPC even amid weaker inflation were quite surprising but convince us that we will likely wait a little longer than March for the next rate cuts. This week is set to bring plenty of readings from Poland that will provide some new information on economic activity and trends in the labour market towards the end of the year. The zloty should, however, take more cues from outside signals, particularly as Trump’s inauguration could open door for more volatility.