Currency markets volatile as traders digest Trump tariff news

President Trump's decision to postpone tariffs on Canadian and Mexican goods last Monday whipsawed markets, and led initially to a sharp relief rally in major currencies.

FX Market Updates

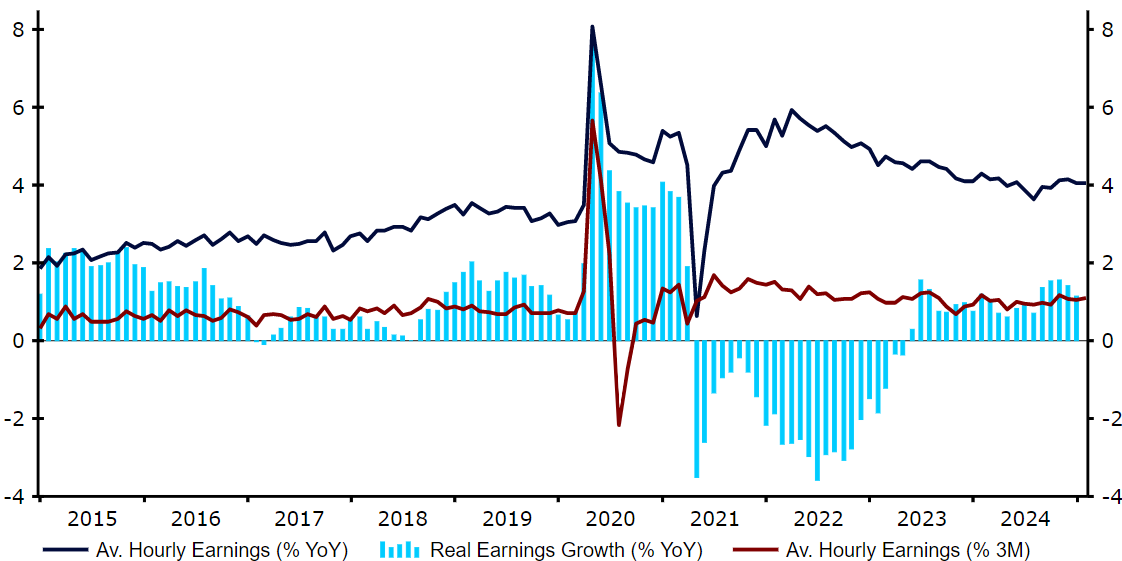

President Trump's decision to postpone tariffs on Canadian and Mexican goods last Monday whipsawed markets, and led initially to a sharp relief rally in major currencies.This recovery in risk assets faded throughout the week, as Trump insisted that tariffs are coming, but failed to clarify their extent or breadth. A strong January US payrolls report pressured European currencies, in particular, by highlighting the significant performance gap between the US and European economies. The overall winner last week was the yen, which continues to rally as traders price in more aggressive hikes from the Bank of Japan, and the currency benefits from its obvious cheapness after years of underperformance.Trump's announcement of 25% steel and aluminum tariffs over the weekend will be key for markets. Investors appear torn between fear about the impact of the trade restrictions and relief that the higher tariffs seem to be reserved for specific sectors. Beyond tariffs, the focus will be the key inflation report out of the US on Tuesday. With tariffs likely to put further upward pressure on US prices, the Fed's tolerance for another above-target month will be limited and the prospect of cuts should fade further. Beyond that, UK GDP figures for Q4 2024 will provide important, though lagged, information for sterling. USDTrying to predict the next tariff news to hit the newswires is a bit of a fool's errand, so it is perhaps more productive to focus more on the macroeconomic backdrop. Last week’s nonfarm payrolls report was, once again, consistent with a US labour market that remains strong. Companies continue to create jobs at a healthy clip, the unemployment rate is hovering around levels consistent with full employment, and the report showed a surprise uptick in wages in January - monthly earnings rose at their fastest pace since mid-2023.All of this positive economic news, plus the looming threat of price hikes from Trump's tariffs, makes it increasingly difficult to justify any further interest rate cuts at all from the Fed in 2025. With rates in the US remaining almost the highest in the G10, we think that it will be difficult for the dollar to sell-off in spite of its admittedly very expensive levels.Figure 1: US Average Hourly Earnings (2015 - 2025)

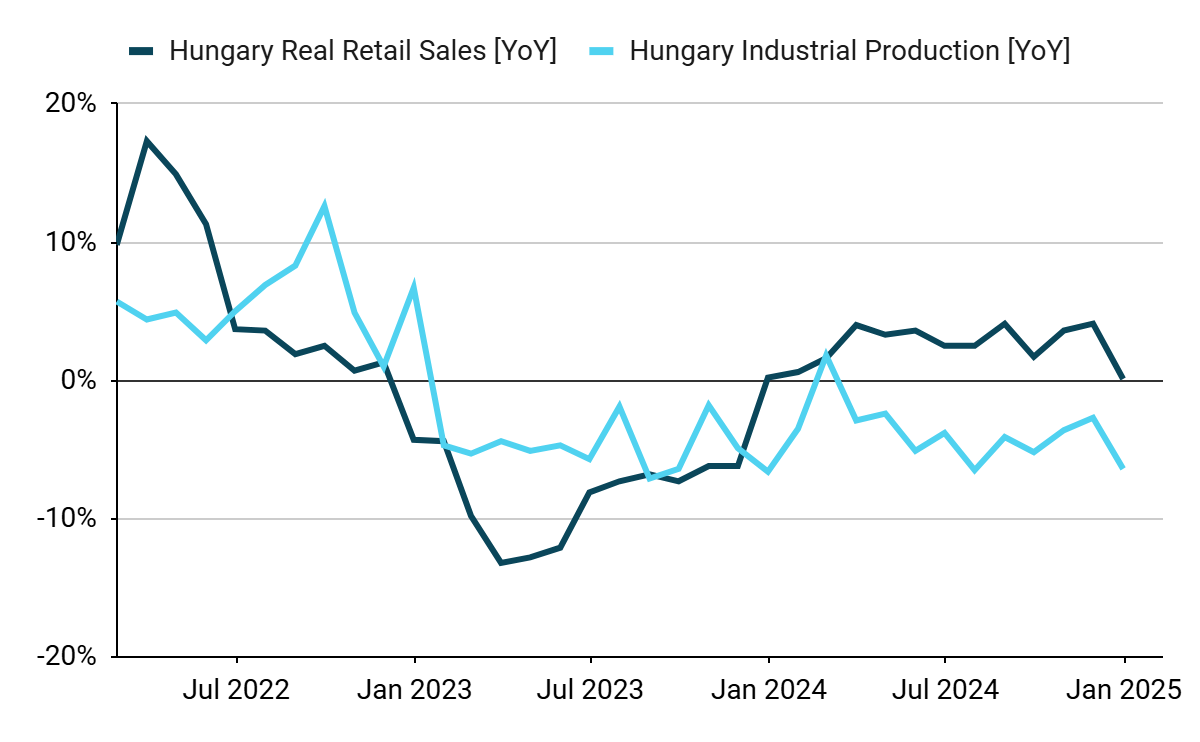

USDTrying to predict the next tariff news to hit the newswires is a bit of a fool's errand, so it is perhaps more productive to focus more on the macroeconomic backdrop. Last week’s nonfarm payrolls report was, once again, consistent with a US labour market that remains strong. Companies continue to create jobs at a healthy clip, the unemployment rate is hovering around levels consistent with full employment, and the report showed a surprise uptick in wages in January - monthly earnings rose at their fastest pace since mid-2023.All of this positive economic news, plus the looming threat of price hikes from Trump's tariffs, makes it increasingly difficult to justify any further interest rate cuts at all from the Fed in 2025. With rates in the US remaining almost the highest in the G10, we think that it will be difficult for the dollar to sell-off in spite of its admittedly very expensive levels.Figure 1: US Average Hourly Earnings (2015 - 2025) Source: LSEG Datastream Date: 10/02/2025EURLast week’s January inflation data for the Euro Area surprised to the upside. We note that the core index first fell to 2.7% nine months ago, and has failed to improve at all since that time. As in the UK, dismal growth is more a factor of restrictions to supply than insufficient demand, and we think that the ECB will, therefore, have difficulty cutting rates much further.Tariffs and the manufacturing recession are certainly negative factors for the common currency, but we think that current levels against the dollar largely price them in already. All eyes will now be firmly on the Trump administration, which has firmly indicated that trade restrictions aimed at the European Union are in the offing. Reports have suggested that a blanket tariff of 10% could be on the way, and it will be interesting to see to what extent this is already incorporated into the price of the euro - we would suggest, not entirely. GBPWeaker than expected economic data led to a very dovish MPC voting split after the Bank of England’s February meeting. All nine members of the rate-setting committee opted for lower rates last week, with two of the nine members, including hawk Catherine Mann, actually voting for a 50bp rate reduction, rather than the 25bp one delivered. The revised 2025 economic growth projection, which was slashed in half relative to the previous estimate, provides a clear indication of just how concerned the BoE is with Britain’s economy.Sterling bounced back after an initial sell off, but it is still the worst performing G10 currency so far in 2025. We think the prospects for the pound are relatively good, however. Inflation remains sticky and wage growth remains elevated, and firmly positive in real terms. We think that markets may be overstating the degree to which the Bank of England will be able to cut rates this year, as the MPC itself stressed that ‘gradual’ cuts remain the way forward. RONRetail sales declined for the third month in a row, but it is hard to say whether this already marks some kind of a slowdown in domestic demand. Nonetheless, it still places at very healthy levels (7.8% in December). Q4 GDP data (coming on Friday, 14/02) should be substantially more important in this regard, likely showing the largest QoQ growth in 5 quarters. The same day will bring January inflation data and a NBR meeting, likely a “non-event”.Figure 2: Romania Retail SalesAll this has been overshadowed by the resignation of a centrist President of the country, Klaus Iohannis, who has already served the maximum tenure at the position (10 years) and has only continued to his office as the latest presidential election, won by the controversial Calin Georgescu, were cancelled in December. This has consequently led to a bit of a crisis, with the far-right parties actively seeking Iohannis’ ouster. The parliament has been expected to vote for the impeachment and the President himself decided to “spare Romania from this crisis”. HUFForint continued to be the biggest regional winner of risk-on, which has been the case since the beginning of the year. With no major political headlines, the Hungarian currency is well positioned to capitalise on improved sentiment, slowly regaining the ground lost last year. Interest rates also remain at elevated levels (base rate at 6.5%, unchanged since September), which provides further support towards the HUF.We do not foresee the loosening of the monetary policy soon, as inflation stopped to decline, actually edging up since the mid-2024 lows. The January reading (11/02) should further emphasise this point. An economic slowdown may bring cuts a little closer, however, as most of the data has been rather disappointing as of late. December’s retail sales were particularly poor, printing at the lowest level in a year, barely above 0 (0,1%).Figure 3: Hungary Retail Sales & Industrial Production (2021 - 2025)

Source: LSEG Datastream Date: 10/02/2025EURLast week’s January inflation data for the Euro Area surprised to the upside. We note that the core index first fell to 2.7% nine months ago, and has failed to improve at all since that time. As in the UK, dismal growth is more a factor of restrictions to supply than insufficient demand, and we think that the ECB will, therefore, have difficulty cutting rates much further.Tariffs and the manufacturing recession are certainly negative factors for the common currency, but we think that current levels against the dollar largely price them in already. All eyes will now be firmly on the Trump administration, which has firmly indicated that trade restrictions aimed at the European Union are in the offing. Reports have suggested that a blanket tariff of 10% could be on the way, and it will be interesting to see to what extent this is already incorporated into the price of the euro - we would suggest, not entirely. GBPWeaker than expected economic data led to a very dovish MPC voting split after the Bank of England’s February meeting. All nine members of the rate-setting committee opted for lower rates last week, with two of the nine members, including hawk Catherine Mann, actually voting for a 50bp rate reduction, rather than the 25bp one delivered. The revised 2025 economic growth projection, which was slashed in half relative to the previous estimate, provides a clear indication of just how concerned the BoE is with Britain’s economy.Sterling bounced back after an initial sell off, but it is still the worst performing G10 currency so far in 2025. We think the prospects for the pound are relatively good, however. Inflation remains sticky and wage growth remains elevated, and firmly positive in real terms. We think that markets may be overstating the degree to which the Bank of England will be able to cut rates this year, as the MPC itself stressed that ‘gradual’ cuts remain the way forward. RONRetail sales declined for the third month in a row, but it is hard to say whether this already marks some kind of a slowdown in domestic demand. Nonetheless, it still places at very healthy levels (7.8% in December). Q4 GDP data (coming on Friday, 14/02) should be substantially more important in this regard, likely showing the largest QoQ growth in 5 quarters. The same day will bring January inflation data and a NBR meeting, likely a “non-event”.Figure 2: Romania Retail SalesAll this has been overshadowed by the resignation of a centrist President of the country, Klaus Iohannis, who has already served the maximum tenure at the position (10 years) and has only continued to his office as the latest presidential election, won by the controversial Calin Georgescu, were cancelled in December. This has consequently led to a bit of a crisis, with the far-right parties actively seeking Iohannis’ ouster. The parliament has been expected to vote for the impeachment and the President himself decided to “spare Romania from this crisis”. HUFForint continued to be the biggest regional winner of risk-on, which has been the case since the beginning of the year. With no major political headlines, the Hungarian currency is well positioned to capitalise on improved sentiment, slowly regaining the ground lost last year. Interest rates also remain at elevated levels (base rate at 6.5%, unchanged since September), which provides further support towards the HUF.We do not foresee the loosening of the monetary policy soon, as inflation stopped to decline, actually edging up since the mid-2024 lows. The January reading (11/02) should further emphasise this point. An economic slowdown may bring cuts a little closer, however, as most of the data has been rather disappointing as of late. December’s retail sales were particularly poor, printing at the lowest level in a year, barely above 0 (0,1%).Figure 3: Hungary Retail Sales & Industrial Production (2021 - 2025) PLNThe Polish zloty goes from strength to strength. After crossing the 4.20 threshold, EUR/PLN is slowly edging lower despite a fall in EUR/USD in the last few days. The recent resilience of the Polish currency is quite impressive, and some of it could be attributed to the hawkishness of the National Bank of Poland. Last week, governor Glapiński reiterated that, at present, the economic environment is not supportive of rate reductions. This is somewhat questionable, but perhaps the NBP wants to eliminate any doubts before engaging in the rate-cut cycle. We now consider a cut in March as highly unlikely, but the meeting will be important due to a release of updated macroeconomic projections. A persistence of hawkish communications from the NBP could keep the PLN well bid, but we still see rate reductions in 2025.Although attention should be primarily on the outside news, this week’s Q4 GDP data (Thursday) and fresh January CPI report (Friday) will be worth watching.

PLNThe Polish zloty goes from strength to strength. After crossing the 4.20 threshold, EUR/PLN is slowly edging lower despite a fall in EUR/USD in the last few days. The recent resilience of the Polish currency is quite impressive, and some of it could be attributed to the hawkishness of the National Bank of Poland. Last week, governor Glapiński reiterated that, at present, the economic environment is not supportive of rate reductions. This is somewhat questionable, but perhaps the NBP wants to eliminate any doubts before engaging in the rate-cut cycle. We now consider a cut in March as highly unlikely, but the meeting will be important due to a release of updated macroeconomic projections. A persistence of hawkish communications from the NBP could keep the PLN well bid, but we still see rate reductions in 2025.Although attention should be primarily on the outside news, this week’s Q4 GDP data (Thursday) and fresh January CPI report (Friday) will be worth watching.

USDTrying to predict the next tariff news to hit the newswires is a bit of a fool's errand, so it is perhaps more productive to focus more on the macroeconomic backdrop. Last week’s nonfarm payrolls report was, once again, consistent with a US labour market that remains strong. Companies continue to create jobs at a healthy clip, the unemployment rate is hovering around levels consistent with full employment, and the report showed a surprise uptick in wages in January - monthly earnings rose at their fastest pace since mid-2023.All of this positive economic news, plus the looming threat of price hikes from Trump's tariffs, makes it increasingly difficult to justify any further interest rate cuts at all from the Fed in 2025. With rates in the US remaining almost the highest in the G10, we think that it will be difficult for the dollar to sell-off in spite of its admittedly very expensive levels.Figure 1: US Average Hourly Earnings (2015 - 2025)Source: LSEG Datastream Date: 10/02/2025EURLast week’s January inflation data for the Euro Area surprised to the upside. We note that the core index first fell to 2.7% nine months ago, and has failed to improve at all since that time. As in the UK, dismal growth is more a factor of restrictions to supply than insufficient demand, and we think that the ECB will, therefore, have difficulty cutting rates much further.Tariffs and the manufacturing recession are certainly negative factors for the common currency, but we think that current levels against the dollar largely price them in already. All eyes will now be firmly on the Trump administration, which has firmly indicated that trade restrictions aimed at the European Union are in the offing. Reports have suggested that a blanket tariff of 10% could be on the way, and it will be interesting to see to what extent this is already incorporated into the price of the euro - we would suggest, not entirely. GBPWeaker than expected economic data led to a very dovish MPC voting split after the Bank of England’s February meeting. All nine members of the rate-setting committee opted for lower rates last week, with two of the nine members, including hawk Catherine Mann, actually voting for a 50bp rate reduction, rather than the 25bp one delivered. The revised 2025 economic growth projection, which was slashed in half relative to the previous estimate, provides a clear indication of just how concerned the BoE is with Britain’s economy.Sterling bounced back after an initial sell off, but it is still the worst performing G10 currency so far in 2025. We think the prospects for the pound are relatively good, however. Inflation remains sticky and wage growth remains elevated, and firmly positive in real terms. We think that markets may be overstating the degree to which the Bank of England will be able to cut rates this year, as the MPC itself stressed that ‘gradual’ cuts remain the way forward. RONRetail sales declined for the third month in a row, but it is hard to say whether this already marks some kind of a slowdown in domestic demand. Nonetheless, it still places at very healthy levels (7.8% in December). Q4 GDP data (coming on Friday, 14/02) should be substantially more important in this regard, likely showing the largest QoQ growth in 5 quarters. The same day will bring January inflation data and a NBR meeting, likely a “non-event”.Figure 2: Romania Retail SalesAll this has been overshadowed by the resignation of a centrist President of the country, Klaus Iohannis, who has already served the maximum tenure at the position (10 years) and has only continued to his office as the latest presidential election, won by the controversial Calin Georgescu, were cancelled in December. This has consequently led to a bit of a crisis, with the far-right parties actively seeking Iohannis’ ouster. The parliament has been expected to vote for the impeachment and the President himself decided to “spare Romania from this crisis”. HUFForint continued to be the biggest regional winner of risk-on, which has been the case since the beginning of the year. With no major political headlines, the Hungarian currency is well positioned to capitalise on improved sentiment, slowly regaining the ground lost last year. Interest rates also remain at elevated levels (base rate at 6.5%, unchanged since September), which provides further support towards the HUF.We do not foresee the loosening of the monetary policy soon, as inflation stopped to decline, actually edging up since the mid-2024 lows. The January reading (11/02) should further emphasise this point. An economic slowdown may bring cuts a little closer, however, as most of the data has been rather disappointing as of late. December’s retail sales were particularly poor, printing at the lowest level in a year, barely above 0 (0,1%).Figure 3: Hungary Retail Sales & Industrial Production (2021 - 2025)PLNThe Polish zloty goes from strength to strength. After crossing the 4.20 threshold, EUR/PLN is slowly edging lower despite a fall in EUR/USD in the last few days. The recent resilience of the Polish currency is quite impressive, and some of it could be attributed to the hawkishness of the National Bank of Poland. Last week, governor Glapiński reiterated that, at present, the economic environment is not supportive of rate reductions. This is somewhat questionable, but perhaps the NBP wants to eliminate any doubts before engaging in the rate-cut cycle. We now consider a cut in March as highly unlikely, but the meeting will be important due to a release of updated macroeconomic projections. A persistence of hawkish communications from the NBP could keep the PLN well bid, but we still see rate reductions in 2025.Although attention should be primarily on the outside news, this week’s Q4 GDP data (Thursday) and fresh January CPI report (Friday) will be worth watching.