Currency markets in holding pattern awaiting April 2nd tariff news

Currencies traded within tight ranges of each other in a week when economic or policy news was relatively sparse, awaiting Trump's announcement on "reciprocal tariffs" on Wednesday.

FX Market Updates

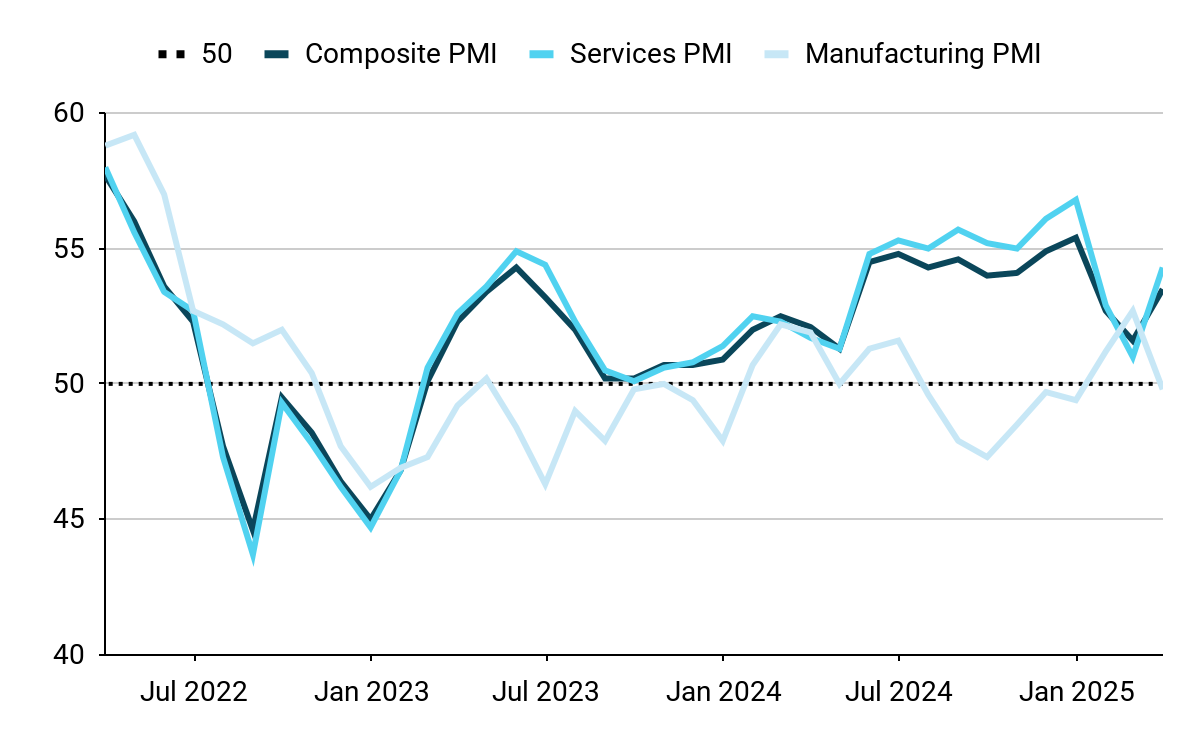

Currencies traded within tight ranges of each other in a week when economic or policy news was relatively sparse, awaiting Trump's announcement on "reciprocal tariffs" on Wednesday.This announcement will come right after a volley of 25% flat tariff on all foreign-made vehicles imported into the US. The consensus seems to be for a significant announcement that could bring the average tariff in the US to well above 10%, from just 2.5% before Trump took office.The dollar is caught in the crosswinds between the boost one would expect from higher tariffs and the increasingly apparent economic damage from Trump’s chaotic policies and disregard for their economic impact. Inflation is rising as consumers retreat, posing a particularly difficult dilemma for the Federal Reserve. This week's key releases will be the March flash inflation report in the Eurozone on Tuesday and a spate of US labor data starting Wednesday with the JOLTS report and culminating Friday with the all-important payroll report for March. USDEvidence that Trumpian chaos is harming consumer confidence, expectations, and spending is piling up, but it's still short of dispositive. Consumer spending in February again undershot expectations, while the core index of the Fed’s preferred gauge, the PCE rose again on a monthly basis.On the other hand, the March services PMI surprised heavily to the upside, driving the composite sharply higher. In addition to the tariff announcement, this week's employment data (JOLTS on Wednesday, jobless claims on Thursday and, critically, the March payroll report on Friday) take on added importance to confirm whether consumer retrenchment is starting to affect business hiring decisions.Figure 1: US PMIs (2022 - 2025)

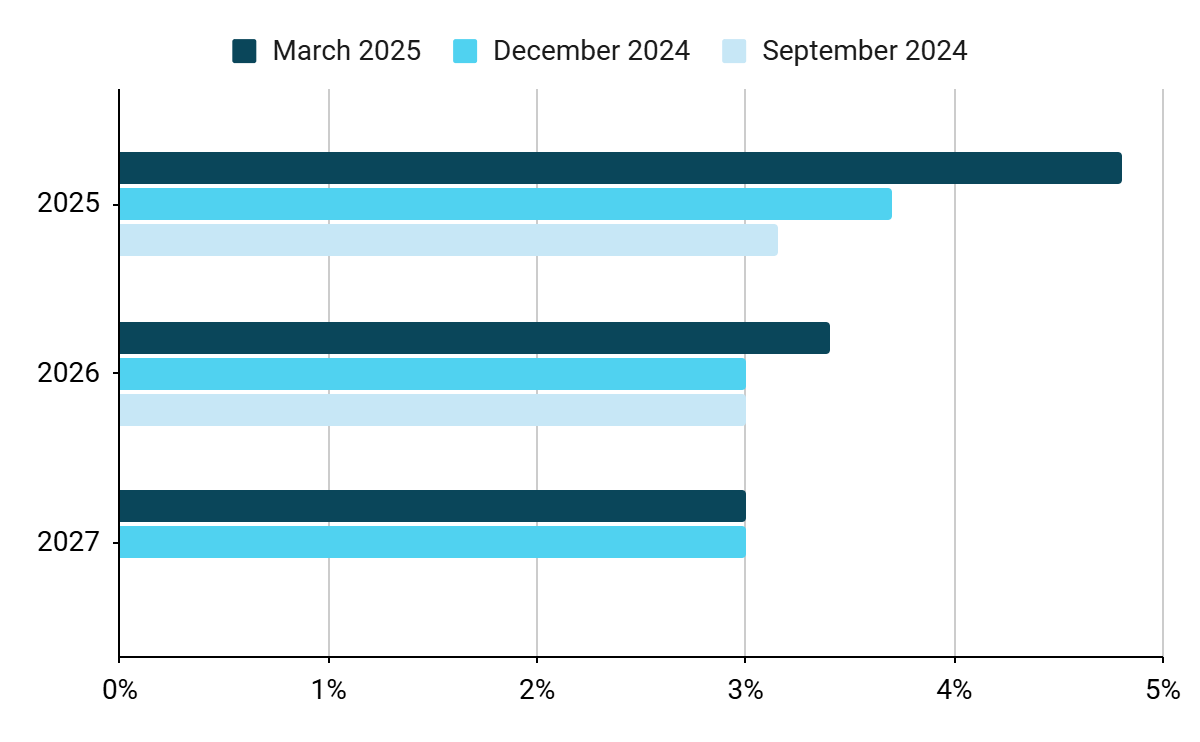

USDEvidence that Trumpian chaos is harming consumer confidence, expectations, and spending is piling up, but it's still short of dispositive. Consumer spending in February again undershot expectations, while the core index of the Fed’s preferred gauge, the PCE rose again on a monthly basis.On the other hand, the March services PMI surprised heavily to the upside, driving the composite sharply higher. In addition to the tariff announcement, this week's employment data (JOLTS on Wednesday, jobless claims on Thursday and, critically, the March payroll report on Friday) take on added importance to confirm whether consumer retrenchment is starting to affect business hiring decisions.Figure 1: US PMIs (2022 - 2025) Source: Bloomberg Date: 31/03/2025 EURThe March PMIs out of the Eurozone fail to reflect the optimism that has swept European financial markets after the massive fiscal stimulus announcement coming out of Germany. The composite PMI index was almost unchanged and is still consistent with near stagnation.The flash inflation report this Tuesday should be better news for the ECB, as the numbers in France and Spain have surprised to the downside. The tariff announcement this week, however, should be the main focus of the week, given the Eurozone's massive trade surplus with the US, and it's difficult to see the common currency breaking to the upside under these conditions. GBPThe UK's economic outlook remains underpinned by improving demand and the UK’s relatively low exposure to Trump’s tariffs, as it is a country that mostly exports services and runs a significant trade deficit with the US. The PMI surveys of business activity for March improved meaningfully and unexpectedly, and are now consistent with steady growth, led by the services sector.February retail sales also outperformed expectations, diverting attention from OBR’s halving of the UK’s 2025 GDP forecast to 1%. Moreover, British households received a welcome relief from a sharp drop in inflation. That said, persistently high growth in prices of services to the tune of 5% suggests it is not yet time for the Bank of England to abandon its cautious approach to policy easing, in our view. The combination of steadying growth, resilience to tariffs and better ties with the EU remains the key supportive factor for sterling. RONOn April 4, the electoral campaign for the May presidential elections officially begins, and we can now confirm that 11 candidates will participate. According to current polls, George Simion – the founder and chairman of the Alliance for the Union of Romanians (AUR), a right-wing populist and nationalist party – is the frontrunner in the first round of the elections. This somewhat confirms a trend we already observed in the initial voting: the right wing is thriving very well in Romania. Simion’s rival in the second round would likely be either Crin Antonescu or Nicusor Dan, both of whom can be classified as liberal center-right politicians. One of them would most likely emerge as the favorite in a direct duel with Simion.Ahead of us is another data-light week. Apart from Tuesday’s release of the PMI indicator for the industrial sector and the unemployment rate, we won’t see any readings likely to capture significant attention from economists. HUFAlthough the Hungarian National Bank (MNB) meeting delivered rather hawkish rhetoric and a significant upward revision of inflation forecasts (the midpoint of the 2025 projection range increased from 3.7% to 4.8%), it was not an easy week for the forint.Figure 2: MNB Hungary Inflation Projections (2025 - 2027)

Source: Bloomberg Date: 31/03/2025 EURThe March PMIs out of the Eurozone fail to reflect the optimism that has swept European financial markets after the massive fiscal stimulus announcement coming out of Germany. The composite PMI index was almost unchanged and is still consistent with near stagnation.The flash inflation report this Tuesday should be better news for the ECB, as the numbers in France and Spain have surprised to the downside. The tariff announcement this week, however, should be the main focus of the week, given the Eurozone's massive trade surplus with the US, and it's difficult to see the common currency breaking to the upside under these conditions. GBPThe UK's economic outlook remains underpinned by improving demand and the UK’s relatively low exposure to Trump’s tariffs, as it is a country that mostly exports services and runs a significant trade deficit with the US. The PMI surveys of business activity for March improved meaningfully and unexpectedly, and are now consistent with steady growth, led by the services sector.February retail sales also outperformed expectations, diverting attention from OBR’s halving of the UK’s 2025 GDP forecast to 1%. Moreover, British households received a welcome relief from a sharp drop in inflation. That said, persistently high growth in prices of services to the tune of 5% suggests it is not yet time for the Bank of England to abandon its cautious approach to policy easing, in our view. The combination of steadying growth, resilience to tariffs and better ties with the EU remains the key supportive factor for sterling. RONOn April 4, the electoral campaign for the May presidential elections officially begins, and we can now confirm that 11 candidates will participate. According to current polls, George Simion – the founder and chairman of the Alliance for the Union of Romanians (AUR), a right-wing populist and nationalist party – is the frontrunner in the first round of the elections. This somewhat confirms a trend we already observed in the initial voting: the right wing is thriving very well in Romania. Simion’s rival in the second round would likely be either Crin Antonescu or Nicusor Dan, both of whom can be classified as liberal center-right politicians. One of them would most likely emerge as the favorite in a direct duel with Simion.Ahead of us is another data-light week. Apart from Tuesday’s release of the PMI indicator for the industrial sector and the unemployment rate, we won’t see any readings likely to capture significant attention from economists. HUFAlthough the Hungarian National Bank (MNB) meeting delivered rather hawkish rhetoric and a significant upward revision of inflation forecasts (the midpoint of the 2025 projection range increased from 3.7% to 4.8%), it was not an easy week for the forint.Figure 2: MNB Hungary Inflation Projections (2025 - 2027) Source: MNB Date: 31/03/2025In terms of the aforementioned forecasts, we did also receive a substantial downward revision of growth projections for 2025 (from 3.1% to 2.4%). Additionally, on Thursday, the Finance Minister announced that starting in October, investment funds will be required to hold at least 3% of their portfolios in short-term Hungarian bonds. This is yet another measure of this kind, following the recent introduction of a 5% long-term bonds requirement. Both limits are set to increase by 1 pp. next year. This represents another intervention that undermines confidence in the Hungarian financial market. Unsurprisingly, it did also weigh the forint, which hit the bottom of the Central and Eastern Europe (CEE) regional dashboard.Figure 3: MNB Hungary GDP Growth Projections (2025 - 2027)

Source: MNB Date: 31/03/2025In terms of the aforementioned forecasts, we did also receive a substantial downward revision of growth projections for 2025 (from 3.1% to 2.4%). Additionally, on Thursday, the Finance Minister announced that starting in October, investment funds will be required to hold at least 3% of their portfolios in short-term Hungarian bonds. This is yet another measure of this kind, following the recent introduction of a 5% long-term bonds requirement. Both limits are set to increase by 1 pp. next year. This represents another intervention that undermines confidence in the Hungarian financial market. Unsurprisingly, it did also weigh the forint, which hit the bottom of the Central and Eastern Europe (CEE) regional dashboard.Figure 3: MNB Hungary GDP Growth Projections (2025 - 2027)

USDEvidence that Trumpian chaos is harming consumer confidence, expectations, and spending is piling up, but it's still short of dispositive. Consumer spending in February again undershot expectations, while the core index of the Fed’s preferred gauge, the PCE rose again on a monthly basis.On the other hand, the March services PMI surprised heavily to the upside, driving the composite sharply higher. In addition to the tariff announcement, this week's employment data (JOLTS on Wednesday, jobless claims on Thursday and, critically, the March payroll report on Friday) take on added importance to confirm whether consumer retrenchment is starting to affect business hiring decisions.Figure 1: US PMIs (2022 - 2025)Source: Bloomberg Date: 31/03/2025 EURThe March PMIs out of the Eurozone fail to reflect the optimism that has swept European financial markets after the massive fiscal stimulus announcement coming out of Germany. The composite PMI index was almost unchanged and is still consistent with near stagnation.The flash inflation report this Tuesday should be better news for the ECB, as the numbers in France and Spain have surprised to the downside. The tariff announcement this week, however, should be the main focus of the week, given the Eurozone's massive trade surplus with the US, and it's difficult to see the common currency breaking to the upside under these conditions. GBPThe UK's economic outlook remains underpinned by improving demand and the UK’s relatively low exposure to Trump’s tariffs, as it is a country that mostly exports services and runs a significant trade deficit with the US. The PMI surveys of business activity for March improved meaningfully and unexpectedly, and are now consistent with steady growth, led by the services sector.February retail sales also outperformed expectations, diverting attention from OBR’s halving of the UK’s 2025 GDP forecast to 1%. Moreover, British households received a welcome relief from a sharp drop in inflation. That said, persistently high growth in prices of services to the tune of 5% suggests it is not yet time for the Bank of England to abandon its cautious approach to policy easing, in our view. The combination of steadying growth, resilience to tariffs and better ties with the EU remains the key supportive factor for sterling. RONOn April 4, the electoral campaign for the May presidential elections officially begins, and we can now confirm that 11 candidates will participate. According to current polls, George Simion – the founder and chairman of the Alliance for the Union of Romanians (AUR), a right-wing populist and nationalist party – is the frontrunner in the first round of the elections. This somewhat confirms a trend we already observed in the initial voting: the right wing is thriving very well in Romania. Simion’s rival in the second round would likely be either Crin Antonescu or Nicusor Dan, both of whom can be classified as liberal center-right politicians. One of them would most likely emerge as the favorite in a direct duel with Simion.Ahead of us is another data-light week. Apart from Tuesday’s release of the PMI indicator for the industrial sector and the unemployment rate, we won’t see any readings likely to capture significant attention from economists. HUFAlthough the Hungarian National Bank (MNB) meeting delivered rather hawkish rhetoric and a significant upward revision of inflation forecasts (the midpoint of the 2025 projection range increased from 3.7% to 4.8%), it was not an easy week for the forint.Figure 2: MNB Hungary Inflation Projections (2025 - 2027)Source: MNB Date: 31/03/2025In terms of the aforementioned forecasts, we did also receive a substantial downward revision of growth projections for 2025 (from 3.1% to 2.4%). Additionally, on Thursday, the Finance Minister announced that starting in October, investment funds will be required to hold at least 3% of their portfolios in short-term Hungarian bonds. This is yet another measure of this kind, following the recent introduction of a 5% long-term bonds requirement. Both limits are set to increase by 1 pp. next year. This represents another intervention that undermines confidence in the Hungarian financial market. Unsurprisingly, it did also weigh the forint, which hit the bottom of the Central and Eastern Europe (CEE) regional dashboard.Figure 3: MNB Hungary GDP Growth Projections (2025 - 2027)